")

Buy Here Pay Here vs. Traditional Financing for Bad Credit

Carfixcredit | Updated April 2026 | 9 min read

If your credit’s been through it and you’re trying to get a car, you’ve probably run into both options. The traditional dealership that says they can finance you through “their lenders.” And the buy here pay here lot down the road with the big “We Finance Everyone” sign out front.

They sound similar. They’re not. And the difference between them can mean thousands of dollars and a very different ownership experience.

This is for anyone trying to figure out which option actually makes sense for their situation. Both are real paths. Bad credit auto loan options exist on both sides. The trick is knowing which one fits where you are right now.

What buy here pay here actually is

Buy here pay here, usually shortened to BHPH, is when the dealer is also the lender. They sell you the car and finance it themselves. You make payments directly to the dealer, not to a bank or finance company.

The model exists because some buyers can’t qualify for any kind of outside financing. Their credit is too low, their income is too thin, or they’ve had recent serious credit damage that even specialist subprime lenders won’t touch. BHPH dealers fill that gap by taking on the full risk themselves.

Because they’re taking on more risk, they charge accordingly. Higher rates. Higher down payments relative to the vehicle. Older inventory. Stricter rules around payments. Sometimes GPS trackers or starter interrupt devices on the cars to make collection easier if you fall behind.

It’s not always a bad deal. For some buyers it’s the only option that exists. But it’s structured very differently from traditional financing, and the differences matter.

What traditional financing for bad credit actually is

Traditional financing for bad credit means a regular dealership selling you a car, with the loan coming from an outside lender. That lender is usually a specialist subprime finance company, sometimes a credit union, occasionally a bank that runs a subprime program.

The dealer makes their money on the car. The lender makes their money on the loan. They’re two separate companies with separate interests, which actually works in your favor in a few ways we’ll get into.

This is what most people think of as “regular” auto financing, just with the loan going to a lender that specializes in credit-challenged buyers instead of a prime bank. The mechanics are the same as any car loan. You apply, the lender reviews, they approve or decline, and if approved, you make payments to them every month.

The key differences, side by side

Here’s where the two paths actually split.

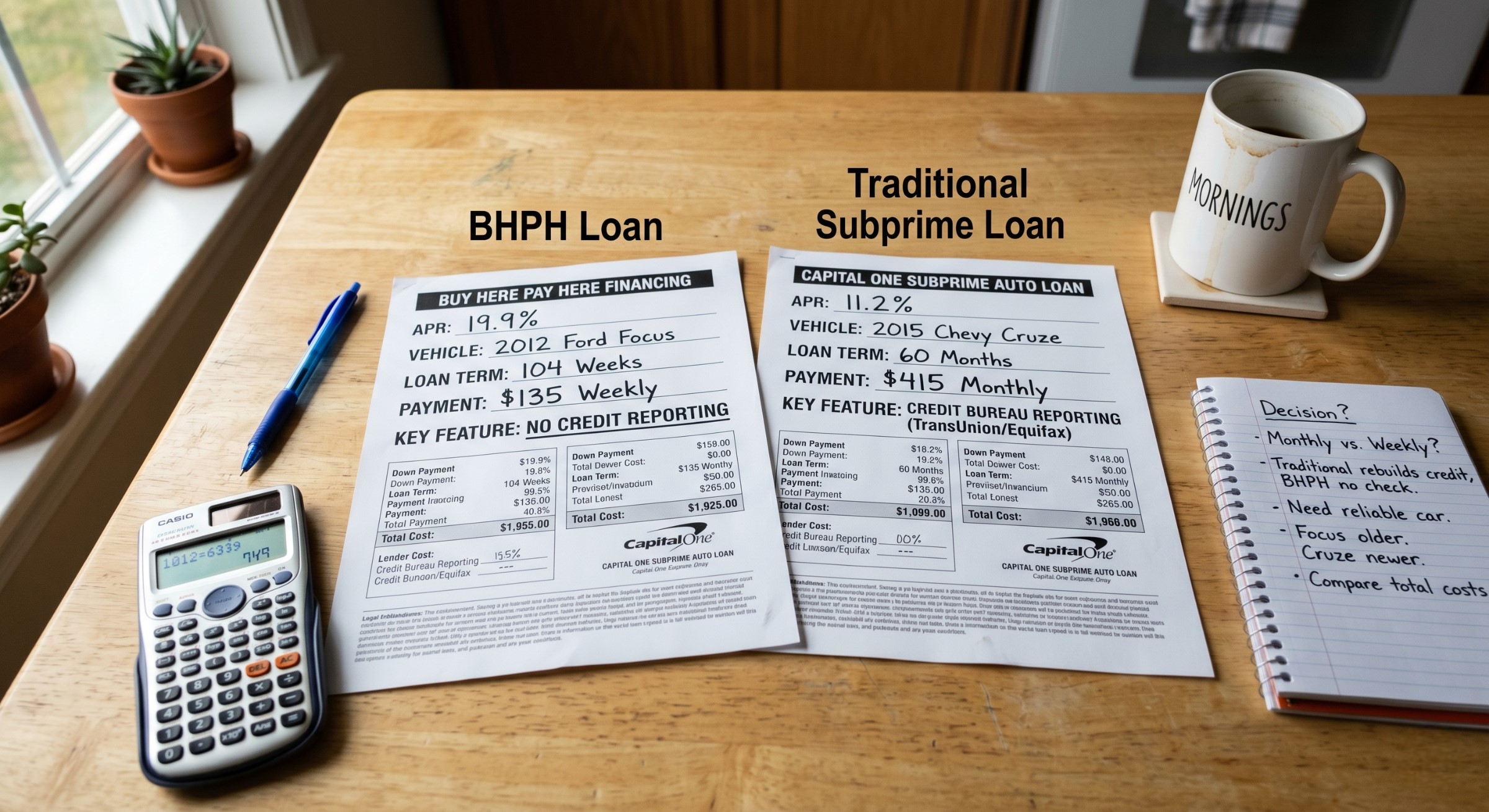

Who holds your loan. With BHPH, the dealer holds the loan. With traditional financing, an outside lender holds it. This matters more than people realize. If you have a problem with your car, the dealer who sold it to you isn’t the same company you’re paying every month, so they have less leverage to pressure you. With BHPH, they’re the same company, and that changes the dynamic.

The interest rate. Traditional subprime loans usually run somewhere between 12% and 22% APR depending on your credit. BHPH loans are often higher, sometimes significantly. Many BHPH dealers charge close to or at the legal maximum allowed in your state, which can be 25% or more. Over a 5-year loan, the difference between 18% and 25% on a $12,000 car is real money.

The down payment. Traditional subprime typically wants 10 to 20 percent down. BHPH often requires similar or higher amounts, sometimes 20 to 30 percent of the vehicle price. The reason is simple: the BHPH dealer is taking on all the risk and uses the down payment to recover costs quickly if the deal goes sideways.

The vehicle. Traditional subprime lenders usually have requirements around vehicle age and mileage. Cars under 8 to 10 years old, under 100K to 120K miles, in solid condition. BHPH inventory is often older, higher mileage, and lower-priced. You’re more likely to find a 2015 sedan with 130,000 miles at a BHPH lot than at a traditional dealer using outside financing.

Credit reporting. This is the one most people miss. Traditional subprime lenders almost always report to the major credit bureaus. Your on-time payments build your credit. Many BHPH dealers don’t report at all, or only report negative activity. That means you can pay on time for three years and your credit score doesn’t move, but if you miss a payment, it can still hurt you.

Payment frequency. Traditional loans are almost always monthly. BHPH loans are often weekly or biweekly, sometimes set up to coincide with your paydays. This isn’t necessarily good or bad, but it’s a different rhythm.

Collection practices. Traditional lenders go through standard collection processes if you fall behind. BHPH dealers have repossession built into their model and often act faster, sometimes within days of a missed payment. Some install starter interrupt devices that can disable the car remotely if you’re late.

When buy here pay here actually makes sense

BHPH gets a bad reputation, but it’s not always the wrong choice. There are real situations where it’s the right path.

You’ve been turned down by every traditional subprime lender. If you’ve tried multiple specialist lenders and nobody will approve you, BHPH might be your only realistic option. A car you can drive is worth more than waiting indefinitely for credit you can’t get.

You need a vehicle immediately and have no time to shop. BHPH lots can often get you in a car the same day with minimal documentation. If your current car just died and you have to be at work tomorrow, that speed has value.

You’re in deep subprime territory with no co-signer available. Buyers with scores under 500, very recent serious credit damage, or active bankruptcy without trustee approval often can’t qualify for traditional financing at all. BHPH is built for this situation.

You have very thin or nonexistent income documentation. Some BHPH dealers are flexible with income verification in ways traditional lenders aren’t. If you’re paid in cash, work seasonal jobs, or have nontraditional income, BHPH might approve where others don’t.

The key in all of these situations is going in with eyes open. The car will cost more than it would through traditional financing. The terms will be stricter. The credit benefit may be limited. None of that automatically makes it wrong, but you should know what you’re agreeing to.

When traditional financing is the better path

For most buyers with bad credit, traditional financing is the better deal if you can qualify. Here’s when it makes the most sense.

You have steady income above $1,800 to $2,000 a month. Most specialist subprime lenders want to see this minimum, and if your income is verifiable and consistent, you usually qualify regardless of how rough your credit looks.

Your bankruptcy is discharged. Once you’re past discharge, especially after 6 months or more, traditional subprime lenders open up significantly. Many will work with you the day after discharge, and the rates are better than BHPH almost always.

You can put 10 to 15 percent down. A real down payment opens up traditional lender options that wouldn’t approve you with nothing down. The rate improvement from having a down payment usually saves more money than the down payment itself costs.

You want your on-time payments to rebuild your credit. This is the big one. Traditional subprime lenders report to credit bureaus, which means every on-time payment is moving your score up. After 12 to 18 months of payments, you can refinance into much better terms. With BHPH, this credit-rebuilding effect often doesn’t happen.

You can wait a few days for approval. Traditional financing isn’t usually as fast as BHPH, but the difference is days, not weeks. If you can hold off on the deal until the lender comes back with an answer, you’ll usually save thousands over the life of the loan.

The credit rebuilding piece

This is the part that changes the math for a lot of buyers, so it’s worth slowing down on.

If you take a traditional subprime loan and pay it on time for 18 months, your credit score will probably go up by 50 to 100 points or more, depending on what else is on your report. That’s enough to refinance into a much better rate. It’s also enough to help with future credit applications, like a credit card, an apartment, or eventually a mortgage.

If you take a BHPH loan that doesn’t report to the bureaus and pay it on time for 18 months, your credit score might not move at all. You’ll have paid off most of a car, but to the credit world, it’s like you didn’t do anything. The next time you go to buy a car, you’re starting from the same place.

This isn’t true of every BHPH dealer. Some do report. The right question to ask before signing is “do you report to the credit bureaus?” If they say no, or if they only report negative activity, that’s a real cost of the deal that doesn’t show up in the rate or the down payment.

For some buyers in dire situations, getting a car at all is more important than rebuilding credit, and BHPH is the right call anyway. But going in knowing this trade-off is the difference between a smart decision and one you regret in a few years.

What to watch for in BHPH deals

If BHPH is the right path for your situation, there are still ways the deal can go wrong. A few things to watch for.

Excessive markup on the vehicle. Some BHPH dealers price their cars well above what they’re actually worth, sometimes double the wholesale value. Check the vehicle’s value through Kelley Blue Book or NADA before agreeing to a price. If it’s significantly above book, that’s a problem.

Hidden fees. Documentation fees, dealer prep fees, processing fees. Some are normal, some are inflated. Read the itemized list and ask about anything you don’t understand.

Aggressive starter interrupt devices. Many BHPH dealers install these now, and the technology itself isn’t necessarily bad. What can be bad is how it’s used. Some dealers disable cars within hours of a missed payment, even if you’re sick or had a banking issue. Ask about the policy specifically and get it in writing.

Vehicle condition issues. BHPH inventory is often older with more wear, which is fine, but some lots sell cars with serious mechanical problems hidden under cosmetic fixes. A pre-purchase inspection from an independent mechanic, usually $100 to $200, can save you thousands.

Forced add-ons. Some BHPH dealers require you to buy their warranty, their gap insurance, their service plan. Some of these have value, some are just more profit for the dealer. If something’s truly required, get a clear written explanation of why.

No grace period on payments. Some BHPH contracts charge late fees the day after a payment is due, with no grace window. Find out what the late payment policy is before signing.

What to watch for in traditional bad credit deals

Traditional financing for bad credit isn’t free of pitfalls either. The big ones to watch for.

Yo-yo financing. This is when the dealer tells you you’re approved, lets you drive the car home, and then calls a week later saying the financing fell through and you need worse terms or more down. Don’t drive a car off the lot until the financing is fully approved, signed, and locked in.

Padded loans. Extras getting rolled into the loan that you didn’t really agree to. Extended warranties, gap insurance, paint protection, theft tracking. Read the itemized list. Decide on each one separately.

Rate markup. Traditional dealers can mark up the rate above what the lender actually approved. Getting pre-approved by a lender directly before you walk in tells you what your real rate should be and protects you from this.

Long terms that don’t fit the car. A 96-month loan on a 7-year-old used car is a setup for being underwater for years. Be cautious of any term over 72 months on a used car.

The smart play for most bad credit buyers

If you’re trying to figure out which path makes sense, here’s the order to think about it.

Start by checking what you qualify for through traditional subprime financing. Auto loan pre-approval through a service like Carfixcredit takes a few minutes, doesn’t affect your credit, and tells you exactly what’s available to you. If you qualify for traditional financing at reasonable terms, take it. That’s almost always the better deal.

If traditional financing comes back with terms that are noticeably worse than what you expected, get a second opinion before assuming BHPH is your only option. A lot of buyers think they’re stuck in BHPH territory when they actually qualify for better.

If you genuinely don’t qualify for traditional financing anywhere, then BHPH is a real option. Just go in with the questions list. Does the dealer report to credit bureaus? What’s the late payment policy? What’s the vehicle actually worth at wholesale? Are there required add-ons? Get the answers in writing before signing.

And whichever path you take, build a refinance plan from day one. Twelve to 18 months of on-time payments rebuilds enough credit to put you in a much better position for the next loan. The first loan after a credit hit is the price of admission. The next one is where you start saving real money.

The bottom line

Buy here pay here and traditional bad credit financing both have their place. Neither is inherently good or bad. They’re different products serving different situations.

For most buyers with steady income and a small down payment, traditional subprime financing is the better deal. Lower rates, real credit reporting, broader vehicle options, and a clean structure that helps you rebuild rather than just survive. For buyers who genuinely can’t qualify anywhere else, BHPH is a real path to a vehicle and a way to keep your life moving while you work on the longer-term credit picture.

The mistake to avoid is assuming you have to use BHPH because someone told you that’s all that’s available, when the reality is you might qualify for something significantly better. Check your real options first. Then make the decision based on what’s actually in front of you.

How Carfixcredit can help you find out what you really qualify for

A lot of buyers walk into BHPH lots because they assume that’s their only option, when traditional subprime financing would actually work for them. The only way to know is to check.

Carfixcredit works with a network of lenders across the United States who handle real-world credit situations every day. Bad credit, no credit, past bankruptcies, recent repossessions, none of these are automatic disqualifiers. The options available are usually broader than people assume going in, and seeing what you actually qualify for changes the conversation completely.

Getting pre-approved takes about two minutes, doesn’t affect your credit score, and gives you a real answer instead of a guess. No sales pressure, no commitment, just clarity on whether traditional financing is on the table for you.

If traditional financing works, you’ll save thousands compared to BHPH. If it doesn’t, at least you’ll know for sure and can make the BHPH decision with eyes open.