")

What Documents Do You Need to Apply for a Car Loan?

Carfixcredit | Updated April 2026 | 7 min read

One of the most common reasons a car loan application stalls isn’t credit. It’s missing paperwork.

Knowing exactly what documents you need to apply for a car loan before you start the process means no delays, no last-minute scrambles, and no sitting at a dealership finance desk while someone waits for you to find something on your phone.

The list isn’t long. But having everything ready before you apply makes the difference between a smooth process and a frustrating one.

Why Lenders Ask for Documents

Before we get into the list, it helps to understand what lenders are actually trying to confirm.

Three things. Who you are, whether you can afford the payment, and whether the information you provided on the application matches reality.

Every document on this list serves one of those three purposes. Once you understand why each one is asked for, the list stops feeling like bureaucracy and starts making sense as a straightforward verification process.

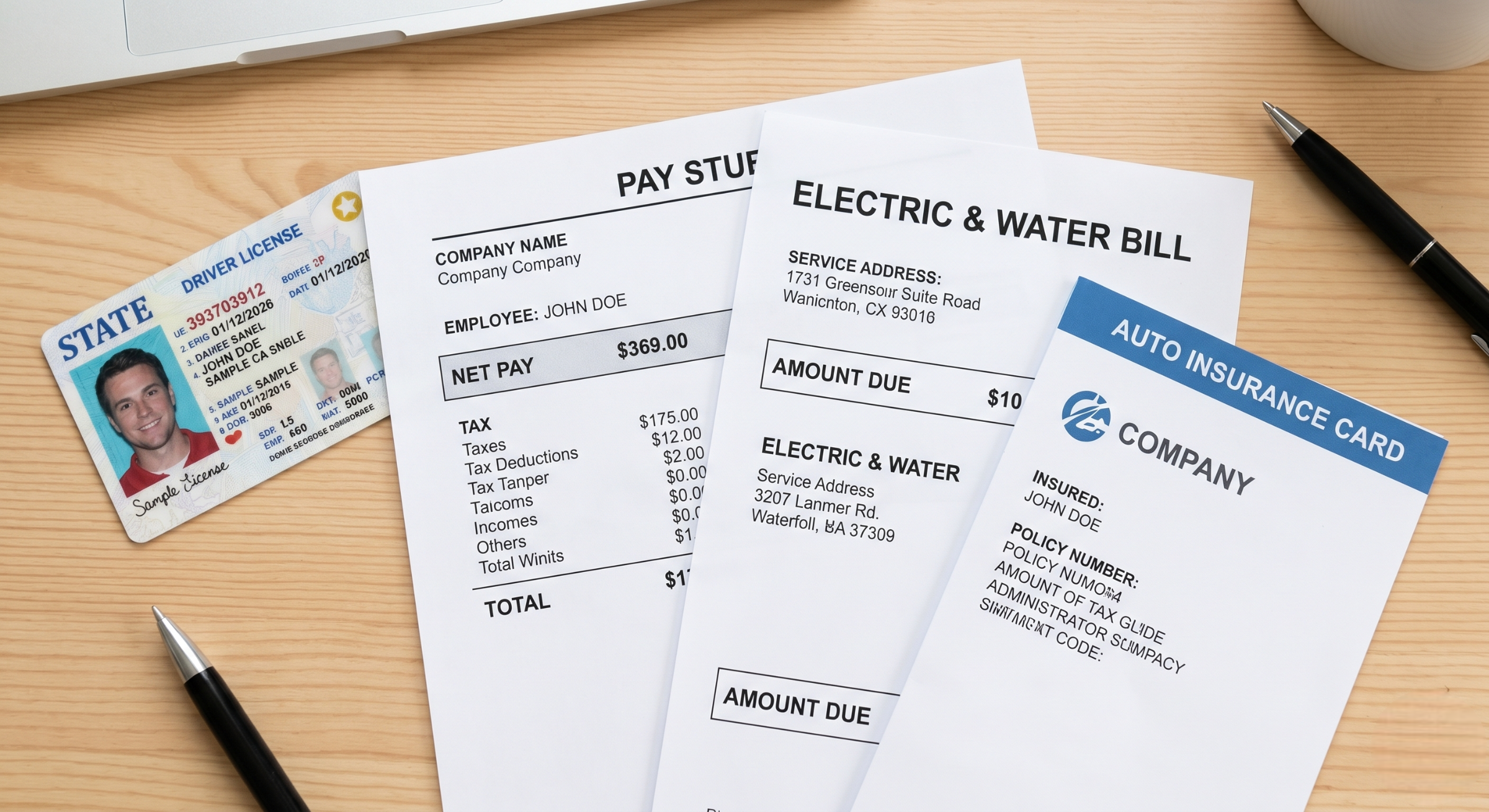

1. Proof of Identity

Lenders need to confirm you are who you say you are. A government-issued photo ID is standard across all lenders.

A valid driver’s license is the most commonly used document here and the most practical one since you’ll need it to drive the vehicle anyway. A passport works equally well if your license isn’t current.

Make sure your ID isn’t expired before you apply. An expired license creates an unnecessary delay that’s easily avoided.

If you’re not a US citizen, a valid visa or permanent resident card alongside your passport is typically what lenders require. The specific documents accepted vary by lender so it’s worth confirming before you apply.

2. Proof of Income

This is the document set lenders look at most carefully after your credit score. It answers the fundamental question of whether the monthly payment is actually manageable for your situation.

For salaried or hourly employees

Recent pay stubs are the standard. Most lenders want to see the last 30 days, which typically means two to four pay stubs depending on how frequently you’re paid. The pay stub needs to show your employer’s name, your gross income, and the pay period clearly.

Some lenders also ask for a recent bank statement showing the deposits that match your pay stubs. This confirms the income is actually being received rather than just documented on paper.

For self-employed buyers

Self-employment income is harder to verify than a regular paycheck and lenders know it. You’ll typically need two years of federal tax returns, recent bank statements showing consistent deposits, and sometimes a profit and loss statement if your business is structured formally.

The more documentation you can provide showing consistent, verifiable income over time, the stronger your application. Self-employed buyers who’ve been in business for less than two years often face more scrutiny, which makes having clean, organized records even more important.

For buyers with multiple income sources

If you have income from more than one source, document all of it. Part-time work, rental income, freelance work, social security or pension payments. Lenders can only count income they can verify. The more verified income you show, the stronger your debt-to-income ratio looks on the application.

3. Proof of Residence

Lenders want to confirm where you live. This affects which lenders can serve you, helps verify your identity, and is a standard part of the fraud prevention process.

A utility bill, a bank statement, or a lease or mortgage statement showing your name and current address works for most lenders. The document needs to be recent, typically within the last 60 to 90 days.

If you’ve recently moved and your ID still shows your old address, bring both a document showing the old address and one showing the new one. A brief explanation of the recent move smooths this over quickly.

4. Proof of Insurance

Most lenders require you to have auto insurance in place before they’ll finalize a loan. The vehicle serves as collateral for the loan and the lender needs to know it’s protected.

You don’t necessarily need to have the specific vehicle insured before you apply, but you’ll need proof of coverage before you drive off the lot. Having your existing insurance information ready speeds up this part of the process.

If you’re purchasing your first vehicle, get insurance quotes before you finalize the purchase. Your insurance carrier can typically add the new vehicle to a policy and issue proof of coverage quickly once you have the vehicle details.

5. Social Security Number

Your Social Security number is required for the lender to pull your credit report. It’s also used to verify your identity against federal databases as part of the standard fraud prevention process.

Most applications ask for this upfront on the form itself. Have it ready rather than needing to look it up mid-application.

If you don’t have a Social Security number, an Individual Taxpayer Identification Number, or ITIN, is accepted by some lenders. Not all lenders accept ITINs so it’s worth confirming with the specific lender before you apply.

6. Employment Information

Beyond income documentation, lenders typically ask for basic employment details directly on the application. Your employer’s name, address, and phone number, how long you’ve been employed there, and your job title or role.

Employment stability is a meaningful signal to lenders. Two years or more with the same employer is viewed favorably. Recent job changes aren’t automatically a problem but they can prompt additional questions about income consistency.

If you recently changed jobs, be prepared to explain the transition and document that the income level is stable or higher than your previous position.

7. Vehicle Information

If you’re applying with a specific vehicle in mind, having the vehicle details ready moves the process along. The make, model, year, VIN, mileage, and purchase price are the key details most lenders ask for.

For a new vehicle from a dealership, this information appears on the window sticker or buyer’s order. For a used vehicle from a private seller, the title and the seller’s listing typically contain everything you need.

Some lenders, particularly those you approach for pre-approval before you’ve chosen a vehicle, will approve you for a loan amount first and ask for vehicle details later when you’ve found the right car. In that case, you can skip this document set until you’re ready to finalize the purchase.

8. Down Payment Documentation

If you’re making a down payment, lenders need to know the funds are real and accessible. A recent bank statement showing sufficient funds in the account is typically enough.

If part of your down payment is coming from a trade-in, the lender will assess the trade-in value as part of the loan structure. Having the title for your trade-in vehicle ready speeds up that part of the process.

For buyers using a gift as part of a down payment, some lenders require a gift letter confirming the funds are a gift rather than a loan that would affect your debt-to-income ratio.

9. References

Some lenders, particularly those working with buyers who have challenged credit or no credit history, ask for personal or professional references as part of the application.

Typically two or three references with their names, relationship to you, phone numbers, and how long you’ve known them. Let your references know they may receive a call so they’re not caught off guard.

This isn’t standard across all lenders but it’s common enough in the subprime lending market that having a short list of contacts ready is worth doing before you apply.

10. Co-Signer Documentation

If you’re applying with a co-signer, they’ll need to provide most of the same documentation as the primary borrower. Proof of identity, proof of income, Social Security number, and employment information.

The co-signer should have all of this ready before the application starts. An incomplete co-signer application creates the same delays as an incomplete primary application.

Organizing Before You Apply

Taking 20 minutes to pull everything together before you start an application is one of the most practical things you can do.

Go through the list, gather what you have, and identify anything missing. A pay stub you need to download from your employer’s portal, an insurance card that needs to be renewed, a utility bill at an address that doesn’t match your ID. Better to find the gap before you’re sitting in a finance office than during the application itself.

If you’re applying online, having documents scanned or photographed clearly on your phone before you start means you can upload them immediately rather than stopping to find them mid-application.

Getting pre-approved for a car loan before you visit a dealership is easier when your documents are already organized. The pre-approval process uses most of the same information and having it ready means you can complete the application in one sitting.

Documents for Specific Situations

Buying from a private seller

Private party purchases sometimes require additional documentation because there’s no dealership involved in the transaction. You may need a bill of sale signed by both buyer and seller, the vehicle title showing the seller’s ownership, and sometimes a vehicle history report confirming the car’s background.

Recent bankruptcy

If you’ve been through a bankruptcy, lenders may ask for the discharge paperwork confirming the bankruptcy is complete rather than ongoing. Having this ready prevents a delay while the lender waits for documentation.

Recent address change

If your ID and your current utility bills show different addresses, bring documentation for both and a brief explanation. A lease agreement at your new address alongside your old-address ID is a straightforward way to handle this.

The Bottom Line

The document list for a car loan application is manageable. None of it is hard to gather. The only thing that makes it stressful is trying to find everything at the last minute under pressure.

Pull the list together before you apply. Know what you have and what you need to locate. Then the application itself becomes a formality rather than a scramble.

Prepared buyers move faster through the process, encounter fewer delays, and often make a better impression on lenders who see organized documentation as a signal of reliability.

How Carfixcredit Makes the Application Process Simple

Whether your credit is strong, challenged, or you’re applying for the first time, Carfixcredit connects buyers across the United States with lenders who work with real financial situations.

Checking what you qualify for takes about two minutes and won’t affect your credit score. Once you know your options, the full application process is straightforward with your documents ready to go.