")

Soft Credit Check vs Hard Credit Check on Car Loans: What Every Buyer Should Know

TL;DR — Quick Summary

- A soft credit check on a car loan does not affect your credit score and is used for pre-qualification, rate previews, and approval odds — like the one CarFix Credit runs to start your application.

- A hard credit check (or hard inquiry) appears on your credit report, can drop your FICO score by up to 5 points, and stays visible for 24 months — but only impacts scoring for 12 months.

- Multiple hard auto loan inquiries within a 14-day window (45 days on newer FICO models) count as a single inquiry for scoring purposes, so rate-shopping is safe if you keep it tight.

- Lenders use soft pulls to give you an estimate and hard pulls to finalize your loan — both are normal parts of the financing process.

- CarFix Credit lets you check your approval odds with a soft pull only — no credit damage required to see what you qualify for across all 50 US states.

Roughly one in three Americans avoids applying for an auto loan because they fear the inquiry will tank their credit. That fear is mostly outdated. The difference between a soft credit check vs hard credit check on car loans isn’t just technical jargon — it directly controls whether shopping for financing costs you 0 points or 5 points off your FICO score.

Understanding which type of pull happens at each step lets you compare lenders, get pre-approved, and walk into a dealership without a paper trail of damaging inquiries. Below is exactly how each works, when lenders use them, and how to protect your score while still getting the best rate.

CARFIX CREDIT

Curious what you’d qualify for — without the credit hit?

CarFix Credit uses a soft credit check to give you a real loan estimate — your score stays exactly where it is. It only takes a few minutes — no credit check required to start.

What Is a Soft Credit Check on a Car Loan?

A soft credit check (also called a soft inquiry or soft pull) is a review of your credit file that does not affect your FICO or VantageScore. Lenders use soft pulls to estimate what rate, loan amount, and term you’d likely qualify for — before any formal application begins.

Soft pulls are invisible to other lenders. They appear only on the credit report version you pull yourself, listed under “inquiries that don’t affect your credit score.” Common examples include pre-qualification offers, employer background checks, account reviews from your existing credit card issuer, and your own annual credit report check at AnnualCreditReport.com.

In the auto financing world, a soft pull is what powers most online pre-approval tools. When CarFix Credit asks for basic information to show you how the CarFix Credit process works, the underlying credit check is soft — meaning you can check your odds without consequence. This matters most for buyers rebuilding credit, where every point counts.

What Is a Hard Credit Check on a Car Loan?

A hard credit check (hard inquiry or hard pull) is a formal review triggered when you apply for credit. It typically lowers your FICO score by up to 5 points, appears on your credit report for 24 months, and influences your score for the first 12 of those months.

Lenders pull hard inquiries when you’ve committed to moving forward — finalizing an auto loan, mortgage application, or new credit card. For a car loan specifically, the hard pull usually happens at the dealership when you sign the formal financing paperwork, or when an online lender funds the loan after you accept the terms.

“A single hard inquiry typically lowers a FICO score by less than five points, and the impact diminishes over time, disappearing from score calculations after 12 months.” — myFICO, Fair Isaac Corporation

The hard pull serves a real purpose: it pulls your full credit file so the lender can verify income claims, calculate your debt-to-income ratio, and lock in the exact APR. Without one, no auto loan can actually close. Understanding how your credit score affects your loan helps you time hard inquiries strategically — typically only when you’re ready to buy.

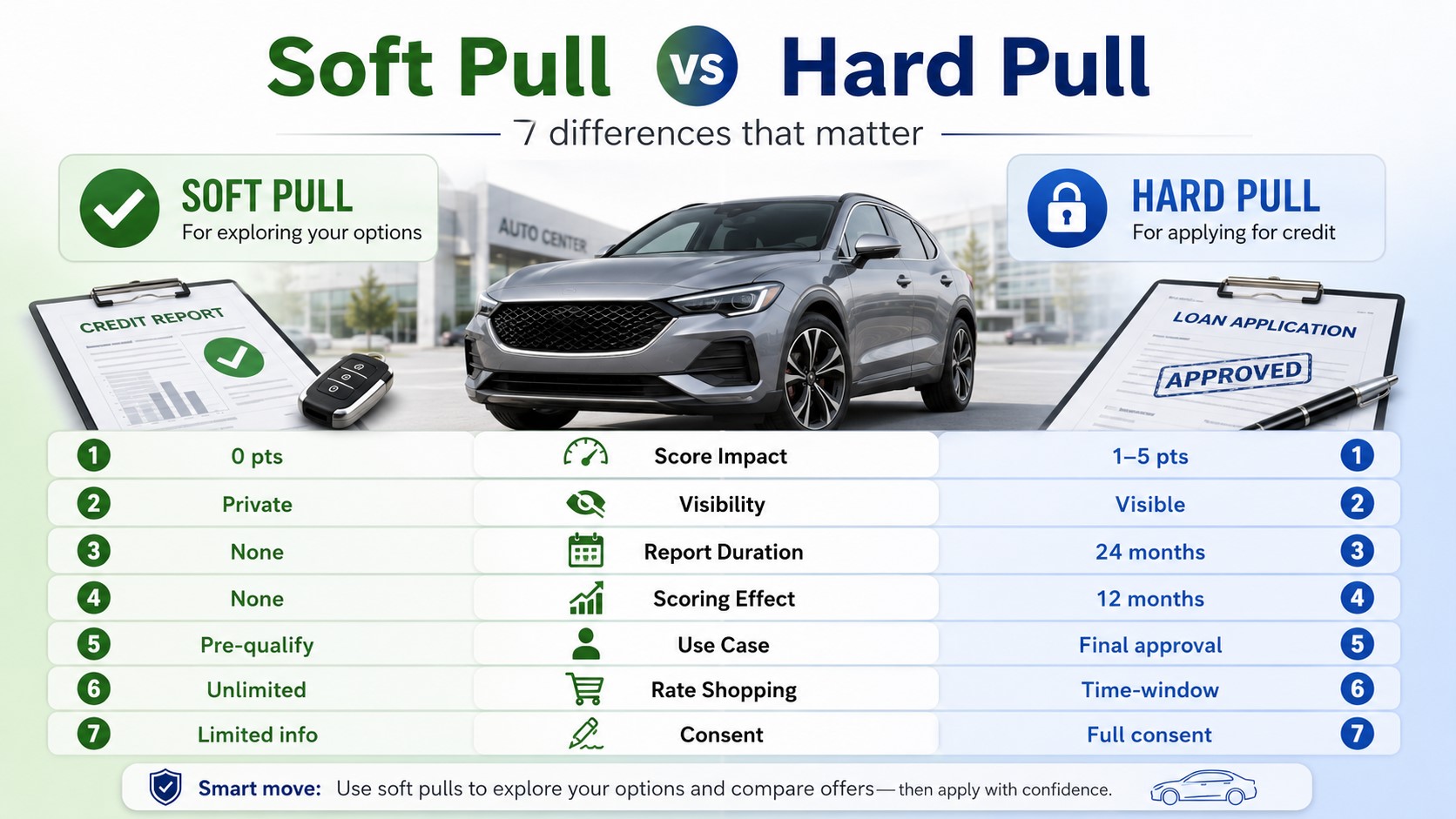

Soft Pull vs Hard Pull: The Seven Differences That Matter

The two credit checks differ across every dimension that matters when financing a vehicle — and the gaps shape when you should shop and when you should sign. Here are the seven practical differences in plain terms.

Score impact. A soft pull costs zero points. A hard pull typically costs 1 to 5 points off your FICO score, with most borrowers landing in the 1 to 3 point range.

Visibility to other lenders. Soft pulls are invisible to anyone reviewing your file later. Hard pulls show up on the credit report that lenders, landlords, and employers see for 24 months from the date of the inquiry.

Scoring window. Soft pulls never affect your score. Hard pulls influence your FICO score for the first 12 months, then stay listed on your report for another 12 months with no scoring impact.

Information required. Most soft pulls only need the last four digits of your Social Security Number plus basic personal information. Hard pulls require your full SSN and explicit written or digital consent under the Fair Credit Reporting Act.

Use case. Lenders use soft pulls for pre-qualification, rate previews, and approval-odds checks before you’ve committed to anything. They use hard pulls for final approval and loan funding — the binding step.

Rate-shopping safety. Soft pulls are always safe to repeat — there’s no cap on how many you can run. Hard pulls are safe to repeat only within a 14-day window under classic FICO, or a 45-day window under FICO 8 and 9, which treats multiple auto loan inquiries as a single event.

Consent format. Soft pulls sometimes happen without your direct authorization — such as pre-screened mailers from credit card issuers. Hard pulls always require your explicit consent, and any hard inquiry on your report you didn’t authorize can be disputed.

The practical takeaway: use soft pulls broadly to compare offers and find your best match, then accept a single hard pull only when you’re confident in the deal. Tools like the loan calculator to estimate your monthly payment let you model the deal before any inquiry occurs.

The 14-Day Rate-Shopping Window Explained

When you apply for an auto loan with multiple lenders, FICO treats all hard inquiries within a 14-day window as a single inquiry for scoring purposes — and newer FICO 8 and 9 models extend that window to 45 days. This is specifically designed so consumers aren’t penalized for comparison shopping.

For example: a borrower in Texas applies at three different banks for the same vehicle on June 1, June 5, and June 10. FICO sees these as one hard inquiry, costing at most a few points. If that same borrower spread the applications across June 1, July 1, and August 1, they’d be counted as three separate inquiries — potentially dropping their score 10–15 points.

⚠️ Dealer Inquiry Trap: When you sit at a dealership “F&I” desk, the finance manager may submit your application to 8–12 lenders simultaneously to find the best rate. Even within the 14-day window this still counts as one inquiry — but the rejections and credit pulls become visible on your file. Always ask the dealer to send your application to a maximum of two or three specific lenders, not blast it out unrestricted.

When Does Each Type of Credit Check Happen?

Most auto loan applications follow the same two-stage credit check pattern: a soft pull at the front end to qualify you, and a hard pull at the back end to fund the loan. Knowing the sequence lets you pause at the right moments.

- Online pre-qualification (soft pull): You enter basic info, get an estimated rate and loan range. No credit impact.

- Pre-approval letter (soft pull): A conditional offer based on stated income, also soft. You can shop with this letter at any dealership.

- Vehicle selection (no pull): Choosing the specific car, truck, SUV, or motorcycle. No inquiry happens here.

- Dealer financing submission (hard pull): The dealer or direct lender pulls your full credit report to verify, lock the APR, and finalize the loan.

- Final loan documents (no additional pull): Signing the retail installment contract uses the report already pulled.

CarFix Credit operates the same way — soft pull to start, hard pull only when you’ve chosen a vehicle and are ready to close. That’s a major reason 183,256+ Americans have used the platform to compare options without burning their score on the first click.

CARFIX CREDIT

183,256+ Americans Approved — Soft Pull First, Always.

CarFix Credit offers auto loans from $5,000 to $75,000 with terms from 12 to 96 months across all 50 US states. Start with a soft credit check, see your real options, and only proceed to a hard pull when you’ve picked your vehicle.

Does Pre-Approval Use a Soft Pull or a Hard Pull?

Most reputable online auto lenders — including CarFix Credit — use a soft pull for pre-approval. Some traditional banks and credit unions, however, run a hard inquiry for pre-approval even when you haven’t selected a vehicle, so the distinction matters when comparing providers.

Before applying, look for explicit language like “checking will not affect your credit score,” “soft credit check only,” or “no credit check to start.” Vague phrasing like “free pre-approval” can mean either — always ask before submitting. The Consumer Financial Protection Bureau requires lenders to disclose which type of inquiry will be made, but the disclosure is sometimes buried in fine print.

If you’re unsure where your credit currently sits before any inquiry, it’s worth understanding how auto loans work and what credit tier you fall into. Borrowers in the deep subprime range (below 580) particularly benefit from soft pull pre-approval, since they often need to apply to multiple specialty lenders to find an approval.

How to Protect Your Credit Score While Shopping for a Car Loan

Smart auto loan shopping is structured: use soft pulls broadly, hard pulls narrowly, and keep the timeline compressed. Buyers who follow this pattern often save thousands in interest while losing fewer than 5 points in the process.

- Start with two or three soft-pull pre-approvals — get baseline rate estimates without any score impact.

- Decide on your vehicle and budget before authorizing any hard inquiry.

- Compress all hard pulls into a 14-day window so FICO treats them as one inquiry.

- Avoid opening other credit lines — credit cards, store financing — within 60 days of an auto loan application.

- Check your own credit report at AnnualCreditReport.com (soft pull, free) before applying so you know exactly what lenders will see.

For buyers with thin or damaged credit, this structure is especially important — a single avoidable hard inquiry can mean the difference between qualifying for prime rates around 7% APR (the average new car loan APR per Experian’s Q4 2024 State of the Automotive Finance Market) and subprime rates north of 14%. The same applies whether you’re financing a sedan in Ohio, a truck in Arizona, or motorcycle loan options in Florida — every inquiry counts.

Frequently Asked Questions

Does a soft credit check show up on my credit report?

A soft credit check appears on the version of your credit report that you pull yourself, but it does not show up on the report that lenders, landlords, or employers see. It also does not affect your FICO or VantageScore in any way, no matter how many soft pulls occur.

How many points does a hard credit check cost on a car loan?

A single hard credit check on a car loan typically lowers your FICO score by 1 to 5 points, with most borrowers seeing less than a 3-point drop. The impact is temporary — hard inquiries stop influencing your score after 12 months and disappear from your report entirely after 24 months.

Can I get pre-approved for a car loan without a hard credit check?

Yes, you can get pre-approved for a car loan without a hard credit check by using lenders that run soft pulls for pre-qualification. CarFix Credit, for example, uses a soft credit check to give you a real loan estimate across all 50 US states before any hard inquiry occurs.

How long do hard inquiries stay on my credit report?

Hard inquiries remain visible on your credit report for 24 months from the date of the pull, but they only affect your FICO score for the first 12 months. After the first year, the inquiry is still listed but has zero scoring impact.

Will multiple car loan applications hurt my credit score?

Multiple car loan applications submitted within 14 days count as a single inquiry under classic FICO scoring — and within 45 days under FICO 8 and 9 models. As long as you compress your auto loan shopping into that window, you can apply with several lenders and only incur one score hit.

What’s the difference between pre-qualification and pre-approval?

Pre-qualification is a soft-pull estimate based on self-reported information — quick, non-binding, and credit-safe. Pre-approval is a more thorough review based on verified income and credit data; some lenders use a soft pull for this, others a hard pull, so always check before submitting.

Check Your Auto Loan Options Without Touching Your Credit Score

CarFix Credit helps Americans across all 50 states get approved for auto financing — regardless of credit history. Loan amounts from $5,000 to $75,000, terms from 12 to 96 months, and approval decisions in minutes.

- ✅ All credit types welcome — including bad credit and bankruptcy

- ✅ $0 down financing options available

- ✅ No credit check to start the application

- ✅ Approval decisions in minutes, fully online

📍 Address: 3401 N. Miami Ave, Suite 230, Miami, FL 33127

🌐 Website: carfixcredit.com

🇺🇸 Coverage: All 50 US states — fully online application

Bad credit. No credit. Bankruptcy. CarFix Credit helps you get on the road regardless.