")

Secured vs. Unsecured Car Loans: Which Is Right for You?

TL;DR — Quick Summary

- A secured car loan uses the vehicle as collateral, which lowers your APR but lets the lender repossess the car if you miss payments.

- An unsecured car loan is a personal loan with no collateral — APRs are typically 4–8 percentage points higher and approval depends almost entirely on your credit profile.

- Most US auto financing — including every loan CarFix Credit arranges — is secured, because collateral is what makes approval possible for bad credit, no credit, and post-bankruptcy borrowers.

- Unsecured personal loans rarely make sense for buyers with credit below 680, since the higher rate erases any benefit of avoiding a lien on the title.

- CarFix Credit offers secured auto loans from $5,000 to $75,000 across all 50 states, with terms from 12 to 96 months and approval decisions in minutes.

The average APR on a new auto loan hit 7.18% in Q4 2024 according to Experian — but borrowers using unsecured personal loans for the same purchase often paid 12% to 24%. That gap is the single biggest reason the type of car loan you choose matters as much as the lender you choose. Secured and unsecured loans both put you behind the wheel, but they price risk very differently, treat your credit very differently, and end very differently if life throws a curveball.

This guide breaks down how each loan type works, what they cost in real dollars, and which one fits your situation — whether you have excellent credit, you’re rebuilding after bankruptcy, or you’re financing your first vehicle in the United States.

CARFIX CREDIT

Not Sure Which Loan Type You’d Actually Qualify For?

CarFix Credit matches you with secured auto loan offers based on your real numbers — not generic estimates. It only takes a few minutes, and there’s no credit check required to start.

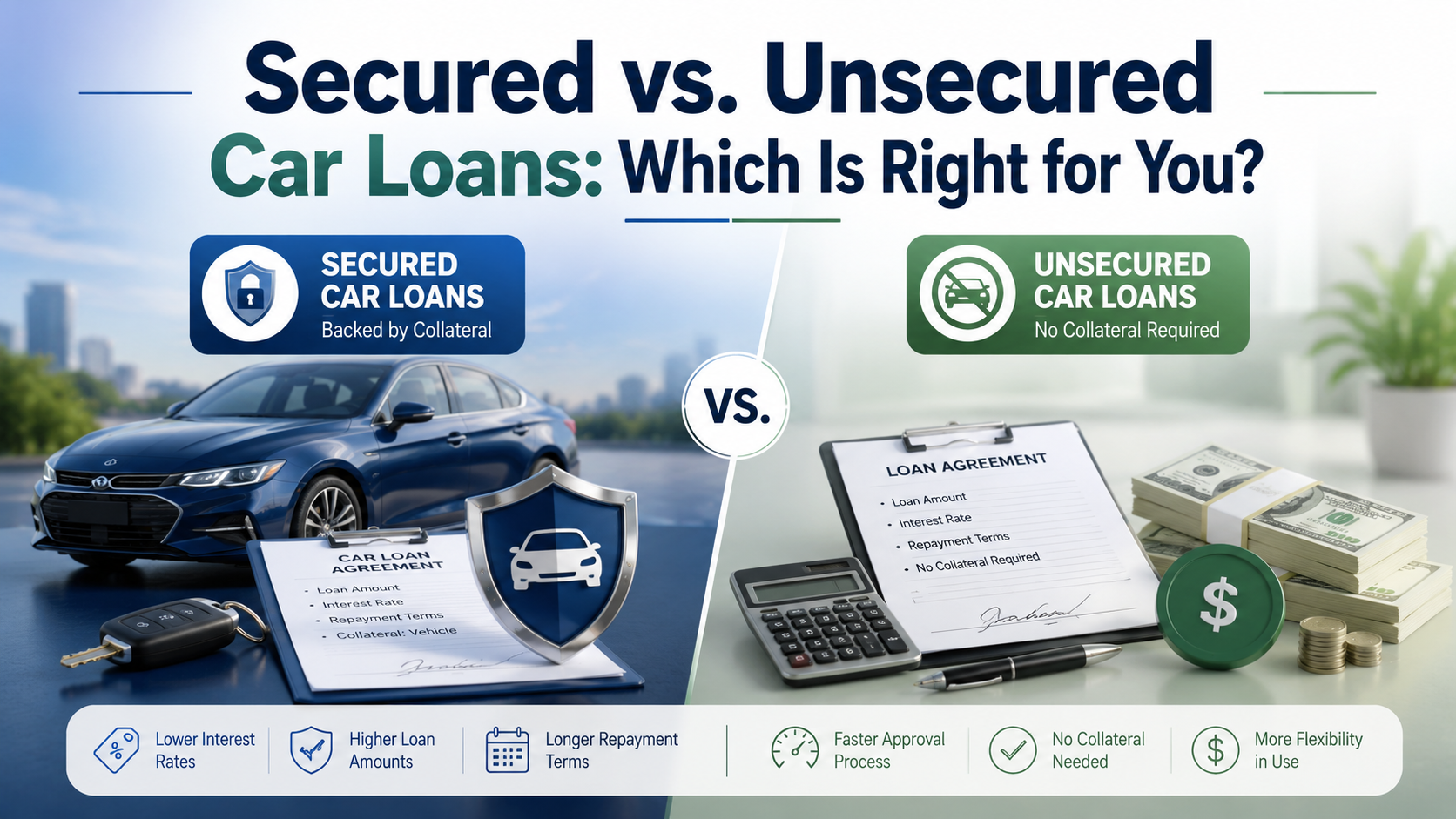

What Is a Secured Car Loan?

A secured car loan is an auto loan where the vehicle itself serves as collateral — the lender places a lien on the title until the loan is paid in full. This is the standard structure for nearly every auto loan issued in the United States, from major banks to credit unions to specialty subprime lenders.

Because the lender holds a claim on the vehicle, their downside risk is capped. If you stop paying, they can repossess and resell the car to recover what’s owed. That security translates into real benefits for you: lower APRs, longer terms, larger loan amounts, and — critically — approval odds that don’t hinge entirely on your credit score. Understanding how auto loans work at this level helps explain why secured financing dominates the market.

Secured auto loans typically range from $5,000 to $75,000, with terms from 12 to 96 months. They’re available through dealerships, banks, credit unions, online lenders, and platforms like CarFix Credit that specialize in connecting borrowers with multiple lenders at once.

What Is an Unsecured Car Loan?

An unsecured car loan is really a personal loan used to buy a vehicle — there’s no lien on the title and no collateral backing the debt. You receive the loan amount as cash, then use those funds to pay the dealer or private seller directly. The car belongs to you outright from day one.

Without collateral, the lender’s only protection is your promise to pay — backed by your credit history, income, and debt-to-income ratio. That makes unsecured loans riskier for the lender, which they price in through higher APRs and stricter credit requirements. Most unsecured personal loans in the US require a credit score of 660 or higher to qualify, and the best rates go to borrowers above 720.

“The average personal loan APR in the United States ranged from 11.92% to 20.05% in 2024, compared to an average new auto loan APR of 7.18% — a difference that costs borrowers thousands of dollars over the life of the loan.” — Federal Reserve consumer credit data, Experian State of the Automotive Finance Market

Unsecured loans also tend to come with shorter terms — usually 24 to 60 months — and smaller maximum amounts, often capped at $40,000 to $50,000 even for highly qualified borrowers. Looking at how your credit score affects your loan options is essential before choosing this path.

Secured vs. Unsecured Car Loans: The Key Differences

Secured car loans beat unsecured options on rate, term length, and loan amount — but unsecured loans give you a debt-free title from day one. The differences come down to seven factors that matter most to American car buyers.

- Collateral: Secured loans use the vehicle as collateral with a lien on the title. Unsecured loans have no collateral at all.

- Typical APR (2024–2025): Secured runs 5% to 20% depending on credit. Unsecured runs 10% to 24% or higher.

- Loan amounts: Secured stretches from $5,000 up to $75,000 or more. Unsecured is usually capped at $40,000 to $50,000.

- Term length: Secured terms run 12 to 96 months. Unsecured terms are typically limited to 24 to 60 months.

- Minimum credit score: Secured loans have no firm minimum because subprime lenders specialize in lower scores. Unsecured loans typically require 660 or higher.

- Risk if you default: Secured defaults trigger repossession and credit damage. Unsecured defaults trigger lawsuits, potential wage garnishment, and the same level of credit damage.

- Title status: The lender holds a lien on a secured loan title until payoff. With unsecured, you own the title outright from day one.

The dollar impact of that APR gap is bigger than most buyers expect. On a $25,000 vehicle financed over 60 months, a 7% secured loan costs $4,702 in total interest. The same purchase at 15% unsecured costs $10,679 — nearly $6,000 more for the same car.

When a Secured Car Loan Makes Sense

A secured car loan makes sense for the vast majority of US car buyers — and it’s effectively the only realistic option for anyone with credit below 660. Subprime auto lending is built specifically around the collateral model, which is why borrowers with scores in the 500s and post-bankruptcy applicants can still get approved.

Choose a secured car loan when:

- Your credit score is below 680, you have a thin credit file, or you’re rebuilding after bankruptcy

- You want the lowest APR available for your credit tier

- You need a loan amount above $40,000 or a term longer than 60 months

- You’re using the loan to rebuild credit — secured auto loans report installment payments to all three bureaus, which strengthens your credit mix

- You’re financing through a dealer that offers manufacturer incentives or promotional APRs

- You’re buying a powersports vehicle — motorcycles, ATVs, Sea-Doos, and side-by-sides are nearly always financed with secured loans

CarFix Credit specializes in secured auto loans for buyers across the entire credit spectrum, including those who’ve been turned down elsewhere. You can estimate your monthly payment before applying to see exactly what fits your budget.

CARFIX CREDIT

Over 183,000 Americans Have Been Approved Through CarFix Credit.

Secured auto loans from $5,000 to $75,000, with terms from 12 to 96 months, across all 50 US states. All credit types welcome — including bad credit, no credit, and post-bankruptcy borrowers — with approval decisions in minutes.

When an Unsecured Loan Might Be Worth Considering

An unsecured personal loan for a car only makes financial sense in a narrow set of situations — usually when the vehicle is too old, too cheap, or too unusual for traditional auto financing to cover. For most buyers, the higher APR makes unsecured loans the more expensive choice even when they’re available.

An unsecured loan may be worth a look when:

- You’re buying a vehicle under $5,000, below most secured auto loan minimums

- The car is too old (typically 10+ years) or has too many miles for a traditional lender to finance

- You’re buying from a private seller in a state where lien processing is slow or complicated

- You have excellent credit (720+) and qualify for a promotional unsecured rate below 8%

- You want to avoid having a lien on the title for resale flexibility

⚠️ Unsecured Loan Trap: Skipping collateral does not skip consequences. If you default on an unsecured personal loan, the lender can sue, secure a judgment, and pursue wage garnishment in most US states — and your credit takes the same 100+ point hit a repossession would cause. The vehicle just stays in your driveway while the debt follows you.

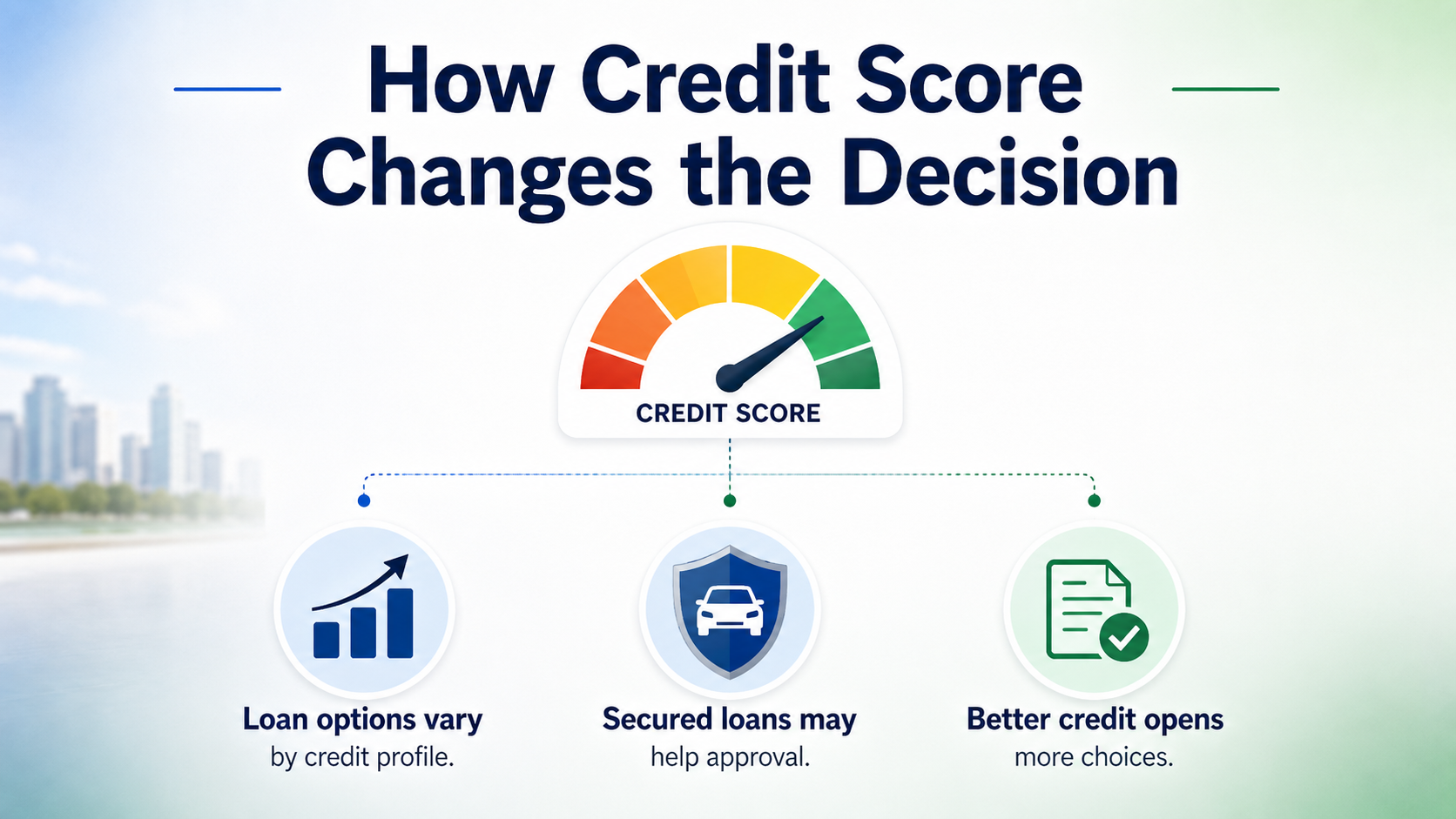

How Credit Score Changes the Decision

Your credit score doesn’t just affect your APR — it often determines which loan type is even available to you. Lenders sort applicants into tiers (prime, near-prime, subprime, deep subprime), and the type of loan they’ll offer shifts at each threshold.

Here’s how the math works at each FICO tier in the United States:

- Super-prime (781+): Either loan type works. Secured offers the lowest APR; unsecured is viable for small loans under $20,000.

- Prime (661–780): Secured is almost always the better choice — the APR advantage over unsecured is significant at this tier.

- Near-prime (601–660): Secured only. Unsecured loans are rarely approved at workable rates in this range.

- Subprime (501–600): Secured only. Unsecured personal loans are generally unavailable below 600.

- Deep subprime (300–500): Secured only, and specialty lenders are required — this is exactly the tier CarFix Credit’s lender network was built to serve.

The takeaway is direct: if you’re below 660, the collateral on a secured loan is what makes approval possible at all. CarFix Credit works with subprime and deep-subprime lenders across all 50 states, including borrowers in Texas, Florida, California, and every state in between, which is why borrowers turned down by their bank can still get approved through CarFix Credit’s network. For deeper reading, explore more auto financing guides on credit tiers, refinancing, and rate shopping.

How to Decide Between Secured and Unsecured

Pick a secured car loan if your priority is the lowest possible payment, the highest possible approval odds, or both. Pick unsecured only if a secured loan literally isn’t available for your vehicle and you have the credit profile to qualify for a sub-10% personal loan APR.

Run through these five questions before you apply:

- What’s my credit score? Below 660 — go secured. Above 720 — compare both.

- How much am I borrowing? Under $5,000 might force you into unsecured; over $40,000 likely requires secured.

- What’s the vehicle? A 12-year-old car with 180,000 miles often won’t qualify for secured financing.

- What’s the APR difference? If unsecured is more than 3 percentage points higher, secured almost always wins on total cost.

- What’s my downside tolerance? Repossession is faster than a judgment, but a judgment damages credit just as severely.

Whichever direction you lean, get pre-approved first. A pre-approval shows you the actual rate and amount you qualify for, which lets you negotiate at the dealership instead of accepting whatever financing the F&I office offers. How the CarFix Credit process works walks through what to expect from application to approval.

Frequently Asked Questions

Is a car loan a secured or unsecured loan?

A traditional car loan is a secured loan, with the vehicle serving as collateral until the loan is paid off. Some borrowers use unsecured personal loans to buy a car, but those are personal loans being used for an auto purchase — not auto loans in the technical sense. Every loan arranged through CarFix Credit is a secured auto loan.

Can I get an unsecured car loan with bad credit?

Getting an unsecured loan for a car with bad credit is very difficult, since most personal loan lenders require a FICO score of 660 or higher. Borrowers with scores below 660 are almost always better served by a secured auto loan, where collateral allows lenders to approve credit profiles they’d otherwise reject. CarFix Credit specializes in secured loans for bad credit, no credit, and post-bankruptcy buyers.

Do secured car loans have lower interest rates than unsecured loans?

Yes, secured car loans have meaningfully lower interest rates than unsecured loans for the same borrower. The collateral reduces the lender’s risk, which they pass along as a lower APR — typically 4 to 8 percentage points lower than a comparable unsecured personal loan. On a $25,000 vehicle, that gap can mean $5,000 to $8,000 in interest savings over a 60-month term.

What happens if I default on a secured car loan?

If you default on a secured car loan, the lender has the legal right to repossess the vehicle and sell it to recover the outstanding balance. Repossession laws vary by state — some states require notice, others allow self-help repossession — but the credit impact is similar across all 50 states: a repossession typically drops a FICO score by 100 points or more and stays on your credit report for seven years.

Can I refinance an unsecured car loan into a secured one?

Yes, you can refinance an unsecured personal loan that you used for a car into a secured auto loan, as long as the vehicle still meets the new lender’s age and mileage requirements. Refinancing into a secured loan typically drops your APR significantly and can reduce your monthly payment or shorten the term. CarFix Credit’s lender network handles both refinances and new purchases across all 50 states.

Does applying for a car loan hurt my credit?

Starting a pre-approval through CarFix Credit uses a soft credit pull, which does not affect your credit score. A hard inquiry only happens once you accept a specific loan offer and the lender finalizes the approval. Multiple auto loan inquiries within a 14-day window are also counted as a single inquiry by FICO, so rate shopping doesn’t compound the credit impact.

Get Pre-Approved for Your Secured Auto Loan Today

CarFix Credit helps Americans across all 50 states get approved for auto financing — regardless of credit history. Loan amounts from $5,000 to $75,000, terms from 12 to 96 months, and approval decisions in minutes.

- ✅ All credit types welcome — including bad credit and bankruptcy

- ✅ $0 down financing options available

- ✅ No credit check to start the application

- ✅ Approval decisions in minutes, fully online

📍 Address: 3401 N. Miami Ave, Suite 230, Miami, FL 33127

🌐 Website: carfixcredit.com

🇺🇸 Coverage: All 50 US states — fully online application

Bad credit. No credit. Bankruptcy. CarFix Credit helps you get on the road regardless.