")

What Credit Score Is Considered Bad for a Car Loan?

Carfixcredit | Updated April 2026 | 7 min read

Bad credit is one of those terms that gets used constantly in auto financing without much explanation of what it actually means in practice.

The honest answer is that bad credit isn’t a single number.

It’s a range, and where you fall within that range determines which lenders will work with you, what rate you’ll pay, and what the path to getting approved actually looks like.

Understanding what credit score is considered bad for a car loan before you apply means no surprises and a much clearer picture of your actual options.

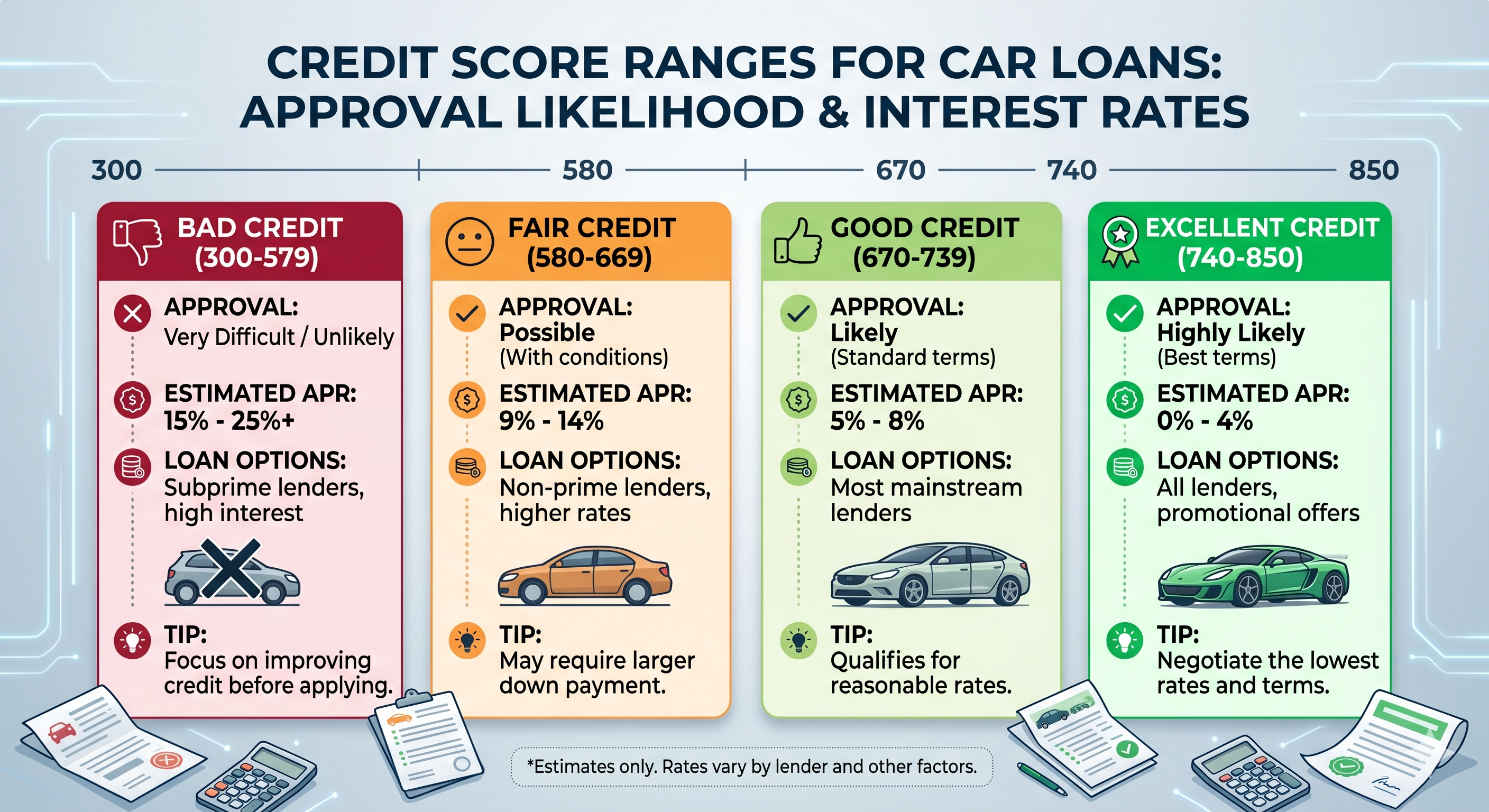

What the Industry Considers Bad Credit

Most auto lenders use credit score thresholds to categorize buyers into tiers. Here’s where bad credit generally falls in that framework.

Scores below 580 are widely considered poor or bad credit by the majority of lenders. At this level, traditional banks and most credit unions are unlikely to approve a standard auto loan application. The lender pool narrows significantly and the rate offered by lenders who will work with this range is considerably higher than what standard credit buyers see.

Scores in the 580 to 619 range sit in what most of the industry calls subprime territory. Some people in this range consider themselves to have bad credit. Technically this tier falls between poor and fair, and while lenders will work with it, the terms are less favorable than buyers in higher tiers see.

Scores below 500 are often categorized as deep subprime. This is the most restricted range in terms of lender options. Most specialist subprime lenders have minimum score floors somewhere around 480 to 520. Below those floors, buy here pay here dealerships and a small number of deep subprime specialist lenders are the most realistic channels.

The important thing to understand is that none of these ranges mean you can’t get financed. They mean the financing looks different than it does for buyers with stronger credit.

Why the Definition of Bad Credit Varies by Lender

There is no universal threshold that all lenders agree on.

Different lenders draw their lines differently based on their risk appetite, their product offerings, and the markets they serve.

A traditional bank might decline any application below 660. A credit union that serves a specific community might be more flexible for existing members. An independent finance company specializing in challenged credit might actively pursue buyers in the 520 to 580 range. A buy here pay here dealership might not use credit scores at all.

This variation matters because a denial from one lender at one threshold tells you nothing about whether a different lender with a different threshold would approve the same application. It’s one of the most common misconceptions in auto financing and it leads a lot of buyers to assume the market is closed when it isn’t.

What Bad Credit Actually Costs You

This is the part worth understanding clearly before you apply, because the financial impact of a lower credit score is real and significant.

The rate difference between a buyer with excellent credit and one with bad credit on the same vehicle can be 12 to 18 percentage points or more. That difference translates directly into the total cost of the loan.

Here’s a concrete example on a $18,000 loan over 60 months.

At 6 percent the monthly payment is approximately $348 and total interest paid is around $2,860.

At 14 percent the monthly payment climbs to approximately $419 and total interest reaches around $7,120.

At 20 percent the monthly payment rises to approximately $476 and total interest hits approximately $10,580.

That’s a difference of roughly $7,700 in total interest between a good credit rate and a bad credit rate on the same vehicle. The car doesn’t change. The financing cost does.

Knowing this going in helps you make realistic decisions about vehicle price, loan term, and whether to take steps to improve your score before applying.

The Credit Score Ranges Explained for Auto Financing

300 to 499: Very Poor

The lowest range on the standard scoring scale. Approval through traditional channels is unlikely. Buy here pay here and deep subprime specialist lenders are the most realistic paths. Approval almost always requires a meaningful down payment and verified stable income as compensating factors.

500 to 579: Poor

Widely considered bad credit by most lenders. Standard banks and credit unions are largely inaccessible at this level. Independent finance companies who specialize in subprime lending are your primary options. Rates are high but approval is genuinely possible with the right lender and appropriate deal structure.

580 to 619: Subprime

The upper portion of what’s generally considered bad or challenged credit. More lender options than the tier below but still well outside standard financing territory for most banks. Specialist lenders can work with this range and the rate, while elevated, is typically lower than what buyers below 580 see.

620 to 659: Near Prime

This is the transition zone. Some buyers in this range qualify for near-standard financing through certain lenders. Others still need specialist channels. The variation in what’s available at this level makes shopping across multiple lenders particularly important.

660 and Above: Standard Credit Territory

Above 660 and most buyers are in standard or prime financing territory. The bad credit conversation largely ends here and the focus shifts to finding the best available rate within a competitive lender market.

What Lenders Look at Beyond the Score

A bad credit score makes getting approved harder but it doesn’t end the conversation because credit score is only one input in most lender’s decisions.

Income stability

A consistent, verifiable income tells the lender the monthly payment is manageable regardless of what the credit history looks like. Stable employment history, even if it’s relatively recent, works meaningfully in your favor. The lower your credit score, the more weight income verification carries in the underwriting.

Down payment

Money down reduces the lender’s risk immediately. For bad credit buyers, a down payment is one of the most effective compensating factors available. Even a modest amount, 10 to 15 percent of the vehicle price, can change the terms offered or make the difference between an approval and a decline in borderline situations.

Debt-to-income ratio

How much of your monthly income is already committed to existing debt payments matters alongside the credit score. A buyer with a low score but manageable existing debt is in a different position from one with a low score and payments already stretching their income.

Co-signer

A co-signer with stronger credit is one of the most powerful tools available to a bad credit buyer. The lender evaluates both profiles and the stronger credit history carries significant weight. Both parties need to understand fully what the co-signer responsibility means before anyone signs.

Can You Get a Car Loan With Bad Credit?

Yes. This is the part most buyers in this situation need to hear clearly.

Bad credit makes financing more expensive and limits which lenders will work with you. It does not make financing impossible. The subprime auto lending market exists specifically for buyers who don’t qualify for standard financing, and it’s a well-developed market with multiple lender options at most credit levels above 500.

Below 500 the options narrow significantly but they don’t disappear entirely. Buy here pay here dealerships and a small number of deep subprime specialist lenders operate in this space specifically because the need for transportation doesn’t disappear just because someone’s credit score is very low.

The key is approaching the right lenders for your actual score rather than applying through channels designed for buyers with stronger credit and treating repeated declines as evidence that approval isn’t possible.

How to Improve Your Position Before You Apply

If you have some time before you need a vehicle, a few specific actions can move your score meaningfully.

Check your credit report for errors before you do anything else. Mistakes on credit reports are more common than most people realize. A payment incorrectly reported as late, an account that doesn’t belong to you, or a closed account still showing as open can all drag your score down without reflecting your actual credit behavior. Disputing errors is free and a correction can produce a visible improvement within one to two billing cycles.

Pay down credit card balances where possible. Reducing your credit utilization ratio has one of the fastest effects on your score of any action available. Getting a card from 80 percent utilization down to 40 percent can produce a meaningful improvement within a billing cycle or two.

Make every payment on time from this point forward. Payment history is the single biggest factor in your credit score. A pattern of on-time payments over several months before you apply demonstrates current behavior that some lenders weigh alongside the historical marks on your report.

Even moving from 560 to 590, or from 590 to 620, can open different lender options and produce a meaningfully lower rate. Small score improvements compound into real dollar savings over the life of a loan.

What to Do If You Need a Car Now

Sometimes waiting isn’t an option. If you need a vehicle before you’ve had time to improve your score, here’s the practical path.

Find out your actual score before you apply anywhere. Free monitoring through credit card providers and apps gives you a current read. Knowing the number tells you which lenders to approach and what rate range to expect.

Focus your applications on lenders built for your credit tier. An independent finance company that specializes in subprime lending is a better first call than a bank whose minimum threshold is 100 points above your current score. Routing to the right channel saves hard inquiries and gets you to an answer faster.

Keep the vehicle price reasonable. A more modest vehicle at a higher rate is a more manageable financial position than an expensive vehicle at the same rate. Keeping the loan amount in a range that fits your income makes the monthly payment more workable and the approval more straightforward.

Have a down payment ready if you can. Even a few hundred dollars changes the conversation with some lenders. If you have a vehicle to trade in, that equity counts too.

Getting pre-approved through a lender that works with bad credit before you visit a dealership gives you a clear budget and something to compare any dealer offer against.

Using a Bad Credit Car Loan to Improve Your Score

This is worth understanding because it changes the frame around what a bad credit auto loan actually is.

A subprime auto loan, managed well, isn’t just a way to get a car. It’s a structured opportunity to rebuild the credit score that’s making everything more expensive right now.

Every on-time payment gets reported to the credit bureaus. Over 12 months of consistent payments, most buyers with bad credit see meaningful score improvement. Over 18 to 24 months, many have moved into a range where refinancing at a significantly lower rate becomes possible.

The higher rate on a bad credit loan is the cost of access to that credit-building opportunity. Buyers who treat the loan that way, making every payment on time and planning to refinance once the score improves, consistently end up in a better financial position than they were when they started.

Set up autopay immediately so nothing gets missed. Check your score every few months to track the progress. And set a reminder at the 12-month mark to check what refinancing would look like. Many buyers are surprised by how much their options have improved through consistent payments alone.

The Bottom Line

Bad credit for a car loan is generally a score below 580, though the definition varies by lender. It makes financing more expensive and limits which lenders will work with you. It doesn’t make financing impossible.

Know your score, approach the right lenders for your actual profile, keep the vehicle price realistic, and have a plan to refinance once your credit has improved. That approach consistently produces better outcomes than applying through channels that aren’t built for your situation and treating the resulting declines as a final answer.

How Carfixcredit Helps Bad Credit Buyers Get Approved

Whether your score is in the 500s, the low 600s, or somewhere in between, Carfixcredit connects buyers across the United States with lenders who work with real credit situations including bad credit, limited history, and previous declines.

Checking what you qualify for takes about two minutes and won’t affect your credit score. Finding out where you actually stand is always better than assuming the answer is no.