")

How Long Should Your Car Loan Term Be? (12 to 96 Months)

Carfixcredit | Updated April 2026 | 7 min read

The loan term is one of the most consequential decisions in auto financing and most buyers barely think about it.

They see a monthly payment that fits their budget and say yes. The term that produced that payment is almost an afterthought.

That’s understandable.

Monthly payments feel real and immediate. Loan terms feel abstract. But the term you choose affects how much the vehicle actually costs you, how long you’re financially tied to it, and whether you end up in a good or bad position if something changes along the way.

This guide walks through every common loan term from 12 months to 96 months, what each one looks like in practice, and how to figure out which one actually makes sense for your situation.

What a Loan Term Actually Is

The loan term is simply the length of time you have to repay the loan. It’s measured in months.

A 48-month term means four years of monthly payments.

A 72-month term means six years.

A 96-month term means eight years of paying for a vehicle that starts losing value the moment you drive it off the lot.

The term affects two things directly. Your monthly payment and your total interest paid.

Longer term equals lower monthly payment but more total interest. Shorter term equals higher monthly payment but less total interest. That tradeoff is the core of every loan term decision.

The Full Range of Loan Terms

12 to 24 Months

These are the shortest terms available and almost nobody uses them for a standard vehicle purchase.

The monthly payment on a short term is high. A $25,000 loan at 6.5 percent over 24 months works out to roughly $1,120 per month. That’s a significant monthly commitment and most buyers simply can’t absorb it.

Where short terms make sense is on a small loan amount, a vehicle being partially paid off with a large down payment, or a buyer who wants to eliminate the debt as fast as possible and has the income to support the payment.

The total interest saved on a 24-month term versus a 60-month term on the same loan can be substantial. If the payment is manageable for your budget, the financial case for a short term is strong.

36 Months

Three years. Still on the shorter end but starting to produce monthly payments that work for a broader range of buyers.

On a $20,000 loan at 6.5 percent, a 36-month term produces a monthly payment of around $612 and total interest of approximately $2,030.

Buyers who choose 36-month terms typically have a reasonably large down payment reducing the loan amount, a strong income relative to the payment, or a preference for owning the vehicle free and clear quickly.

The interest savings compared to longer terms are meaningful and you build equity in the vehicle fast. The downside is purely the monthly commitment.

48 Months

Four years. This is where a lot of buyers with good credit land when they’re being financially disciplined about their vehicle purchase.

On a $20,000 loan at 6.5 percent, a 48-month term produces a payment of around $476 and total interest of approximately $2,840.

The monthly payment is meaningfully lower than a 36-month term but the total interest increase is relatively modest. The 48-month term represents a reasonable balance between affordability and cost efficiency for buyers who can make it work.

60 Months

Five years. The most common loan term in the market and the one most buyers end up with when they finance a vehicle.

On a $20,000 loan at 6.5 percent, a 60-month term produces a payment of around $391 and total interest of approximately $3,460.

The payment is accessible for most income levels, the term is long enough to keep things manageable without extending too far into the future, and five years is a reasonable horizon for a vehicle purchase.

The risk with 60 months is the same as any term long enough for significant depreciation to occur before you’ve paid enough of the principal to keep up. On a new vehicle with a small down payment, you can be underwater for a meaningful portion of the first two years.

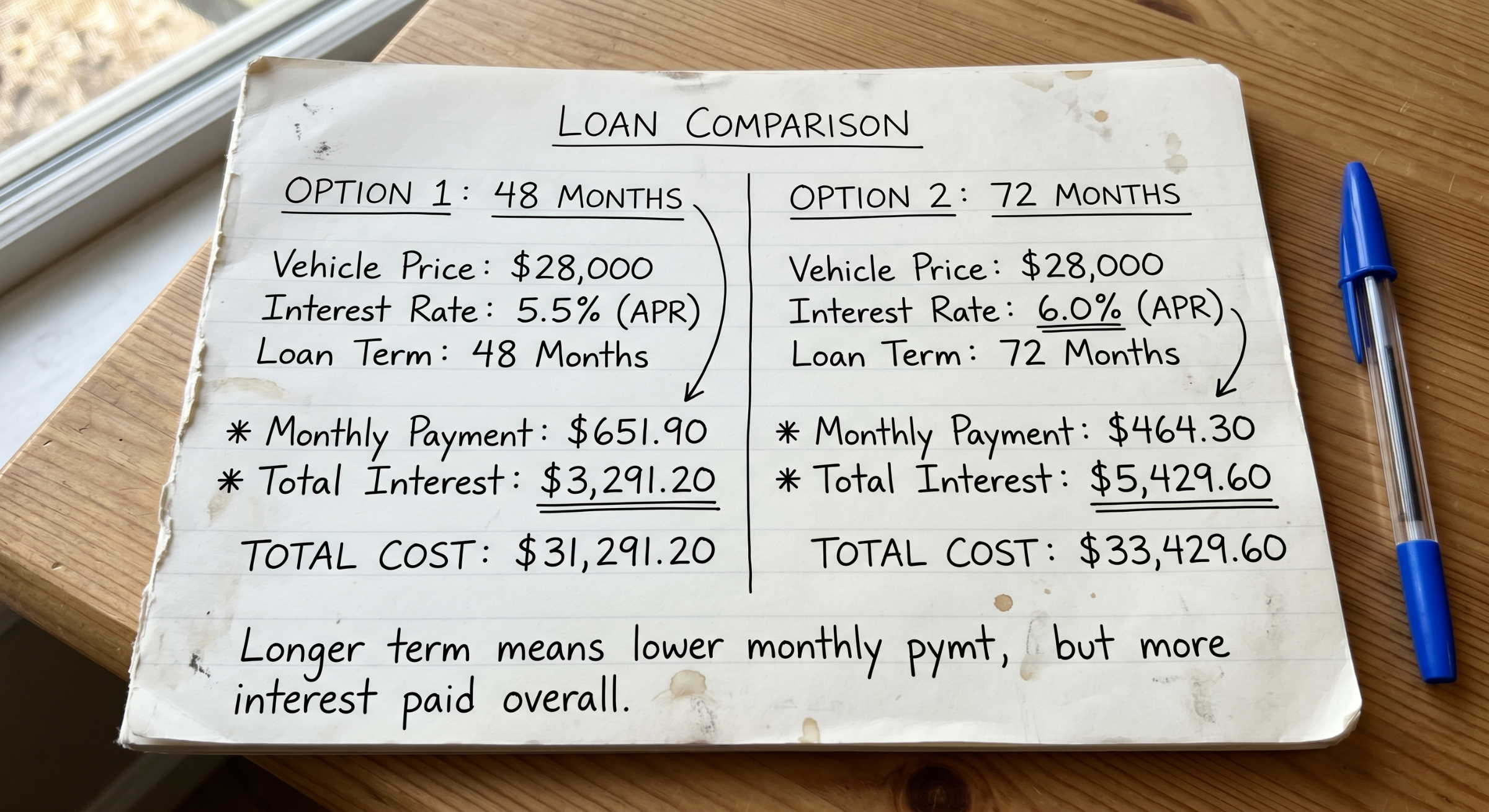

72 Months

Six years. This is where the tradeoffs start becoming more significant and worth examining carefully before you commit.

On a $20,000 loan at 6.5 percent, a 72-month term produces a payment of around $337 but total interest climbs to approximately $4,280.

The monthly payment looks more comfortable than a 60-month term. But you’re paying $820 more in total interest for that lower payment. And six years is a long time to be tied to a vehicle that may need significant maintenance or repairs in the later years of the loan.

The negative equity window is also longer at 72 months. On a new vehicle depreciating at normal rates, you could be underwater for the first three or four years of a six-year loan with a modest down payment.

Buyers who choose 72 months often do so because the monthly payment makes an otherwise unaffordable vehicle fit their budget. That’s worth being honest with yourself about. If the 60-month payment is too much, the vehicle might be too expensive for your current financial situation.

84 Months

Seven years. This is the term that makes financial advisors wince and it’s become increasingly common.

On a $20,000 loan at a subprime rate of 14 percent, which is realistic for many buyers choosing this term, the monthly payment is around $379 but total interest paid over seven years is approximately $11,840.

That’s nearly $12,000 in interest on a $20,000 vehicle. By the time the loan is paid off, the car is seven years old and the total cost of the loan has almost doubled the original price in interest alone.

Buyers are drawn to 84-month terms because the monthly payment looks similar to a shorter term at a lower rate. The difference is invisible in the moment and very visible over time.

There are specific situations where an 84-month term is the only workable option. A buyer with challenged credit who needs a vehicle and has limited lender options may not have a choice. In those cases, having a clear plan to refinance once the credit improves is essential.

For buyers who do have other options, choosing 84 months to get a lower monthly payment on a vehicle you could have financed on a shorter term is a decision worth reconsidering.

96 Months

Eight years. The longest term now offered by some lenders and a decision that almost never makes financial sense for a standard vehicle purchase.

The math at 96 months is genuinely concerning for most buyers. You’re paying off a vehicle for eight years. The vehicle will likely need significant repairs before the loan is done. You’ll be deeply underwater for most of the loan’s life. And the total interest paid makes the actual cost of the vehicle dramatically higher than the sticker price.

The only scenario where a 96-month term makes any practical sense is a very expensive vehicle with a very low rate, where the low payment and long horizon serve a specific financial strategy. For most buyers financing a standard vehicle, this term should be approached with extreme caution.

Understanding how loan term length affects your total auto loan cost before you agree to any term is one of the most important things you can do as a buyer.

The Negative Equity Problem

This is the risk that connects loan term length to a real financial consequence worth understanding before you choose.

Negative equity means you owe more on the loan than the vehicle is currently worth. It’s also called being underwater or upside down on the loan.

It happens because vehicles depreciate faster than most loan terms pay down the principal balance. In the early months of a long-term loan, most of each payment goes toward interest. The principal balance drops slowly. Meanwhile, the vehicle’s market value is dropping steadily.

The longer the term, the deeper and longer the negative equity window.

On a 60-month loan with a reasonable down payment, you might be underwater for the first year or two. On an 84-month loan with no down payment, you could be underwater for four or five years.

If you need to sell the vehicle, trade it in, or if it gets totaled during that window, you’re responsible for the difference between what you owe and what the vehicle is worth. Gap insurance covers the totaled car scenario. Nothing except paying down the loan faster covers the trade-in or sale scenario.

This is why down payment and loan term are connected decisions. A larger down payment shortens the negative equity window regardless of the term you choose.

How to Choose the Right Term for Your Situation

There’s no single answer that works for everyone. Here’s a framework that helps.

Start with what you can actually afford monthly. Not what fits if everything goes perfectly. What’s manageable if something goes wrong in the next few years. A car payment that requires everything to go right for 72 months is a fragile plan.

Work backward from that number to find the shortest term that stays within your budget. That’s your starting point.

If the shortest affordable term still produces a loan that will leave you underwater for a long time, reconsider the vehicle price before you reconsider the term. A less expensive vehicle on a shorter term is almost always a better financial position than an expensive vehicle on a long one.

Factor in the rate. Comparing auto loan terms and rates simultaneously gives you a complete picture of what each option actually costs rather than just what it costs monthly.

Consider how long you plan to keep the vehicle. If you’re the type to trade in every three or four years, a 72-month term creates a very predictable problem. You’ll likely owe more than the vehicle is worth when you try to trade it, and that negative equity gets rolled into the next loan. If you plan to drive the vehicle until it’s paid off, a longer term is less problematic though still more expensive in total interest.

Loan Term and Bad Credit

Buyers with challenged credit often face a specific challenge with loan terms.

The rate offered on a subprime loan is high enough that the monthly payment on a short term becomes unmanageable. Longer terms are sometimes the only way to make the payment work.

If that’s your situation, here’s the honest advice.

Take the longest term you need to make the payment genuinely manageable. Not the longest term that gets you into an expensive vehicle. The longest term that makes a reasonable vehicle affordable.

Set a reminder to check your refinancing options at 12 to 18 months. If your credit has improved through consistent on-time payments, refinancing into a shorter term at a better rate can save meaningful money over the remaining life of the loan.

The long term is a bridge, not a destination. Treat it that way and it works. Settle into it without a plan to improve and it costs you more than it needed to.

A Simple Comparison Across Common Terms

Using a $22,000 loan at 7 percent to illustrate.

A 36-month term produces a monthly payment of roughly $679 and total interest of approximately $2,440.

A 48-month term produces a monthly payment of around $527 and total interest of approximately $3,280.

A 60-month term produces a monthly payment of about $436 and total interest of approximately $4,140.

A 72-month term produces a monthly payment of around $376 and total interest of approximately $5,060.

A 84-month term produces a monthly payment of roughly $333 and total interest of approximately $5,980.

The monthly payment difference between 60 and 84 months is $103.

The total interest difference is nearly $1,840. Paying $103 less per month for 84 months costs you $1,840 more in total interest.

That’s the math worth sitting with before you choose the longer term for the lower payment.

The Bottom Line

The right loan term is the shortest one you can genuinely afford.

Not the shortest one that makes the payment tight every month. Not the longest one that gets you into a vehicle you’d otherwise have to pass on. The shortest term that fits your actual budget with room to breathe.

Everything beyond that is paying interest for the convenience of a lower monthly number. Sometimes that convenience is worth it. Often it isn’t. The difference is knowing the real cost before you agree to it.

How Carfixcredit Helps You Find the Right Term

Whether you’re working with strong credit or a more challenging situation, Carfixcredit connects buyers across the United States with lenders who offer flexible term options across all credit profiles.

Checking what you qualify for takes about two minutes and won’t affect your credit score. You’ll know your rate and term options before you walk into any dealership.