")

Using Your Trade-In as a Down Payment: How It Works

TL;DR — Quick Summary

- Your trade-in’s equity — what it’s worth minus what you still owe — is what actually becomes your down payment.

- According to Edmunds, the average US trade-in value in 2024 was around $21,500, making trade-ins one of the largest down-payment sources for American car buyers.

- Negative equity (owing more than the car is worth) can be rolled into your new loan, but it raises your monthly payment and total interest.

- Trade-in value varies by source — Kelley Blue Book, Edmunds, and dealer offers can differ by $1,500 to $3,000 on the same vehicle.

- CarFix Credit accepts trade-ins toward your down payment on loans from $5,000 to $75,000, across all 50 US states and all credit types.

A trade-in is one of the most powerful tools an American car buyer has when they don’t have thousands of dollars sitting in savings. Using your trade-in as a down payment lets you turn the vehicle you already own into instant cash equity toward your next car — without writing a check or draining your bank account. For buyers with limited credit or tight budgets, it can be the difference between getting approved and being stuck.

But the process is not automatic. Your trade-in’s value depends on its condition, mileage, payoff balance, and where you take it. Dealers may offer less than private-party value, and if you still owe money on the car, the math changes quickly. This guide breaks down exactly how trade-ins work as down payments, what affects your value, and how to make sure you don’t leave money on the table.

CARFIX CREDIT

Curious How Much Your Trade-In Is Really Worth?

Get pre-approved through CarFix Credit and we’ll factor your trade-in equity directly into your auto loan terms. It only takes a few minutes — no credit check required to start.

How a Trade-In Becomes a Down Payment

A trade-in becomes a down payment when the dealer or lender applies your vehicle’s equity directly to the price of your new car. Equity is the difference between what your current vehicle is worth and what you still owe on it. If your car is worth $14,000 and you owe $9,000, you have $5,000 of equity — that $5,000 becomes your down payment.

If your car is paid off, the math is simpler: the full appraised value goes toward your next purchase. This is where trade-ins shine for buyers without savings. Instead of saving $3,000 to $5,000 in cash, your old vehicle does the work. Understanding how auto loans handle trade-ins helps you walk into a deal knowing exactly what your vehicle should reduce from the total financed amount.

The transaction usually happens in three steps. First, the dealer or lender appraises your vehicle. Second, they pay off any remaining loan balance directly to your current lienholder. Third, any leftover equity is credited as your down payment on the new loan. CarFix Credit follows the same process and accepts trade-ins on financing across all 50 US states.

How Trade-In Value Is Calculated

Trade-in value is calculated using your vehicle’s make, model, year, mileage, condition, trim level, options, and current market demand. Dealers and lenders typically pull values from Kelley Blue Book, Black Book, or Manheim auction data, then adjust based on a physical inspection. Different sources can produce different numbers for the same car.

The five biggest factors affecting your trade-in value:

- Mileage — A vehicle with 60,000 miles can be worth $2,000–$4,000 more than the same model with 120,000 miles.

- Condition — Cosmetic damage, mechanical issues, and a worn interior can shave 10–30% off the value.

- Market demand — Trucks and SUVs typically hold value better than sedans, especially in regions like Texas and the Midwest.

- Service history — Documented maintenance records can boost an appraisal by hundreds of dollars.

- Title status — A clean title is worth more than a salvage, rebuilt, or branded title.

“The average US trade-in value reached $21,544 in 2024, with three-year-old vehicles retaining about 60% of their original MSRP — significantly higher than the historical average.” — Edmunds Trade-In Value Report

Before stepping into any dealership, run your vehicle through at least two valuation tools — Kelley Blue Book and Edmunds are the most cited — and write down both the trade-in value and the private-party value. That gap is your negotiation room. You can also estimate your monthly payment at different down-payment levels to see how your trade-in changes the deal.

Positive Equity vs. Negative Equity

Positive equity means your vehicle is worth more than you owe, giving you cash toward your next car. Negative equity — also called being “upside-down” or “underwater” — means you owe more than the car is worth, which adds to the cost of your next loan instead of reducing it.

A real example: Say your truck appraises at $18,000 and you owe $22,000. You have $4,000 of negative equity. If you trade it in toward a $30,000 vehicle, the dealer rolls that $4,000 into your new loan — you’re now financing $34,000 instead of $30,000. According to the Consumer Financial Protection Bureau (CFPB), roughly 1 in 4 American auto trade-ins in recent years has carried negative equity, with the average shortfall sitting near $6,500.

⚠️ Negative Equity Risk: Rolling negative equity into a new loan can stretch your term to 84 or even 96 months and put you upside-down on the new vehicle from day one. If you’re trading in a car you still owe more than $3,000 over its value, consider waiting, refinancing, or putting cash down to offset the gap before signing.

If you’re upside-down, you still have options. Improving your credit score before applying can reduce your APR enough to offset some of the added negative equity. A larger cash down payment, a co-signer, or selecting a less expensive vehicle can also keep the new loan from becoming unmanageable.

How Trade-Ins Affect Loan Approval

A trade-in directly improves your chances of loan approval because it lowers the loan-to-value (LTV) ratio — the percentage of the vehicle’s price you’re financing. Lenders use LTV to gauge risk, and a lower ratio means lower risk and better approval odds, especially for buyers with bad credit, no credit, or past bankruptcies.

A practical example: a borrower with a 580 credit score applying for a $25,000 vehicle with no down payment may be quoted 18% APR — if approved at all. The same borrower with a $4,000 trade-in equity contribution drops the financed amount to $21,000, which can push approval into a lower risk tier and unlock APRs closer to 14–15%. Over a 72-month term, that difference can save more than $4,000 in total interest.

CARFIX CREDIT

Over 183,000 Americans Have Been Approved Through CarFix Credit.

Whether you have a paid-off trade-in or one with a balance, CarFix Credit factors your equity directly into your loan terms. Approvals in minutes for loan amounts from $5,000 to $75,000, across all 50 states, for every credit type.

Steps to Use Your Trade-In as a Down Payment

Using your trade-in as a down payment is straightforward when you follow a clear sequence. Doing the research first puts you in a stronger negotiating position and prevents dealer lowballing.

- Check your loan payoff amount. Call your current lender and request a 10-day payoff quote. This is the exact amount needed to clear the title.

- Get at least two value estimates. Use Kelley Blue Book and Edmunds to pull both the trade-in value and the private-party value of your vehicle.

- Clean and prep your vehicle. A detailed car can add $200–$500 to your appraisal. Fix small issues — a burned-out bulb or missing floor mat — before the appraisal.

- Gather your documents. Bring the title (if you have it), registration, current insurance, recent loan statement, and any service records.

- Get pre-approved before the dealership. Walking in with a pre-approval lets you separate the trade-in negotiation from the financing negotiation — two deals, not one.

- Negotiate the trade-in separately. Ask, “What would you give me for my car as a straight purchase?” before mentioning the new vehicle.

- Confirm equity is applied as down payment. Review the buyer’s order or contract and verify the trade-in credit line matches the agreed appraisal minus your payoff.

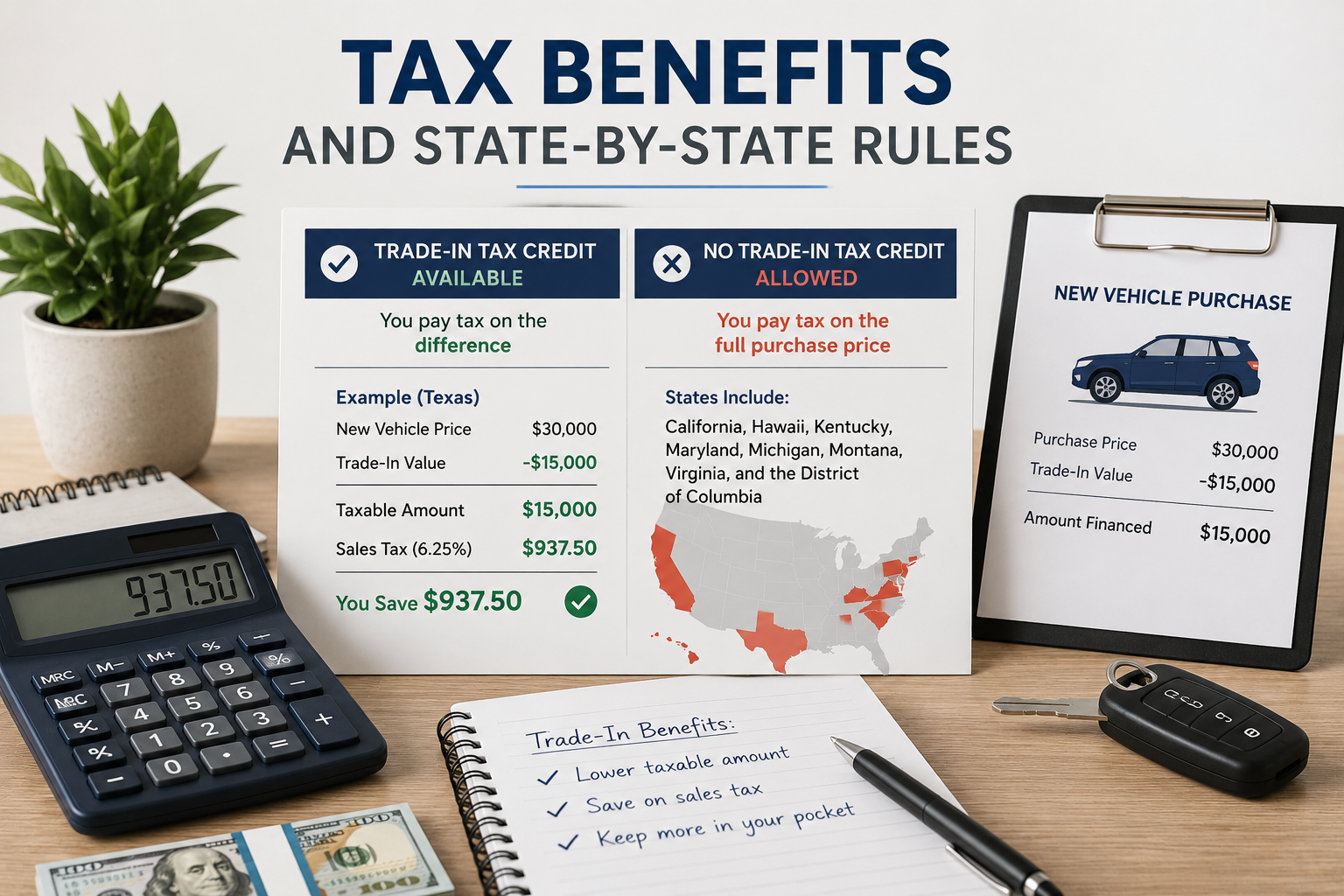

Tax Benefits and State-by-State Rules

In most US states, trading in a vehicle reduces the sales tax you owe on your new purchase — because you only pay tax on the difference between the new vehicle’s price and your trade-in value. This can save hundreds, sometimes thousands of dollars depending on where you live.

For example, in Texas with a 6.25% state sales tax, trading in a $15,000 vehicle toward a $30,000 purchase means you pay tax on $15,000 — not $30,000 — saving roughly $937. California, Hawaii, Kentucky, Maryland, Michigan, Montana, Virginia, and the District of Columbia do not allow this trade-in tax credit, so buyers there pay tax on the full purchase price. Check your state’s department of revenue site to confirm rules before signing.

This tax benefit is part of why selling privately doesn’t always net more money than trading in. If your private-party sale would bring $2,000 more but you’d lose $1,500 in tax savings, the trade-in may come out ahead — especially when you factor in the time, advertising, and risk of selling privately. Seeing how the CarFix Credit process works can help you weigh the trade-in math before committing.

Common Mistakes That Cost You Money

The most expensive trade-in mistake is letting the dealer combine the trade-in, the new car price, and the financing into one figure. When everything moves at once, it’s nearly impossible to verify each piece. Always negotiate the trade-in value, the new vehicle price, and the loan terms as three separate conversations.

Other common mistakes include skipping the cleanup before the appraisal, accepting the first offer without a second opinion, hiding mechanical issues that the inspector finds anyway, and not knowing your loan payoff balance going in. Reading more auto financing guides before negotiating can help you spot dealer tactics and protect your equity.

Frequently Asked Questions

Can I use a trade-in as my entire down payment?

Yes, your trade-in can serve as your entire down payment if its equity covers what the lender requires. For buyers with bad credit, lenders typically expect a down payment of 10–20% of the vehicle price, and a paid-off trade-in worth that amount can cover it completely. CarFix Credit accepts trade-ins as full or partial down payments on loans from $5,000 to $75,000.

What if I still owe money on my trade-in?

If you still owe money on your trade-in, the dealer or lender pays off your existing loan and applies any remaining equity as your down payment. If you owe more than the vehicle is worth, the negative equity gets rolled into your new loan, increasing the total amount you finance. Always request a 10-day payoff quote from your lender before negotiating.

How much does a trade-in lower my monthly payment?

A trade-in lowers your monthly payment by reducing the amount you need to finance. For every $1,000 of trade-in equity applied as a down payment, your monthly payment on a 60-month loan drops roughly $18–$22 depending on your APR. A $4,000 trade-in equity can reduce a typical monthly payment by $75–$90.

Is a trade-in better than selling my car privately?

A trade-in is better when you want speed, simplicity, and sales tax savings — most US states reduce taxes on the difference between your new vehicle and your trade-in. Private sales typically bring $1,500–$3,000 more in raw cash but require time, advertising, test drives, and risk. For credit-challenged buyers, the trade-in path is also tied directly to loan approval.

Does my credit score affect my trade-in value?

No, your credit score does not affect what your trade-in is worth — value is based purely on the vehicle’s make, model, year, mileage, and condition. However, your credit score does affect the APR you’ll pay on the new loan, which determines how far your trade-in equity stretches. A higher score means lower interest and more value from every dollar of equity.

Can I trade in a vehicle with mechanical problems?

Yes, you can trade in a vehicle with mechanical problems, but it will be appraised at a lower value to account for repair costs. Be upfront about known issues — appraisers will find them during inspection, and undisclosed problems can damage trust during negotiation. CarFix Credit works with trade-ins of all conditions when arranging financing across the United States.

Turn Your Trade-In Into a Pre-Approval Today

CarFix Credit helps Americans across all 50 states get approved for auto financing — regardless of credit history. Loan amounts from $5,000 to $75,000, terms from 12 to 96 months, and approval decisions in minutes.

- ✅ All credit types welcome — including bad credit and bankruptcy

- ✅ $0 down financing options available

- ✅ No credit check to start the application

- ✅ Approval decisions in minutes, fully online

📍 Address: 3401 N. Miami Ave, Suite 230, Miami, FL 33127

🌐 Website: carfixcredit.com

🇺🇸 Coverage: All 50 US states — fully online application

Bad credit. No credit. Bankruptcy. CarFix Credit helps you get on the road regardless.