")

How to Refinance Your Auto Loan to Lower Your Rate

Carfixcredit | Updated April 2026 | 8 min read

A lot of people sign an auto loan and never look at it again until it’s paid off.

That approach costs some of them real money.

If your credit has improved since you financed your vehicle, if interest rates have dropped, or if you accepted a higher rate because you were in a hurry to get into a car, refinancing your auto loan could reduce your monthly payment, lower your total interest cost, or both.

The process is simpler than most people expect.

This guide covers when it makes sense, how to do it, and what to watch for so you end up with a deal that actually improves your situation.

What Refinancing Actually Does

Refinancing replaces your existing auto loan with a new one. The new loan pays off the old one and you start making payments to the new lender at the new terms.

The goal is a lower interest rate, which reduces the total interest you pay over the remaining life of the loan. Depending on the rate difference and what’s left on your balance, the savings can range from modest to significant.

Refinancing can also change your loan term. Shortening it means you pay less interest overall and own the vehicle outright sooner. Extending it means a lower monthly payment but more total interest. Which direction makes sense depends on whether your priority is monthly cash flow or total cost.

When Refinancing Makes Sense

Not every situation calls for a refinance. Here’s when it typically makes sense to pursue one.

Your credit score has improved

This is the most common and most compelling reason to refinance. If you financed with challenged credit and have since built a consistent payment history, your score has likely moved. A score that’s improved by 40 or 50 points since your original loan can translate to a rate reduction of several percentage points on a refinance.

Even a modest improvement, 20 to 30 points, is worth checking. The rate difference at different credit tiers is meaningful enough that the math often favors refinancing even with a smaller score improvement.

You got a higher rate than you should have

It happens more often than it should. Buyers in a hurry, buyers who didn’t know their pre-approval options, buyers who accepted dealer financing without comparing it to anything, sometimes end up with a rate that’s higher than their credit profile actually warranted.

If your current rate feels high relative to what you know your credit score should qualify for, refinancing is worth looking into regardless of how long ago you took out the loan.

Interest rates have dropped broadly

Rates move with broader market conditions. If you financed during a period of elevated rates and the market has come down since then, refinancing at the current environment can produce real savings even if your credit hasn’t changed.

You want to change your loan term

If your financial situation has improved and you want to pay the loan off faster, refinancing into a shorter term is a clean way to do it. If your monthly payment has become a strain, extending the term through a refinance can reduce it, though you’ll pay more in total interest over the extended period.

When Refinancing Doesn’t Make Sense

A few situations where the math or the timing works against you.

You’re close to paying off the loan

If you’re in the last 12 months of a loan, refinancing rarely makes financial sense. The interest on most auto loans is front-loaded, meaning you pay proportionally more interest early in the loan than late. By the time you’re near the end, most of what’s left in your payments is principal. The savings from a lower rate on a small remaining balance won’t offset the administrative hassle and any fees involved.

Your car is significantly underwater

If you owe considerably more than the vehicle is worth, refinancing can be complicated. Lenders typically won’t refinance a loan where the balance significantly exceeds the vehicle’s current value because the collateral doesn’t support the loan amount. Bringing the LTV into a more balanced range before attempting a refinance makes the process smoother.

Your credit has gotten worse since the original loan

Refinancing into a higher rate than your current loan isn’t the outcome you’re after. Check your current rate against what you’re likely to qualify for now before you apply. If your credit has declined, waiting until it improves again makes more sense than locking in a worse rate.

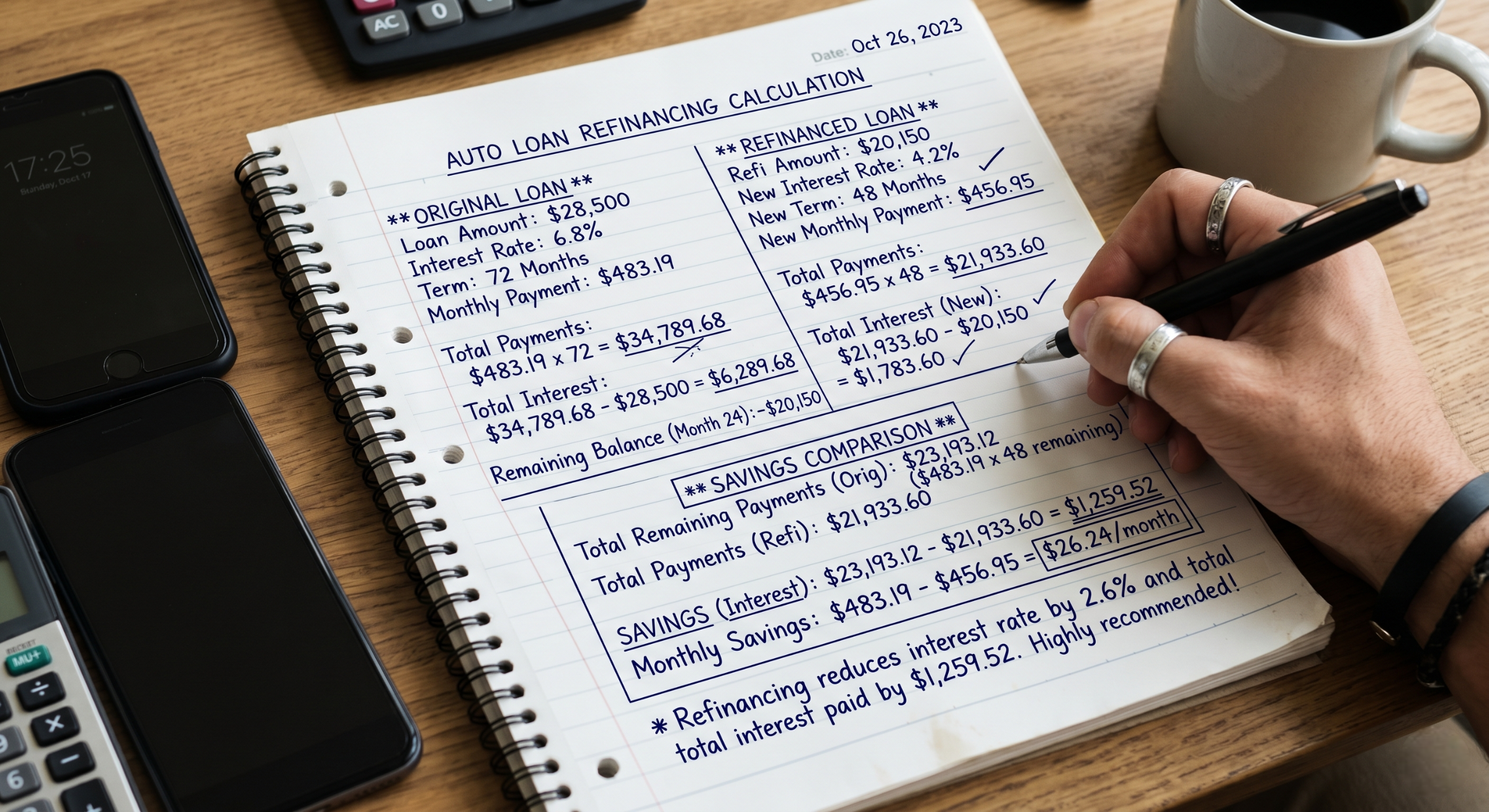

How Much Can You Actually Save?

Here’s a concrete example to make the savings real.

Original loan: $20,000 at 14 percent over 60 months. You’ve made 18 payments. Remaining balance is approximately $14,800. Monthly payment is roughly $465.

Refinanced loan: $14,800 at 8 percent over the remaining 42 months. Monthly payment drops to approximately $401. Total interest on the remaining balance drops from around $4,100 to approximately $2,000.

That’s about $2,100 in interest saved and $64 less per month from a 6 percentage point rate reduction on the remaining balance. The actual numbers depend on your specific situation but the direction is consistent. A meaningful rate reduction on a meaningful remaining balance produces meaningful savings.

Step-by-Step: How to Refinance Your Auto Loan

Step 1: Check your current loan details

Pull out your original loan agreement or log into your lender’s account portal. You need to know your current interest rate, remaining balance, remaining term, and whether there are any prepayment penalties.

Most auto loans don’t have prepayment penalties but some do, particularly in the subprime market. A prepayment penalty means you’ll owe an additional fee for paying off the loan early. Factor that into your calculation before you proceed.

Step 2: Check your credit score

Know where your score sits before any lender pulls it. Free monitoring through credit card providers and apps gives you a current read. If your score has errors dragging it down, dispute them before you apply for a refinance.

The goal is to know approximately what rate you should qualify for so you can evaluate any offers you receive against a reasonable expectation.

Step 3: Find out what your vehicle is worth

Lenders care about loan-to-value on a refinance just as they do on an original loan. Knowing your vehicle’s current market value tells you whether the LTV will support a refinance before you start the application process.

Free tools like Kelley Blue Book and Edmunds give you a reasonable estimate based on make, model, year, mileage, and condition. If your remaining balance is significantly above the vehicle’s current value, that’s worth addressing before you apply.

Step 4: Shop across multiple lenders

This is where most of the savings actually come from. Different lenders offer different rates for the same credit profile. Checking across a bank, a credit union, and an online lending platform gives you a real comparison rather than accepting the first offer you see.

Multiple refinance applications within a short window are treated as a single inquiry by the credit bureaus for scoring purposes. Shop actively within a 14 to 45 day window without worrying about stacking hard inquiries.

Comparing refinance rates across multiple lenders before you commit to any one of them is the most reliable way to find the best available rate for your specific situation.

Step 5: Calculate the actual savings

Once you have a refinance offer, run the math on what it actually saves you rather than just comparing monthly payments.

Take the new monthly payment and multiply by the remaining months. Subtract the original monthly payment multiplied by those same months. The difference is your monthly savings over the life of the loan.

Then compare total remaining interest under the current loan versus total interest under the refinanced loan. The difference is your total savings. Subtract any refinancing fees to get your net benefit.

If the net benefit is positive and meaningful, proceed. If the savings are marginal or the math doesn’t work out after fees, it may not be worth the effort.

Step 6: Apply and finalize

Once you’ve chosen the best offer, complete the formal application. You’ll typically need your driver’s license, proof of income, proof of insurance, your current loan account number, and the vehicle’s title or registration.

The new lender pays off your existing loan directly. Your old account closes. You start making payments to the new lender at the new terms.

The whole process from application to finalization typically takes a few days to two weeks depending on the lender.

How Long Should You Wait Before Refinancing?

Most lenders require at least 60 to 90 days of payment history on your current loan before they’ll consider a refinance application. Some prefer six months.

The practical sweet spot for most buyers is 12 to 18 months into the original loan. By that point you’ve built enough payment history to demonstrate reliability, your credit score has had time to reflect the positive impact of consistent payments, and there’s still enough remaining balance to make the interest savings meaningful.

If you financed with challenged credit specifically to build credit history, 12 to 18 months of clean payments is often enough to produce a score improvement that opens the door to meaningfully better refinance terms.

Refinancing After a Bad Credit Auto Loan

This situation deserves specific attention because it’s one of the most financially rewarding refinance scenarios available.

A buyer who took out a subprime auto loan at 16 or 18 percent, made 14 months of on-time payments, and improved their credit score from 580 to 650 in the process is in a genuinely different financial position from when they originally financed.

That credit improvement can translate to a refinance rate 6 to 10 percentage points lower than the original loan. On a remaining balance of $12,000, that’s a significant amount of money in interest savings over the remaining term.

Using a bad credit auto loan to build credit and then refinancing is one of the most practical financial moves available to buyers who couldn’t access standard financing initially.

Set a reminder at the 12-month mark of your current loan to check what refinancing would look like. Many buyers who do this are surprised by how much their options have improved through consistent payments alone.

What to Watch Out For

Fees rolled into the new loan

Some lenders charge origination fees or other processing costs that get added to the new loan balance. These reduce the net savings from refinancing. Make sure you understand the full cost of the new loan, not just the rate, before you finalize.

Extending the term more than you need to

Refinancing into a significantly longer term reduces your monthly payment but increases your total interest paid. If the goal is to save money overall, extending the term works against you. Stick to the remaining term of your current loan or shorter if your budget allows.

Restarting the interest clock unnecessarily

Interest is front-loaded on amortized loans. You pay more interest in the early months and less as the loan matures. Refinancing restarts that cycle on the new balance. A modest rate reduction late in the loan’s life may not produce enough savings to justify restarting the front-loaded interest phase.

Letting the vehicle title get complicated

Your current lender holds a lien on your vehicle title. When you refinance, the new lender pays off the old loan and the lien transfers. In most states this happens smoothly but it’s worth confirming the title transfer process with both lenders before you finalize to avoid administrative delays.

The Bottom Line

Refinancing an auto loan isn’t complicated and for the right buyer at the right time, it produces real savings with relatively little effort.

The core of the decision is simple. If your current rate is higher than what you’d qualify for today, you’re paying more than you need to on a loan that’s already on your books. Refinancing changes that.

Check your score, check your rate, run the math, and if the numbers work, make the call. The buyers who don’t are the ones paying the difference between what they could qualify for and what they accepted the first time, every month, until the loan is paid off.

What to Do Immediately After a Denial

Read the adverse action notice and identify the specific reasons. This is your starting point.

Check your credit report for errors. A denial is a prompt to review what lenders are actually seeing when they pull your report. Something inaccurate on there deserves to be disputed before you apply again.

Assess which reasons are immediately addressable and which require more time. A down payment shortfall can sometimes be solved quickly. A credit score that needs significant improvement takes months. Knowing the timeline helps you decide whether to address the issue before applying again or to approach a different type of lender now.

Don’t apply to multiple lenders in rapid succession without addressing the underlying issue. Stacking denials adds hard inquiries to your report without improving your approval odds. Fix what you can fix first.

Getting pre-approved through a lender that works with your specific credit situation is a better use of your next application than resubmitting to a lender who’s already told you their threshold doesn’t match your profile.

How Carfixcredit Helps With Auto Loan Refinancing

Whether you’re refinancing from a subprime loan after building credit or just looking for a better rate on an existing loan, Carfixcredit connects buyers across the United States with lenders who work with real financial situations across all credit profiles.

Checking what you qualify for takes about two minutes and won’t affect your credit score. Knowing your options before you commit to staying with your current lender is always worth the two minutes.