")

Car Loans After Repossession: Getting Back on the Road

Carfixcredit | Updated April 2026 | 9 min read

If you’ve been through a repossession, you already know how it changes daily life..

Getting to work suddenly takes twice as long. Grocery runs become an event. The kids need rides everywhere.

And every time you think about applying for a car, you’re sure they’re going to take one look at your credit and laugh you out of the building.

Here’s the part nobody tells you in the middle of all that.

Getting financed again after a repossession is more possible than you think.

Bad credit auto loan options specifically built for buyers in this situation exist, and people use them every day to get back on the road.

This is for anyone who’s lost a car to repossession and is trying to figure out the path back.

It’s not as far as it feels.

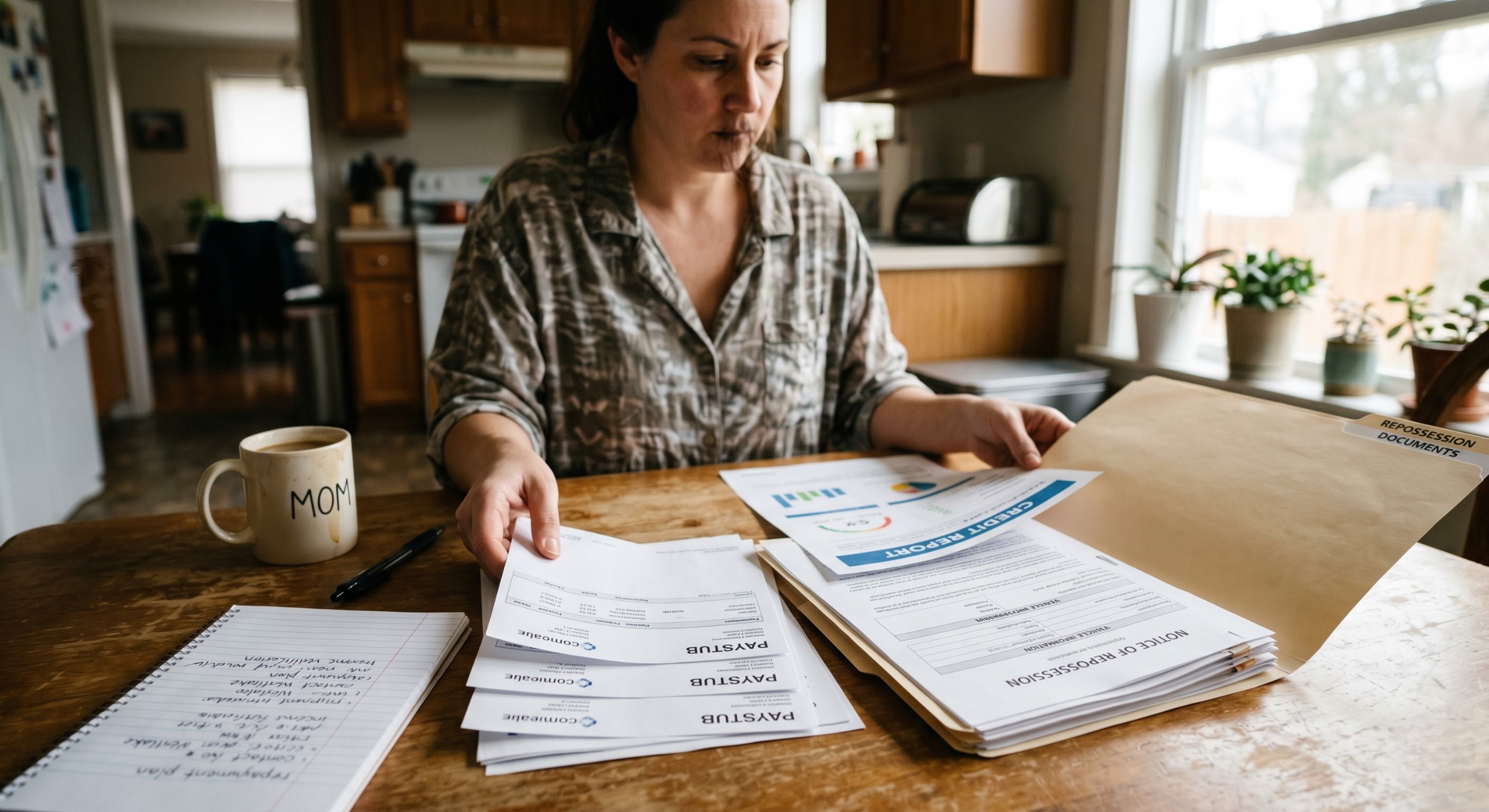

What a repossession actually does to your credit

A repossession hits your credit report hard. There’s no getting around that part. Most people see their score drop somewhere between 100 and 150 points when a repo lands on their report.

The repo stays on your credit for seven years from the date of the original missed payment that triggered it. That sounds like forever, but it isn’t. The damage is heaviest in the first year or two, then gradually starts mattering less as it ages. By year three or four, most lenders weight it much less heavily than they did initially.

There’s also usually a deficiency balance that comes with it. The lender repossessed your car, sold it at auction, and what they got at auction was less than what you owed. The difference is the deficiency, and depending on your state and the lender, they might come after you for it through collections, lawsuits, or wage garnishment.

The deficiency balance creates its own credit damage separate from the repo itself. A collection account, sometimes a charge-off, sometimes a judgment if it goes to court. All of that compounds the original credit hit.

This isn’t to make you feel worse. It’s to help you understand what’s actually on your credit report, because that affects how you approach getting approved for the next loan.

Yes, you can get financed again

The most common myth about repossession is that it disqualifies you from car ownership for years. It doesn’t.

Specialist subprime lenders work with recent repossessions all the time. Some will approve you within months of the repo if your current situation is stable. Others want to see 6 to 12 months pass before they’ll consider it. A small number won’t touch a recent repo at all, but plenty of lenders will.

The factors that determine whether you get approved aren’t really about whether the repo happened. They’re about what’s happened since. Steady employment. Consistent income. Stable address. No new serious credit damage layered on top. Some kind of down payment, even a modest one.

A buyer with a 12-month-old repo who’s been at the same job for two years and has been paying everything on time since the repo is significantly easier to approve than a buyer with no repo but who just lost their job last month. Lenders look at where you are now, not just at the worst point in your past.

Time matters, but maybe not the way you think

A lot of buyers assume they need to wait years after a repo before applying for another loan. That’s usually not necessary, and waiting longer than you have to cost you in other ways.

Here’s roughly how time since the repo affects your options.

Within 6 months of the repo. The lender pool is narrower but real. Specialist programs exist specifically for this window, with stricter down payment requirements and higher rates. Approval is harder but possible if your current situation looks stable.

6 to 12 months out. The pool widens noticeably. Buyers who’ve kept jobs and addresses stable, paid current obligations on time, and started rebuilding even small amounts of credit start looking like reasonable approvals to a broader set of lenders.

12 to 24 months out. The repo still shows on your credit, but most specialist subprime lenders treat applications in this window as standard subprime decisions. The repo matters less than where you are now.

2+ years out with clean credit since. The repo is essentially priced into your credit score at this point. Many lenders treat these applications based on the current credit profile rather than the historical repo.

The point isn’t to rush in immediately after a repo if you’re not ready. The point is that you don’t have to wait three years either. If you have steady income, stable housing, and any kind of down payment, the path is open sooner than most people realize.

The deficiency balance situation

This is the part that trips up a lot of buyers trying to get financed again. The deficiency balance from your original repo can affect the next deal in a few ways.

If the deficiency is sitting in collections, lenders will see it on your credit report. Some specialist subprime lenders are fine with this and approve anyway. Others want to see you’ve made some kind of effort to address it, even a payment plan or partial settlement.

If the deficiency went to a judgment, it’s a more serious issue. A judgment shows you didn’t just have a debt, you had a debt that the creditor took to court and won. Some lenders won’t approve with an active unpaid judgment on file. If this applies to you, finding out the status of the judgment and what it would take to resolve or settle it can make a real difference in approval odds.

If you’ve been making payments on the deficiency, get documentation of that. Lenders see consistent payment history on the deficiency as a positive signal even if the balance is still outstanding. It tells them you’re handling your obligations now, even after a tough stretch.

If the deficiency is paid off entirely, even better. A paid collection still shows on your credit but lenders weight it less heavily than an unpaid one.

What lenders want to see post-repo

Beyond the basic credit picture, lenders evaluating post-repossession applications care about a few specific things.

Income stability matters most. Steady employment in a verifiable job is doing the heaviest lifting in your application. Six months minimum at your current job is the baseline. A year is much better. The lender is essentially asking, “is this person more stable now than they were when the repo happened?”

Verifiable income amount. Most specialist subprime lenders working with post-repo buyers want to see at least $1,800 to $2,000 a month. Self-employed buyers usually need to provide tax returns or bank statements showing consistent income.

Time at residence. Two years at the same address is the strongest signal. Recent moves create more questions, especially if they overlap with the timing of the repo.

A real down payment. Post-repo buyers usually need to put more down than other subprime buyers. 10 to 15 percent is common. Buyers within 6 months of the repo often need closer to 20 percent. The down payment is doing real work to offset the elevated risk.

Recent payment activity. Even a small amount of new positive credit since the repo helps a lot. A secured credit card you’ve been using responsibly, a phone bill that reports to credit bureaus, a small personal loan paid on time. Anything that shows you’re handling current obligations.

A clear story about what happened. You might not have to explain it on the application, but you should be ready to explain it on the call if asked. “I lost my job in 2023, fell behind on the car payment, and they repossessed it. I’ve been at my new job for 18 months and I’ve been doing everything since.” That’s a complete answer that signals stability and self-awareness.

Down payment, the post-repo reality

Most buyers coming out of a repossession aren’t sitting on a lot of cash. The repo itself usually happened because money got tight, and money usually doesn’t get instantly better the next month.

That said, even a modest down payment changes your options significantly. A few ways post-repo buyers put one together.

Tax refund. February through April is the biggest window. If you have a refund coming, it can fund a real down payment without you having to save up over months. A lot of post-repo buyers wait specifically for tax season for this reason.

Saving up over 60 to 90 days. Even $50 a week adds up to $400 to $600 over a couple of months, which is enough to start opening up better lender options. A short wait often saves you significantly more in interest over the loan than the wait itself costs.

A small loan from family. Not always available, not always advisable, but worth mentioning. If a family member can lend you $1,000 toward a down payment, the better terms you get on the loan can sometimes pay that loan back faster than you’d save up the equivalent on your own. Just keep it documented and treat it like a real obligation.

Selling something. Tools, electronics, an extra TV, a side project. Worth a look if you have stuff sitting around that’s worth real money.

The vehicle that fits the situation

The car you can get approved on after a repossession isn’t always the car you initially want. Lenders working post-repo deals are sensitive to loan-to-value because the risk profile is already elevated.

Reliable used vehicles in the $10,000 to $18,000 range, generally under 8 years old, with reasonable mileage tend to fit post-repo financing best. Recent enough that the value is established, common enough that the lender knows what it’s worth, modest enough that the loan stays within your real income capacity.

Trying to finance a $25,000 SUV with a recent repo is going to hit lender resistance. A more modest vehicle gets approved more easily and keeps your monthly payment in a range you can actually sustain. Sustainability is the whole point here, because the worst thing that can happen for someone rebuilding from a repo is to default on the new loan too.

Be willing to have an honest conversation with your finance person about which vehicles work for your specific situation. The right car at $14,000 with an approved loan beats the wrong car at $22,000 with a decline.

Avoiding a second repossession

This is the part that matters most. The first repo damaged your credit. A second one would be much worse, and it would happen on a loan you took specifically to recover from the first one.

A few practical things that help.

Pick a payment you can actually afford, not the maximum you can technically qualify for. The lender will approve you up to a certain payment-to-income ratio, but that doesn’t mean you should max it out. Leave yourself room for the unexpected, because the unexpected is usually what triggers a default.

Set up automatic payments if you can. The most common cause of missed payments isn’t inability to pay, it’s forgetting or losing track. Auto-pay removes that risk entirely.

Have a small emergency fund before you take the loan if at all possible. Even $500 set aside specifically for the car payment if your income hits a snag protects you from a single bad month becoming a default.

Communicate with the lender if something does go wrong. Lenders are much more flexible with buyers who call them proactively than with buyers who go silent and miss payments. A 30-day forbearance because you called and explained a situation is a totally different outcome than a 30-day late mark because you ghosted them.

Know that the first 12 months are the most fragile. Once you’ve made a year of on-time payments, your credit is rebuilding, your situation is stabilizing, and the loan is much more likely to make it to the end successfully. Get through the first year clean and the rest gets easier.

The refinance plan, your way out of high rates

The rate you get on your first post-repo loan will probably feel rough. That’s normal, and it’s not the rate you have to live with for the full term.

Twelve to 18 months of consistent on-time payments rebuilds your credit faster than almost anything else. Once your score has come up and the repo has aged a bit further, you can usually refinance into significantly better terms. A lot of post-repo buyers refinance from 18 to 22 percent down to 10 to 14 percent within 18 months.

That changes how you should think about the original rate. The first loan after a repo is the price of admission to the rebuild. The second loan, or the refinance, is where you start saving real money.

Mark your calendar for 12 months in. Pull your credit, see where you’re at, and start shopping. If your credit has come up enough to qualify for better terms, refinance. If it hasn’t, give it another six months and check again.

The bottom line

A repossession isn’t the end of car ownership. It’s a setback, and a real one, but it’s not a permanent disqualification.

The path back runs through stable employment, a real down payment, a vehicle that fits your situation, and a lender that specifically works with post-repo buyers. Twelve to 18 months of on-time payments on the new loan rebuilds your credit, and a refinance somewhere between months 12 and 18 typically cuts the rate significantly.

The buyers who handle this well usually find that two or three years post-repo, they’re in a better financial position than they were before the original repo happened. The recovery is real. It just takes a plan and the patience to work it.

How Carfixcredit can help you find out where you stand

Most buyers coming off a repossession spend months wondering whether anyone will approve them, when the answer for most of them is yes, and faster than they expected.

Carfixcredit works with a network of lenders across the United States who handle real-world credit situations every day. Recent repossessions, past bankruptcies, deficiency balances, medical debt, none of these are automatic disqualifiers. The options available to buyers in these situations are usually broader than people assume going in, and the only way to know what you actually qualify for is to check.

Getting pre-approved takes about two minutes, doesn’t affect your credit score, and gives you a real answer instead of a maybe. No sales calls, no commitment, just clarity on what’s actually available to you.

If you’ve been putting off applying because you assumed nobody would approve you, that’s the next step. Find out for sure instead of guessing.