")

Why Auto Loan Rates Vary by State: The Big Picture

If you have ever compared notes with a friend in another state about their car loan and wondered why your rate seems higher, you are not imagining things. Auto loan rates by state are genuinely different — sometimes by two or three full percentage points — and those differences can cost or save you thousands of dollars over the life of your loan.

To understand why this happens, think about how auto lending works. When a bank, credit union, or online lender gives you money to buy a car, they are taking on risk. They have to factor in: How likely is this borrower to repay? What happens if they do not — can we repossess the vehicle easily under this state’s laws? What does the broader economy look like in this region? What are other lenders charging? All of these questions get baked into your interest rate.

Because every state has its own laws, its own economic conditions, and its own competitive lending landscape, the answer to those questions changes depending on where you live. A borrower in Connecticut and a borrower in Mississippi with the exact same credit score can walk away with different rates simply because the underlying lending environment in those two states is different.

This matters even more today, in 2025, because auto loan balances are at record highs. The average American financing a vehicle is borrowing more money, for longer terms, than at any previous point in history. That makes it more important than ever to understand exactly where your state sits — and how to make sure you are getting the most competitive rate available to you.

At CarFix Credit, we have helped over 183,000 Americans across all 50 states secure vehicle financing — and one of the most common things we hear from customers is that they had no idea how much they were leaving on the table before they shopped smarter. This guide exists to change that. By the time you finish reading, you will know exactly how to position yourself for the best possible rate, no matter which state you call home.

Key Stat: The gap between the most favorable and least favorable state average APR for a used car loan in 2025 is approximately 1.5% to 2.5%. On a $30,000 loan over 60 months, that difference translates to roughly $1,200 to $2,100 in extra interest paid — money that stays in your pocket if you know how to find the best deal.

What Is an Auto Loan Rate? The Basics Explained Simply

An auto loan rate — formally called an Annual Percentage Rate, or APR — is the yearly cost of borrowing money to buy a vehicle, expressed as a percentage. It includes the interest the lender charges, plus any applicable fees, all rolled into one number that makes it easy to compare offers side by side.

Here is a simple way to think about it: When a lender gives you $25,000 to buy a car, they are essentially renting you that money. The interest rate is the rent you pay. The higher the rate, the more expensive the rental. APR standardizes that rental cost into a single annual figure.

A Real-World Example: How Rate Affects Your Monthly Payment

Let us say you are borrowing $25,000 to finance a used SUV for 60 months. At a 5.5% APR, your monthly payment would be approximately $479 and you would pay a total of $28,740 — meaning $3,740 in interest. At 7.5% APR, your payment rises to around $501 and total interest climbs to $5,060. Push that rate to 10.0% and you are paying roughly $531 per month with $6,860 in interest over the life of the loan. At 14.0%, the monthly payment reaches approximately $582 and total interest paid hits $9,920. And at 20.0% APR, you are looking at a monthly payment of around $661 — and a staggering $14,660 in interest by the time the loan is paid off.

Look at the difference between a 5.5% APR and a 20% APR on the same loan: you pay an extra $10,920 in interest over five years. That is real money — a vacation, a home repair, a college semester. This is exactly why finding the right rate in your state is not just a nice-to-have. It is one of the most important financial decisions you will make.

When you apply through CarFix Credit, our network of lenders competes for your business across all 50 states, which means you are always seeing multiple competitive offers at once — not just whatever one local bank happens to be charging that week.

8 Key Factors That Determine Your Auto Loan Rate

Your auto loan rate is not random. It is calculated based on a specific set of factors that lenders use to assess how much risk they are taking on. Understanding these factors gives you real power to influence the rate you receive.

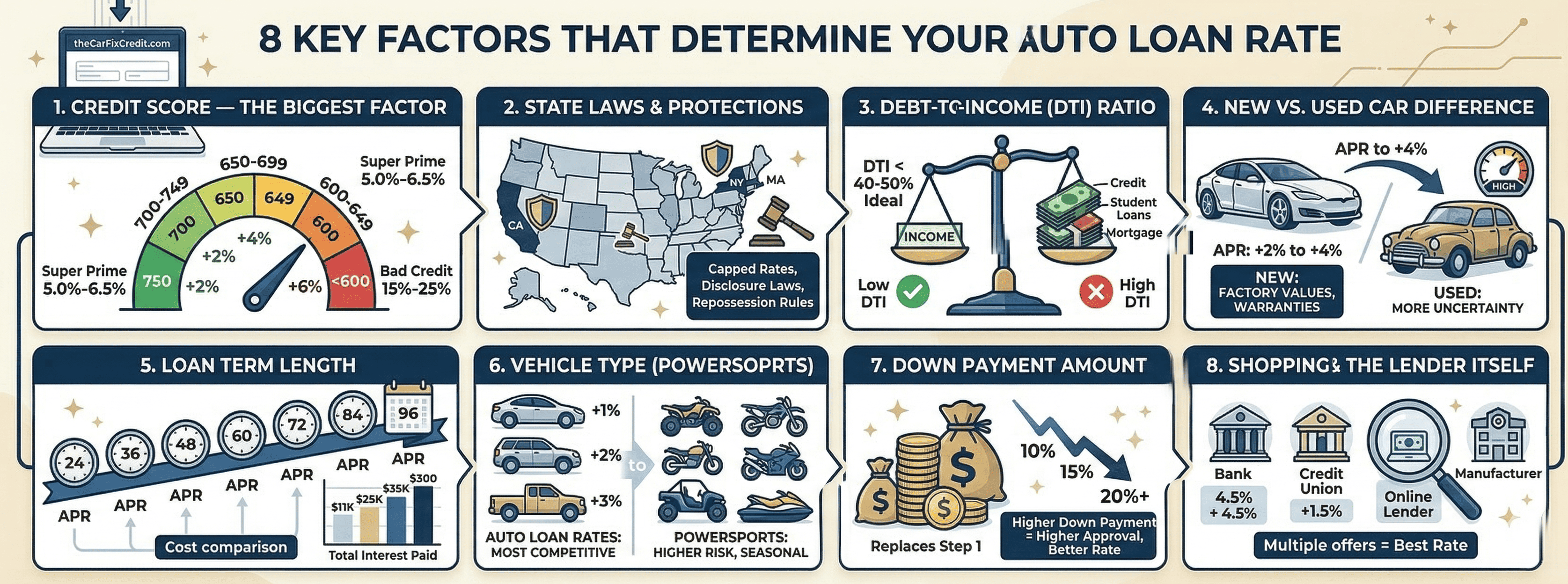

1. Your Credit Score — The Single Biggest Factor

Your credit score is the first number every lender looks at. It is a three-digit summary of your entire borrowing history, and it has an enormous effect on your rate. A borrower with excellent credit can typically secure a rate that is 10 to 15 percentage points lower than a borrower with poor credit on the same loan.

Borrowers with excellent credit — scores in the 750 to 850 range — typically see new car APRs between 5.0% and 6.5%, and used car APRs between 7.5% and 9.5%. Good credit borrowers, those scoring 700 to 749, generally land in the 6.5% to 8.0% range for new cars and 9.0% to 11.0% for used vehicles. Borrowers with fair credit, roughly 650 to 699, can expect new car rates of 8.0% to 11.0% and used car rates of 11.0% to 14.0%. Poor credit borrowers in the 600 to 649 band typically see 11.0% to 15.0% on new cars and 14.0% to 18.0% on used. And for borrowers below 600 — what lenders classify as bad credit — rates generally range from 15.0% to 25.0% and above on new cars, and 18.0% to 28.0% and above on used.

Even if your credit score is less than perfect, you still have options. CarFix Credit specializes in connecting borrowers of all credit backgrounds — including those with bad credit, no credit history, or recent financial setbacks — to lenders willing to work with their situation. Over 183,000 Americans have already been approved through our platform, and many of them came to us after being told “no” somewhere else.

2. State Laws and Consumer Protections

Each state has its own rules governing the auto lending industry. Some states cap the maximum interest rate lenders can charge (these are called usury laws). Others require specific disclosures, dictate how lenders must handle repossessions, or place limits on dealer reserve markups — the extra margin dealers can add on top of a lender’s base rate.

In general, states with stronger consumer protection frameworks — California, Massachusetts, Connecticut, and New York chief among them — tend to have more competitive, lower-average rates. This is partly because lenders must be more transparent, and partly because competition in these densely populated, higher-income states is simply fiercer.

In states with fewer restrictions, some lenders and dealers may charge higher rates, add more fees, or include terms that are harder to navigate. This is exactly why using an online platform like CarFix Credit is so valuable: we surface offers from lenders across the country, so your state’s local market conditions do not automatically limit your options.

3. Your Debt-to-Income Ratio (DTI)

Your debt-to-income ratio is the percentage of your monthly gross income that goes toward debt payments. Most lenders prefer to see a DTI below 40% to 50%. The lower your DTI, the more financial breathing room you appear to have, and the better the rate you can generally access. If you have a lot of existing debt — credit cards, student loans, a mortgage — paying some of it down before applying for an auto loan can meaningfully improve your offer.

4. New Car vs. Used Car — A Significant Rate Difference

New car loans consistently carry lower interest rates than used car loans. This is because new vehicles have predictable, factory-backed values and generally come with manufacturer warranties that protect the lender’s collateral. Used cars, especially older ones, carry more uncertainty: their value can decline faster, and mechanical issues can make them harder to resell in a repossession scenario.

As a general rule, expect used car APRs to run 2% to 4% higher than new car APRs with the same lender. This gap can be even wider for older vehicles — many lenders charge higher rates on cars more than five to seven years old or with high mileage.

CarFix Credit finances a wide range of vehicle ages and conditions, including high-mileage used cars and older model years that some traditional lenders pass on. We understand that not every buyer is in the market for a brand-new car, and our lender network reflects that reality.

5. Loan Term Length — Shorter Costs Less

Loan term — how many months you take to repay the loan — has a direct effect on both your monthly payment and your total interest cost. Shorter terms like 24, 36, or 48 months come with lower APRs because lenders face less risk over a shorter period. Longer terms like 72 or 84 months reduce your monthly payment but almost always come with a higher APR and significantly more total interest paid.

CarFix Credit offers loan terms from as short as 12 months to as long as 96 months. This flexibility lets customers choose the repayment structure that fits their budget — but our financing specialists always walk clients through the total cost comparison so they can make a truly informed decision.

6. Vehicle Type — Cars, Trucks, and Powersports All Have Different Rate Profiles

Not all vehicles are financed the same way. Standard passenger cars — sedans, SUVs, hatchbacks, and pickup trucks — are the most common loan type and generally carry the most competitive rates because lenders have extensive data on their value and resale behavior.

Powersports vehicles are a different story. Motorcycles, ATVs, side-by-sides, and personal watercraft like Sea-Doos are classified differently by most lenders. They are considered higher risk because their market values fluctuate more, they are used seasonally in many states, and their resale pools are smaller. As a result, powersports loans typically carry rates 1% to 3% higher than equivalent auto loans.

Many lenders simply do not offer powersports financing at all. CarFix Credit is one of the few national platforms that finances motorcycles, ATVs, Sea-Doos, and side-by-sides — in all 50 states, for borrowers across the full credit spectrum — through the same easy online pre-approval process as standard auto loans.

7. Down Payment Amount

A larger down payment directly reduces the lender’s risk. When you put 10%, 15%, or 20% down on a vehicle, you are immediately creating equity — a financial cushion that protects the lender even if the vehicle’s value drops. In return, many lenders offer better rates to borrowers who bring a meaningful down payment to the table.

For borrowers with bad credit, a larger down payment can sometimes be the deciding factor between an approval and a rejection, or between a workable rate and an unaffordable one. If you can put even $1,000 to $2,000 extra down, it is often worth it. CarFix Credit’s financing specialists can help you understand exactly how your down payment amount affects your approval odds and your rate.

8. The Lender Itself — Why Shopping Around Matters

This one surprises a lot of people. Two borrowers with identical credit profiles, identical vehicles, and identical loan amounts can receive rates that differ by 2% to 4% simply because they went to different lenders. Banks, credit unions, online lenders, and captive finance arms (the financing divisions of car manufacturers) all have different cost structures, risk appetites, and pricing strategies.

The only way to know you are getting the best rate is to compare multiple offers. That is the core value proposition of CarFix Credit: one application, multiple lenders, all competing for your business. Whether you are in a competitive market like California or a smaller market like Montana, our platform ensures you are not arbitrarily limited to whichever lender happens to be convenient.

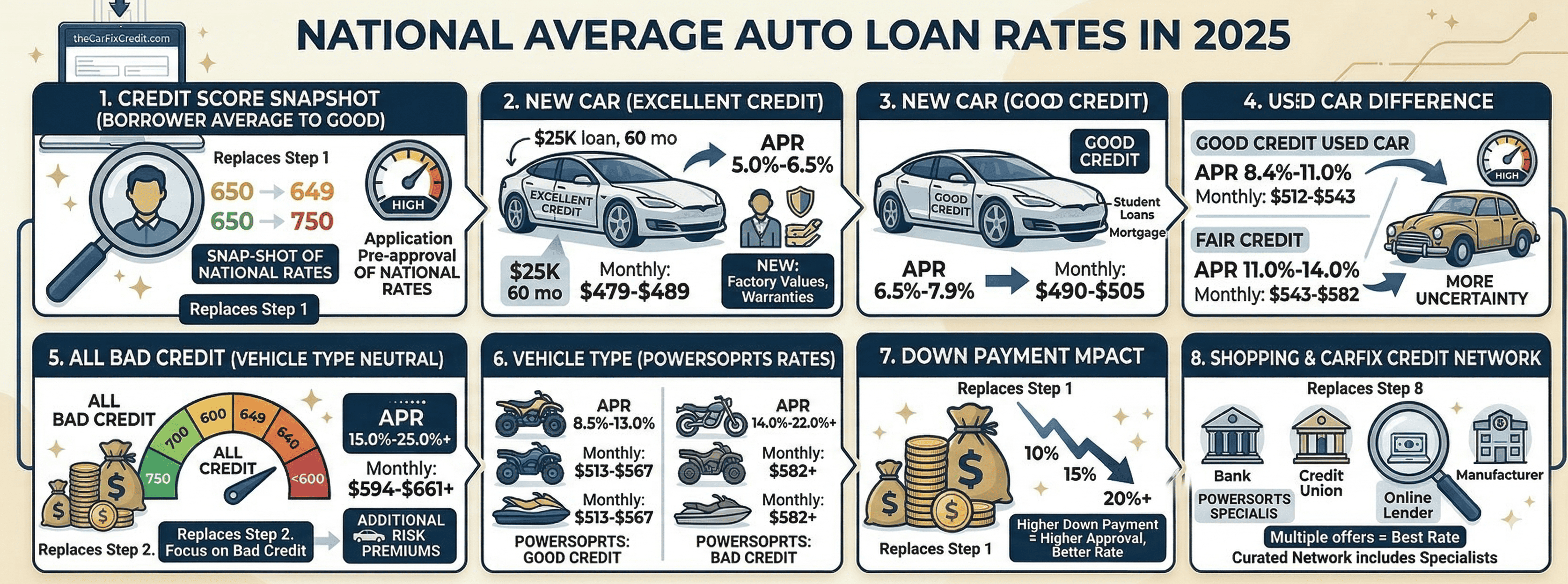

National Average Auto Loan Rates in 2025

Before diving into state-by-state data, here is a snapshot of where national average rates sit in 2025. These ranges represent borrowers with average to good credit, approximately a 650 to 750 credit score. Your individual rate may be higher or lower depending on your credit profile and the lender you choose.

Borrowers with excellent credit financing a new car can expect APRs in the 5.0% to 6.5% range, which translates to a monthly payment of roughly $479 to $489 on a $25,000 loan over 60 months. Good credit new car borrowers typically see rates of 6.5% to 7.9%, putting monthly payments around $490 to $505. Fair credit on a new car generally means 8.0% to 11.0% APR and monthly payments from roughly $507 to $543.

On the used car side, good credit borrowers typically face APRs of 8.4% to 11.0%, with monthly payments around $512 to $543 on a $25,000, 60-month loan. Fair credit used car buyers can expect rates of 11.0% to 14.0% and payments ranging from approximately $543 to $582.

Bad credit borrowers — regardless of vehicle type — generally see APRs starting at 15.0% and extending to 25.0% or higher, which puts estimated monthly payments in the $594 to $661 range and above.

Powersports financing tells a similar story. Good credit borrowers financing a motorcycle, ATV, or watercraft typically encounter rates of 8.5% to 13.0%, with monthly payments from roughly $513 to $567. Bad credit powersports buyers can expect APRs of 14.0% to 22.0% or higher and monthly payments starting around $582.

These powersports figures reflect the reality that powersports loans carry additional risk premiums — but they also reflect the fact that CarFix Credit’s lender network has been curated to include specialists in this vehicle category, which means competitive rates are available even for powersports buyers.

Auto Loan Rates by State

The information below covers all 50 states with estimated APR ranges for average-to-good-credit borrowers in 2025. These are reference ranges — your actual rate will depend on your specific credit profile, selected lender, vehicle type, and current market conditions. Rates update frequently; always verify current offers when actively shopping.

- Alabama — New car APR estimates run from 6.9% to 8.4%, with used car rates typically between 9.2% and 12.1%. Alabama represents an average credit market where dealer markups are common.

- Alaska — New car rates generally fall between 6.5% and 8.0%, with used car rates from 8.8% to 11.5%. Limited lender competition means remote areas may see rates at the higher end of that range.

- Arizona — A competitive market with a strong online lending presence, Arizona typically sees new car APRs of 6.4% to 7.9% and used car rates of 8.6% to 11.2%.

- Arkansas — With moderate lender competition, credit unions tend to offer the best deals. New car rates range from 6.8% to 8.3%, and used car rates from 9.0% to 12.0%.

- California — One of the most competitive markets in the country, bolstered by strong borrower protections. New car APRs typically run 6.2% to 7.7% and used car rates 8.4% to 11.0%.

- Colorado — A competitive market with above-average credit scores statewide. New car rates typically fall between 6.3% and 7.8%, and used car rates between 8.5% and 11.1%.

- Connecticut — Above-average incomes and strong lender competition keep rates among the lowest in the country, with new car APRs of 6.1% to 7.6% and used car rates of 8.3% to 10.9%.

- Delaware — A mid-Atlantic market with moderate competition. New car rates range from 6.3% to 7.8%, with used car rates from 8.5% to 11.2%.

- Florida — A large market with many lenders, though borrowers should watch for dealer add-ons. New car APRs typically run 6.5% to 8.0% and used car rates 8.7% to 11.4%.

- Georgia — A growing market with a wide range of lender options. New car rates generally fall between 6.6% and 8.1%, with used car rates from 8.8% to 11.6%.

- Hawaii — An island market with fewer lenders, where shipping costs affect vehicle prices. New car APRs typically run 6.7% to 8.2% and used car rates 9.0% to 11.8%.

- Idaho — Moderate competition with credit unions being especially popular. New car rates range from 6.5% to 8.0%, with used car rates from 8.7% to 11.4%.

- Illinois — The large urban Chicago market drives significant competition. New car APRs fall between 6.3% and 7.8%, with used car rates from 8.5% to 11.2%.

- Indiana — A strong manufacturing economy supports a decent credit market. New car rates run 6.4% to 7.9% and used car rates 8.6% to 11.3%.

- Iowa — High credit scores statewide keep rates competitive, with new car APRs of 6.3% to 7.7% and used car rates of 8.4% to 11.0%.

- Kansas — A mid-size market where credit unions are particularly competitive. New car rates range from 6.5% to 8.0% and used car rates from 8.7% to 11.4%.

- Kentucky — An average market where online lenders are growing in popularity. New car APRs typically run 6.7% to 8.2% and used car rates 9.0% to 11.8%.

- Louisiana — A higher-risk market where insurance costs can impact loan approvals. New car rates tend to fall between 7.0% and 8.6%, with used car rates from 9.3% to 12.3%.

- Maine — A small market where credit unions are a good option. New car APRs run 6.5% to 8.0% and used car rates 8.8% to 11.5%.

- Maryland — High incomes and a competitive market near the DC metro area. New car rates generally fall between 6.2% and 7.7%, with used car rates from 8.4% to 11.0%.

- Massachusetts — A strong credit culture with many competitive lenders keeps rates near the top of national rankings. New car APRs run 6.1% to 7.6% and used car rates 8.3% to 10.9%.

- Michigan — As an auto industry hub, manufacturer financing is well established here. New car rates range from 6.4% to 7.9% and used car rates from 8.6% to 11.3%.

- Minnesota — High credit scores statewide and competitive options push rates down. New car APRs fall between 6.2% and 7.7%, with used car rates from 8.4% to 11.0%.

- Mississippi — Lower average credit scores statewide cause lenders to price in more risk. New car rates typically run 7.1% to 8.7% and used car rates 9.5% to 12.5%, among the highest nationally.

- Missouri — A mid-size market with both urban and rural lenders. New car APRs range from 6.5% to 8.0% and used car rates from 8.7% to 11.4%.

- Montana — A smaller market where online lenders are especially helpful. New car rates run 6.6% to 8.1% and used car rates 8.9% to 11.7%.

- Nebraska — Solid credit scores and competitive credit unions characterize this market. New car APRs fall between 6.4% and 7.9%, with used car rates from 8.6% to 11.2%.

- Nevada — Larger urban markets with common dealer finance deals. New car rates range from 6.6% to 8.2% and used car rates from 8.8% to 11.6%.

- New Hampshire — High incomes and a competitive market keep rates favorable. New car APRs run 6.2% to 7.6% and used car rates 8.3% to 10.9%.

- New Jersey — A dense market with many lender options available. New car rates fall between 6.2% and 7.7%, with used car rates from 8.4% to 11.0%.

- New Mexico — A smaller market where online lenders broaden choices considerably. New car APRs range from 6.8% to 8.3% and used car rates from 9.1% to 12.0%.

- New York — A large competitive market with strong borrower protections. New car rates run 6.3% to 7.8% and used car rates 8.5% to 11.2%.

- North Carolina — A growing market with competitive suburban areas. New car APRs fall between 6.4% and 7.9%, with used car rates from 8.6% to 11.3%.

- North Dakota — Low unemployment and good average credit scores keep rates competitive. New car rates range from 6.3% to 7.8% and used car rates from 8.5% to 11.1%.

- Ohio — A large market with diverse lender options. New car APRs run 6.4% to 7.9% and used car rates 8.6% to 11.3%.

- Oklahoma — An average market where energy economy fluctuations can affect credit conditions. New car rates fall between 6.7% and 8.2%, with used car rates from 9.0% to 11.9%.

- Oregon — A competitive market with a strong credit union network. New car APRs range from 6.3% to 7.8% and used car rates from 8.5% to 11.1%.

- Pennsylvania — A large state where urban centers drive competition. New car rates run 6.3% to 7.8% and used car rates 8.5% to 11.2%.

- Rhode Island — A small market with access to New England lending options. New car APRs fall between 6.4% and 7.9%, with used car rates from 8.6% to 11.3%.

- South Carolina — A growing market where online lending is increasingly popular. New car rates range from 6.6% to 8.1% and used car rates from 8.9% to 11.7%.

- South Dakota — No state income tax and a stable credit market. New car APRs run 6.4% to 7.9% and used car rates 8.6% to 11.3%.

- Tennessee — A fast-growing economy with decent lender competition. New car rates fall between 6.5% and 8.0%, with used car rates from 8.7% to 11.5%.

- Texas — One of the most borrower-friendly markets in the country, driven by the sheer scale of the state and fierce lender competition. New car APRs range from 6.4% to 7.9% and used car rates from 8.6% to 11.3%.

- Utah — A fast-growing state with a young borrower base and competitive rates. New car rates run 6.3% to 7.8% and used car rates 8.5% to 11.1%.

- Vermont — A small market where credit unions are particularly strong. New car APRs fall between 6.4% and 7.9%, with used car rates from 8.6% to 11.3%.

- Virginia — High incomes near the DC metro and a competitive lender market make Virginia one of the stronger states for borrowers. New car rates range from 6.2% to 7.7% and used car rates from 8.4% to 11.0%.

- Washington — A strong tech economy supports competitive rates. New car APRs run 6.2% to 7.7% and used car rates 8.4% to 11.0%.

- West Virginia — Lower average incomes push rates toward the higher end nationally. New car rates fall between 7.0% and 8.5%, with used car rates from 9.3% to 12.2%.

- Wisconsin — A strong credit union culture drives competitive rates across the state. New car APRs range from 6.3% to 7.8% and used car rates from 8.5% to 11.1%.

- Wyoming — A small market where online lenders are a practical option for accessing competitive offers. New car rates run 6.5% to 8.0% and used car rates 8.7% to 11.4%.

Disclaimer: APR estimates above are derived from publicly available market data as of 2025. Rates change frequently. Always obtain multiple live quotes from lenders before committing to any loan.

Deep Dive: Regional Auto Loan Rate Trends Across America

The 50-state breakdown tells you where individual states sit. Now let us zoom out and look at regional patterns — because understanding why your region looks the way it does helps you know exactly what to expect and how to respond.

Northeast: America’s Most Borrower-Friendly Region

The Northeast consistently posts the most competitive average auto loan rates in the country, and it is not an accident. This region combines high average household incomes, dense populations (which attract more lenders), strong consumer protection laws, and a culture of competitive banking rooted in long-established financial institutions.

Connecticut, Massachusetts, and New Hampshire regularly appear at the top of national low-rate lists. New York and New Jersey, despite their size and complexity, maintain competitive rates thanks to sheer market volume — when thousands of lenders are competing for millions of borrowers, rates fall. Pennsylvania, Maryland, and Virginia (though Maryland and Virginia are sometimes categorized as Mid-Atlantic) complete a strong northeastern corridor of favorable lending conditions.

If you live in the Northeast and have decent credit, you are in an excellent position. That said, even in low-rate states, using an online platform like CarFix Credit ensures you are comparing offers rather than accepting the first one that arrives — which is always the right move.

Southeast: The Region With the Widest Rate Variation

The Southeast is the most uneven region in the country when it comes to auto loan rates, and understanding why matters if you live here.

On the high end of this region sits Virginia — one of the best-rate states in the entire country, largely because the Washington D.C. metro area drives high incomes and fierce lender competition into Northern Virginia. North Carolina and Tennessee are also improving rapidly as their economies grow and populations expand.

At the other end, Mississippi and Louisiana consistently appear among the highest-rate states nationally. In Mississippi, lower average credit scores statewide push lenders to price in more risk. In Louisiana, unusually high vehicle insurance costs combine with an above-average rate of delinquencies to create a more challenging lending environment. West Virginia and Alabama sit in a similar zone, though both have room for improvement.

For borrowers in high-rate Southeastern states, the most powerful tool available is an online lending platform that gives you access to lenders outside your local market. CarFix Credit operates across all 50 states, which means a borrower in Mississippi is not limited to Mississippi-based lenders — they can access the same national lender network as a borrower in Connecticut.

Florida deserves a special note. It is a massive auto lending market — one of the largest in the country — with genuinely fierce competition among lenders. However, Florida is also home to aggressive dealer financing practices and add-on products (like extended warranties and GAP insurance) that can inflate your effective loan cost. Getting pre-approved before visiting a dealership is especially important in Florida.

Midwest: The Credit Union Belt

The Midwest has a distinctive lending culture built around credit unions. States like Wisconsin, Minnesota, Iowa, and Nebraska have some of the highest per-capita credit union membership rates in the country, and credit unions almost universally offer more competitive auto loan rates than big banks. If you live in the Midwest and are not already a member of a credit union, joining one before applying for your next auto loan is a smart move.

Michigan stands out within the region for a different reason: it is the historic heart of the American auto industry. The legacy of having Ford, GM, and Chrysler headquartered in the state means manufacturer financing programs are well-established here, and dealer financing can sometimes be surprisingly competitive.

Illinois benefits from the Chicago metropolitan area’s density and financial sophistication. Ohio and Indiana are large, stable markets with plenty of lender options. The Great Plains states — Kansas, Nebraska, North and South Dakota — have above-average credit scores driven by low unemployment and stable economies, which helps keep rates competitive despite smaller lender pools.

Southwest: Texas Leads the Way

Texas is the standout borrower-friendly state of the Southwest — and one of the most competitive auto lending markets in the entire country. The sheer scale of the Texas market, with tens of millions of residents and a car-centric transportation culture, creates ferocious competition among lenders. If you are in Texas and not getting multiple quotes, you are almost certainly leaving money on the table.

Arizona and Colorado are also competitive markets, particularly in their major urban corridors (Phoenix, Denver, Tucson). Utah is rapidly becoming more competitive as its population grows and its tech economy attracts higher-income residents.

New Mexico and Oklahoma present more mixed pictures. Both are mid-size markets where economic fluctuations — New Mexico’s dependence on government and military employment and Oklahoma’s exposure to energy price swings — can create variability in lending conditions. Online lenders are especially valuable in these states for ensuring you are not limited to local market rates.

West Coast and Pacific: Strong Markets With Geographic Outliers

California is one of the most powerful auto lending markets on earth. Its combination of a massive population, strict consumer protection laws, high incomes in major metros, and aggressive lender competition creates genuinely excellent conditions for borrowers. The California Department of Financial Protection and Innovation (DFPI) actively regulates auto lending, which keeps dealer practices in check and maintains market integrity.

Oregon and Washington share many of California’s competitive advantages, particularly in the Portland and Seattle metro areas. Both states have strong credit union networks and above-average household incomes.

Hawaii and Alaska are the geographic outliers. Both states experience higher rates due to remoteness — fewer lenders operate in these markets, and the logistics of vehicle transportation (especially in Hawaii, where cars must be shipped) add complexity. For residents of both states, national online lending platforms are especially important for accessing mainland-competitive rates. CarFix Credit’s network is available in both Hawaii and Alaska, giving residents the same access to multiple competing lenders as anywhere on the continental United States.

Bad Credit Auto Loans by State: What You Need to Know

One of the most searched questions among car buyers is: “Can I get an auto loan with bad credit?” The answer is yes — in every state — but how you go about it makes an enormous difference in the rate you receive and the total cost of your loan.

CarFix Credit was built specifically for borrowers who do not fit into the “ideal borrower” box that traditional banks prefer. We understand that a low credit score rarely tells the full story. Medical bills, a period of unemployment, a divorce, a missed payment years ago — these things happen to real people, and they should not permanently lock someone out of vehicle financing.

How Bad Credit Affects Rates Differently by State

For bad credit borrowers, the state you live in matters even more than it does for good-credit borrowers. Here is why: in states with strong consumer protections, even high-risk lenders are constrained by law in how much they can charge. In states with fewer regulatory guardrails, the spread between what a good-credit borrower pays and what a bad-credit borrower pays can be substantially wider.

States where bad credit borrowers tend to face the steepest rates include Mississippi, Louisiana, West Virginia, and parts of the rural South, where a combination of weaker regulatory frameworks and higher underlying default rates pushes lender pricing up.

States where bad credit borrowers can still find relatively workable options include California, Texas, Florida, and much of the Northeast and Midwest — not because bad credit is less expensive there, but because the sheer volume of lenders creates more options at every credit level.

CarFix Credit’s Bad Credit Auto Loan Program

CarFix Credit was designed from the ground up to serve borrowers across the full credit spectrum. There is no minimum credit score required to apply — whether your score is 450 or 750, you can submit an application and see real lender offers. Checking your options through CarFix Credit does not hurt your credit score; a soft inquiry is used for pre-qualification, so you can explore your options risk-free.

Rather than sending you to one lender who may or may not approve you, CarFix Credit matches you with multiple lenders in your state who specialize in your credit tier. Competition among those lenders helps drive your rate down. We also work with lenders who specifically offer second-chance programs for borrowers with bankruptcies, repossessions, or other major derogatory marks on their credit history.

Many CarFix Credit lenders report your on-time payments to the major credit bureaus as well. This means every payment you make on time is actively rebuilding your credit score — turning your auto loan into a credit repair tool.

Real Talk from Our Customers: Over 35% of CarFix Credit borrowers came to us with a credit score below 620. Of those approved, the average credit score improvement after 12 months of on-time payments was 47 points. A better score means a better rate on your next loan — and it starts with getting approved today.

Powersports Vehicle Financing by State: Motorcycles, ATVs, Sea-Doos, and Side-by-Sides

Most auto loan guides stop at four-wheeled passenger vehicles. This one does not — because if you are looking to finance a motorcycle, ATV, personal watercraft like a Sea-Doo, or a side-by-side (UTV), the rules of the game are a little different.

CarFix Credit is one of the few national financing platforms that handles powersports loans with the same streamlined online pre-approval process as standard auto loans. Loan amounts from $5,000 to $75,000, terms from 12 to 96 months, all 50 states, and all credit types — the same core offer, applied to a category that most lenders ignore.

Why Powersports Loans Carry Higher Rates

Powersports vehicles are classified as higher-risk collateral by most lenders for several reasons: their value depreciates more unpredictably than passenger cars, they are used seasonally in most states (which affects resale demand), their buyer pool at auction is narrower, and the buyer is often purchasing a discretionary leisure vehicle rather than a daily commute necessity.

These factors typically push powersports loan rates 1% to 3% above equivalent auto loan rates. A borrower who might get 7.5% on a used car loan might see 9.5% to 11.0% on a Sea-Doo or side-by-side through a traditional lender.

Powersports Financing Rates by Region

Just as with standard auto loans, geography matters for powersports financing. The South and Southeast — Florida, Texas, Georgia, South Carolina, and Tennessee — are the most active powersports markets in the country, particularly for ATVs, side-by-sides, and personal watercraft. More lenders serve these markets, which creates somewhat better rate competition. Florida is particularly strong for Sea-Doo and marine-adjacent financing.

- In the Mountain West and Pacific Northwest — Colorado, Utah, Idaho, Oregon, Washington, and Montana — ATVs, off-road side-by-sides, and snowmobiles dominate the market. Seasonal use is more pronounced here, which lenders factor into their pricing. Credit unions in this region are often the best source for competitive powersports rates.

- In the Midwest — Wisconsin, Minnesota, Missouri, Kansas, Ohio, and Indiana — ATVs and side-by-sides used for farm and ranch purposes can sometimes access better rates through agricultural lending products. CarFix Credit’s lender network includes options for utility-purpose powersports vehicles.

- In the Northeast, shorter riding seasons mean lenders are more cautious about seasonally-used powersports. However, motorcycles — which function as year-round transportation for many Northeast riders — can attract better rates than pure-leisure ATVs.

- Hawaii and Alaska are unique markets. Hawaii is one of the top Sea-Doo and personal watercraft states in the country. Alaska has strong ATV and snowmobile demand. Both states benefit from using a national online platform to access lenders who actively serve these categories.

CarFix Credit finances motorcycles of all styles — street bikes, cruisers, sport bikes, touring bikes, and adventure bikes — along with ATVs and utility quads, side-by-sides and UTVs, Sea-Doos and personal watercraft, and other recreational powersports vehicles. The application process for a powersports loan is identical to applying for a standard auto loan: same form, same fast pre-approval timeline, same multi-lender matching approach.

The Complete List of Vehicles CarFix Credit Finances

One of the things that sets CarFix Credit apart is the breadth of vehicles we can finance. Whether you are buying your first car, upgrading your family SUV, getting a work truck, or treating yourself to a side-by-side for the weekend trails, we have lender options for you.

In the everyday passenger vehicle category, CarFix Credit finances sedans in compact, mid-size, and full-size configurations, as well as SUVs and crossovers, hatchbacks and wagons, light and heavy-duty pickup trucks, minivans and passenger vans, luxury vehicles up to $75,000, electric and hybrid vehicles, and commercial-use light vehicles.

In the powersports and recreational vehicle category, we finance motorcycles of all styles, ATVs and four-wheelers, side-by-sides and UTVs, Sea-Doos and personal watercraft, and other powersports vehicles. Across all categories, loan amounts range from $5,000 to $75,000, loan terms run from 12 to 96 months, and financing is available in all 50 states.

How CarFix Credit’s Online Pre-Approval Process Works

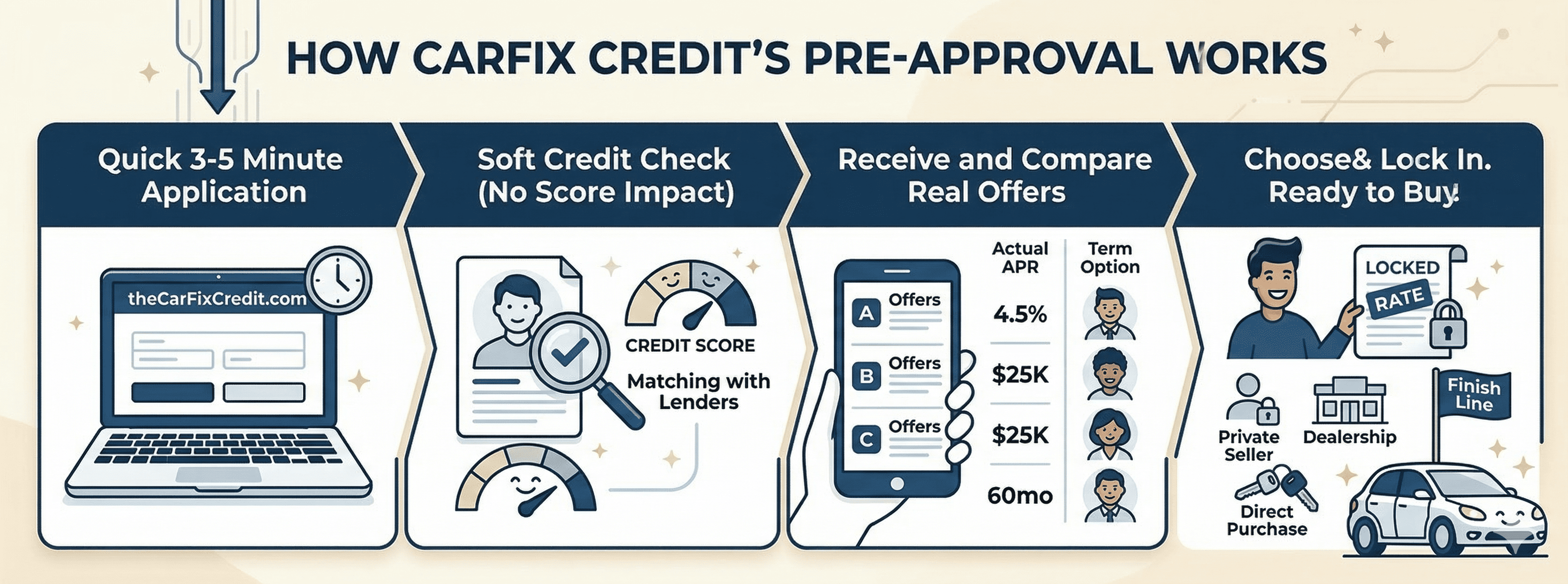

One of the most effective things any car buyer can do — in any state, at any credit level — is get pre-approved for financing before they ever step foot on a dealer lot or commit to a purchase. Pre-approval puts you in control of the conversation and prevents you from being quoted a rate based on whatever deal the dealer wants to make that day.

The process is straightforward. First, you visit carfixcredit.com and fill out the secure online application, which takes about three to five minutes. We then perform a soft credit check that does not impact your credit score and match your profile to lenders in our network. You receive real offers from multiple lenders — with actual APRs, loan amounts, and term options. From there, you compare your offers and choose the one that works best for your budget and timeline. Once you lock in your rate, you can move forward with your purchase at a dealership, through a private seller, or directly.

Most CarFix Credit customers receive their pre-approval results within minutes. In some cases, same-day funding is available. Our team of financing specialists is also available to walk you through your options, explain the fine print, and help you make the choice that is right for your specific situation.

The entire process was designed for real people with real lives — not for people with perfect credit and unlimited time to shop around. If you have ever felt frustrated, confused, or rejected by the traditional auto financing process, we built CarFix Credit for you.

Frequently Asked Questions About Auto Loan Rates by State

What state has the lowest auto loan rates?

Connecticut, Massachusetts, and New Hampshire consistently rank among the lowest-average-rate states in the country. This is driven by high average household incomes, strong consumer protection laws, and competitive lending markets. Maryland, Virginia, California, and Washington are also frequently in the top tier. That said, in-state rates only matter if you are using a local lender — national online platforms like CarFix Credit bring competitive rates from across the country to borrowers in every state.

What state has the highest auto loan rates?

Mississippi, Louisiana, West Virginia, and parts of rural Alabama and Arkansas tend to show the highest average rates. These states combine lower average credit scores, weaker consumer protection frameworks, and smaller lender pools — all factors that push rates up. However, even borrowers in these states can access better rates by using an online platform with a national lender network rather than relying solely on local institutions.

Can I get an auto loan with a 500 credit score?

Yes. CarFix Credit works with lenders who specifically serve borrowers in the subprime and deep subprime credit tiers, including scores as low as 500 or below. Your rate will be higher than what a good-credit borrower receives, but approval is possible — especially if you have stable income, a meaningful down payment, or a co-signer. Getting approved and making on-time payments also helps rebuild your credit score over time, positioning you for better rates in the future.

Can I finance a motorcycle or ATV through CarFix Credit?

Yes. CarFix Credit finances a wide range of vehicles including motorcycles (all styles), ATVs, side-by-sides, Sea-Doos and personal watercraft, as well as standard passenger cars, trucks, SUVs, hatchbacks, and vans. Loan amounts from $5,000 to $75,000, terms from 12 to 96 months, all 50 states, and all credit types. Powersports loans typically carry slightly higher rates than standard auto loans, but CarFix Credit’s lender network includes powersports specialists who offer more competitive terms than general lenders.

How much does my state of residence actually affect my rate?

Your state can affect your rate by as much as 2% to 3% compared to the national average. On a $30,000 loan over 60 months, that difference amounts to roughly $1,800 to $2,700 in additional interest paid over the life of the loan. However, the effect of your credit score and lender choice is even larger — which is why shopping through a multi-lender platform in any state is more impactful than simply being in a “good” state.

Does applying to multiple lenders hurt my credit score?

Not significantly, and not if done correctly. The major credit bureaus treat multiple auto loan inquiries within a 14- to 45-day window as a single inquiry for scoring purposes, recognizing that comparison shopping is a normal and healthy consumer behavior. CarFix Credit’s pre-qualification process uses a soft inquiry that does not affect your score at all — a hard inquiry only occurs when you formally accept and finalize a loan offer.

What is the difference between APR and the interest rate on a car loan?

The interest rate is the base cost of borrowing — the percentage applied to your principal balance to calculate monthly interest. The APR (Annual Percentage Rate) is a broader measure that includes the interest rate plus any lender fees, origination charges, or other costs built into the loan. APR gives you a more complete picture of what you are actually paying. Always compare loans using APR rather than just the stated interest rate.

What loan amounts does CarFix Credit offer?

CarFix Credit facilitates loan amounts ranging from $5,000 to $75,000. This range covers everything from affordable used cars and powersports vehicles at the lower end to luxury vehicles and high-end trucks at the upper end. The maximum amount you qualify for depends on your credit profile, income, and the vehicle being financed.

How long does the pre-approval process take?

Most CarFix Credit applicants receive pre-approval results within minutes of submitting their application. In some cases, same-day funding is available. The application itself takes approximately three to five minutes to complete online. There is no paperwork to mail, no in-person appointment required, and no waiting days for a phone call — everything happens online, on your schedule.

Can I get approved if I have had a bankruptcy or repossession?

Yes. CarFix Credit works with lenders who offer second-chance financing programs specifically designed for borrowers with bankruptcies (including recent Chapter 7 or Chapter 13 filings), prior repossessions, or other significant derogatory marks. Approval is not guaranteed for every borrower in every situation, but we have helped many customers with these backgrounds find workable financing. A larger down payment and stable current income both significantly improve approval odds in these cases.

How do CarFix Credit’s loan terms work?

CarFix Credit offers loan terms from 12 months to 96 months. Shorter terms reduce total interest cost but increase monthly payments. Longer terms lower monthly payments but result in more interest paid overall. Our platform shows you the full cost comparison for different term lengths so you can make an informed decision rather than just chasing the lowest monthly payment.

Ready to Find Your Best Rate? Get Pre-Approved with CarFix Credit Today

You have just finished one of the most comprehensive guides to auto loan rates by state available anywhere. You understand why rates vary, where your state sits in the national picture, how your credit score and vehicle type affect your offer, and exactly what strategies will get you the best deal.

Now it is time to act on that knowledge.

CarFix Credit is a US-based auto financing platform headquartered in Miami, Florida. Since our founding, we have helped over 183,000 Americans across all 50 states secure vehicle financing — quickly, with minimal hassle, and with real transparency about terms and total cost. We built this company for the borrowers who were not being served well by traditional lenders: people with imperfect credit, first-time buyers, buyers who want to finance a powersports vehicle, and anyone who just wants to see all their options at once rather than accepting the first offer that comes along.

CarFix Credit serves all 50 states — from California to Maine, Alaska to Florida. We welcome all credit types, including excellent credit, bad credit, no credit, and recent bankruptcy. We finance the full range of passenger and commercial vehicles, as well as motorcycles, ATVs, Sea-Doos, and side-by-sides. Loan amounts range from $5,000 to $75,000, with flexible terms from 12 to 96 months. Pre-approval results arrive in minutes, with no impact to your credit score to check offers — soft inquiry only for pre-qualification. And with more than 183,000 Americans already helped, you are in good company.

Apply Now — It Takes Less Than 5 Minutes

www.carfixcredit.com

No hard credit pull to see your offers. No paperwork. No waiting. Loans from $5,000 to $75,000 | 12 to 96 Months | All 50 States | All Credit Types

Or call us toll-free to speak with a CarFix Credit financing specialist.

CarFix Credit — Helping Americans Drive Forward, One Loan at a Time.

Disclaimer: All APR ranges and rate estimates in this article are based on publicly available market data as of 2025 and are provided for general informational and educational purposes only. Actual rates vary based on individual credit profiles, lender underwriting criteria, vehicle type, loan term, down payment, and current market conditions. CarFix Credit does not guarantee any specific rate or approval outcome for any individual borrower. Always consult directly with lenders for current, personalized rate quotes. CarFix Credit is a loan-matching platform; it is not a bank or direct lender.