")

Does Getting Pre-Approved for a Car Loan Hurt Your Credit?

Carfixcredit | Updated April 2026 | 8 min read

This is one of the most common questions people ask before applying for a car loan, and one of the most misunderstood.

Most people have heard somewhere that checking on a loan can hurt your credit, so they hesitate. They wait. They keep driving a car that’s barely running because they’re scared a five-minute application is going to drop their score.

Here’s the short version. Auto loan pre-approval usually doesn’t hurt your credit at all, and even when it does, the impact is small and temporary. The fear is way bigger than the actual risk.

This is for anyone who’s been putting off checking their options because they don’t want to mess with their credit.

Let’s clear it up!

The two kinds of credit checks, and why the difference matters

When a lender or company looks at your credit, they’re doing one of two things. A soft inquiry or a hard inquiry. They sound similar but they affect your credit completely differently.

A soft inquiry is when someone checks your credit without you formally applying for new credit. This includes when you check your own credit, when an existing creditor reviews your account, when a company pre-screens you for an offer, or when most pre-approval tools run a quick check. Soft inquiries don’t show up on your credit report in any way that affects your score. You can have hundreds of them and your score doesn’t move.

A hard inquiry happens when you formally apply for credit and the lender pulls your full credit report to make a decision. Auto loans, credit cards, mortgages, personal loans. Hard inquiries do show up on your credit report and can drop your score, usually by 5 to 10 points temporarily.

The pre-approval question hinges entirely on which kind of inquiry the pre-approval uses. Most legitimate pre-approval tools, including the one at Carfixcredit, use a soft inquiry to give you an initial answer. That means checking what you qualify for has zero impact on your credit score.

The hard inquiry only happens if you actually proceed with a formal application after seeing your pre-approval. And even then, the impact is small.

What “pre-approval” actually means

People use the word pre-approval to mean a few different things, which adds to the confusion. Let’s get clear on what it actually is.

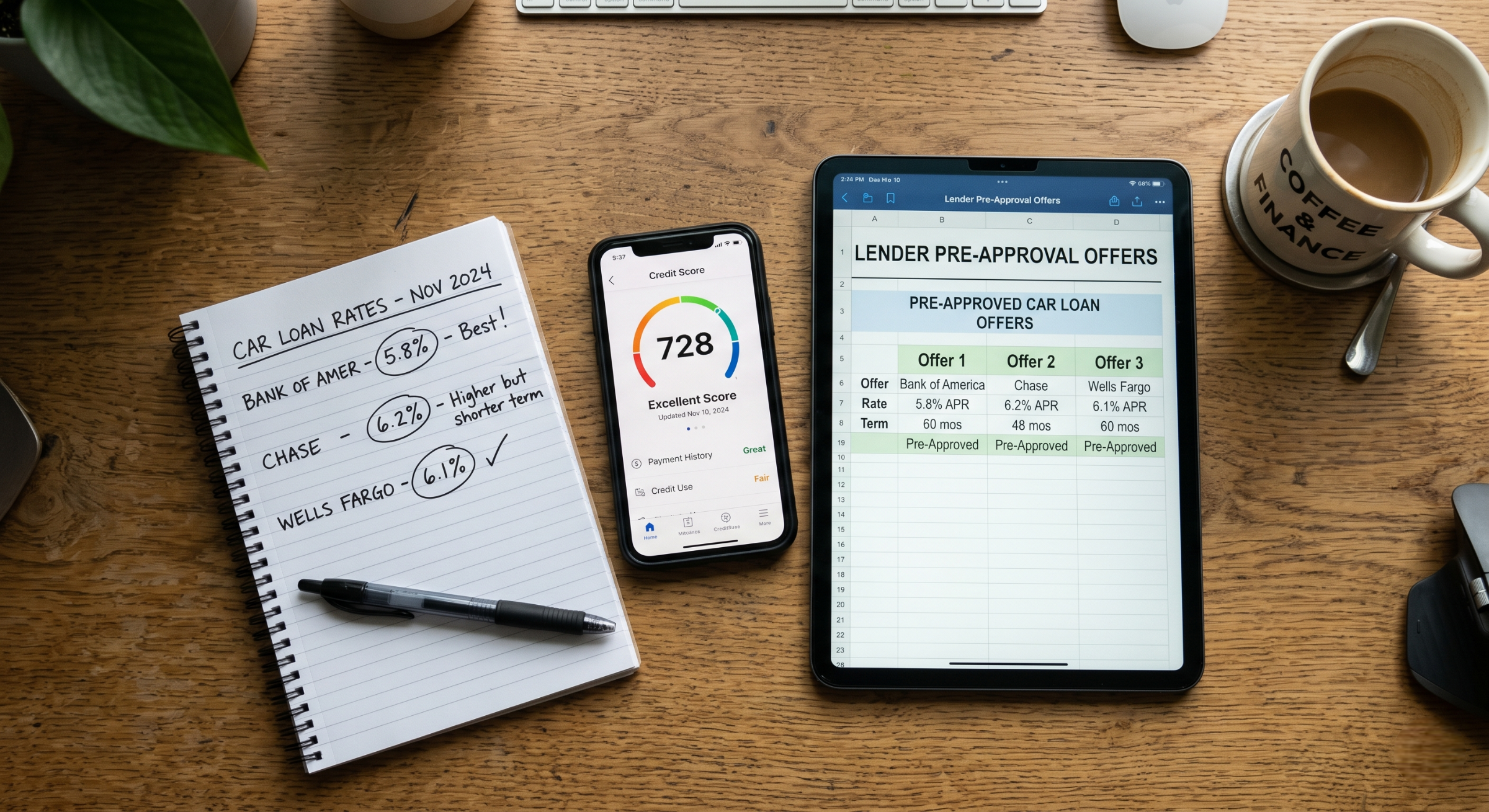

A pre-approval is the lender telling you, based on a quick review of your information, what you’d likely qualify for if you submitted a full application. It’s not a guarantee. It’s a strong indicator. The lender has looked at your basic information, run a soft credit check, and said something like, “based on what we’re seeing, you’d likely qualify for a loan up to $X at around Y percent.”

That’s useful information. It tells you whether buying a car is realistic for you right now, what kind of monthly payment you’d be looking at, and roughly what rate you should expect when you actually go to a dealership.

Pre-approval is different from pre-qualification, which is even lighter. Pre-qualification often doesn’t involve any credit check at all and is just based on what you self-report. Pre-qualification is faster but less reliable.

Pre-approval is also different from a final approval. Final approval happens when you’ve picked out a specific car, submitted a full application, the lender has done their full underwriting, and the deal is locked in. That’s when the hard inquiry happens, if it hasn’t already.

Most online auto loan pre-approval tools work like this. You fill out a short form with your information. The system runs a soft credit check. You get an answer in a couple of minutes about what you’d likely qualify for. No hard inquiry. No impact on your score. You take that information with you when you start shopping.

The actual impact of a hard inquiry, when one does happen

Eventually, if you decide to actually apply for an auto loan, a hard inquiry will happen somewhere in the process. So it’s worth understanding what that actually does to your credit.

A single hard inquiry typically drops your score by 5 to 10 points. The impact varies depending on what’s already on your credit report. People with thin credit files see slightly bigger impacts. People with established credit see smaller ones.

The impact is temporary. Most of the score drop fades within a few months as the inquiry ages on your report. The inquiry itself stays on your report for about two years, but its effect on your score essentially disappears within 12 months.

Compared to other credit factors, a single inquiry is small. Late payments, collections, high credit card balances, all of those affect your score significantly more than an inquiry does. People worry about inquiries way more than they should and worry about payment history way less than they should.

If you’re applying for a car loan and the inquiry drops your score 8 points, but the loan you take out and pay on time for a year raises your score 50 points, the math is overwhelmingly in your favor. The inquiry is the cost of getting access to a tool that improves your credit substantially.

The 14-day rule that most people don’t know about

Here’s a piece of how credit scoring actually works that most car buyers have never heard of. It changes the whole conversation about shopping for rates.

When you’re shopping for an auto loan and you submit applications to multiple lenders within a short window, the credit bureaus treat all those inquiries as a single inquiry for scoring purposes. The window varies depending on which scoring model is used, but it’s usually 14 days. Some models extend it to 45 days.

This means you can apply at five different lenders within two weeks and your score impact is essentially the same as if you’d only applied at one. The credit bureaus understand that auto loan shopping involves comparing rates, and they don’t want to penalize people for being smart about it.

So the worry that “every application I submit is going to crush my score” isn’t accurate. As long as you’re shopping within a reasonable window, the cumulative impact is similar to a single application.

This applies to auto loans, mortgages, and student loans specifically. It doesn’t apply to credit card applications, where each one is treated as a separate inquiry.

Why pre-approval is actually good for your credit, indirectly

There’s a counterintuitive piece of this most people miss. Getting pre-approved before you walk into a dealership often protects your credit better than walking in without one.

Here’s why. When you don’t have a pre-approval and you sit down at a dealer’s finance desk, they typically submit your application to multiple lenders to find one that will approve you. Each of those submissions is a hard inquiry. If they submit to seven lenders, that’s seven inquiries.

In theory, the 14-day rule we just talked about should bundle those into a single inquiry for scoring purposes. In practice, dealer submissions sometimes get spread out over more than 14 days, especially if the deal takes time to structure or if the dealer keeps trying new lenders. That can result in inquiries that count separately and add up.

When you walk in with a pre-approval already in hand, you usually don’t need the dealer to shop your application across multiple lenders. You already have a financing offer. The dealer might still submit one or two additional applications to see if they can beat your pre-approved rate, but the volume of inquiries is typically lower.

Pre-approval also gives you leverage in the negotiation, which is its own benefit. But the credit protection piece is real and underrated.

The pre-approval process from the buyer’s side

If you’ve never been through it, here’s what an auto loan pre-approval actually looks like in practice.

You fill out a short form online. Most reputable services ask for the basics. Your name, address, date of birth, social security number, employment information, income, and what kind of vehicle you’re thinking about. The form usually takes about two to three minutes to complete.

The system runs a soft credit check. This happens in the background, doesn’t affect your score, and pulls your credit report so the lender can see what they’d be working with.

You get an answer, usually within a couple of minutes. The answer tells you whether you’re likely to be approved, roughly what loan amount you’d qualify for, and roughly what rate to expect. Some pre-approvals also tell you what monthly payment range you’d be looking at.

If the pre-approval is positive, you can take that information shopping. You know what you can afford, what rate you should expect, and you have a much stronger position when you walk into a dealership.

If the pre-approval shows you don’t qualify for what you wanted, that’s also useful information. It might tell you that you need to wait, save up a larger down payment, look at less expensive vehicles, or work on your credit before applying. Better to find that out from a soft inquiry than to find out after a series of hard inquiries.

The myths that keep people from checking

A few persistent myths keep people from getting pre-approved when they should. Worth clearing them up directly.

“Any check on my credit will drop my score.” Not true. Soft inquiries don’t affect your score at all. Hard inquiries do, but only by a few points and temporarily.

“If I get denied for pre-approval, that hurts my credit.” Not really. The soft inquiry from the pre-approval check itself doesn’t affect your score. Even if the pre-approval comes back as a no, your score doesn’t move. The “denial” doesn’t get reported to the bureaus as a separate event.

“Multiple pre-approvals will tank my credit.” Not true if they’re soft inquiries, which most are. Even if they were hard inquiries, the 14-day rule would bundle them together for scoring purposes.

“Pre-approvals are a scam to collect my information.” A legitimate pre-approval service uses your information to actually run a real credit check and give you a real answer. The information is used for the purpose you submitted it for. Reputable services explain clearly how your information is used and don’t sell it to unrelated third parties.

“Once I get pre-approved, I have to use that lender.” Not true. A pre-approval is information, not an obligation. You can get pre-approved through one source and end up financing through another if you find better terms elsewhere. The pre-approval is yours to use however you want.

What to actually do

Here’s the practical playbook if you’re trying to figure out whether to get pre-approved.

If you’re considering buying a car within the next few months, get pre-approved. The information is valuable, the soft inquiry doesn’t affect your credit, and walking into a dealership informed is significantly better than walking in blind.

Use a reputable service that uses soft inquiries for the initial pre-approval. Carfixcredit is one option, but there are others. The right service will tell you upfront whether they use a soft or hard inquiry and how your information will be used.

If you want to compare rates across multiple lenders, do it within a 14-day window when possible. This bundles any hard inquiries that happen into a single scoring impact rather than multiple separate ones.

Don’t let the fear of a tiny temporary score drop keep you from getting information that could save you thousands. Even in the worst case scenario where every step involved a hard inquiry, the total score impact would be small, temporary, and dwarfed by the benefits of making an informed financing decision.

The bigger picture on credit and car loans

Step back for a second. The whole reason people worry about credit checks is because they’re worried about their credit score. But the biggest factor in your credit score isn’t inquiries. It’s how you handle the credit you already have.

Paying your bills on time, keeping credit card balances low, not applying for too much new credit at once, those things move your score. A few inquiries from auto loan shopping are noise compared to the signal of your overall credit behavior.

If your credit is good and you take out an auto loan and pay it on time, your score will keep growing. The inquiry from the application is irrelevant within a year.

If your credit is rough and you take out a subprime auto loan and pay it on time, your score will rebuild meaningfully. The inquiry from the application is more than offset by the positive payment history that follows.

The car loan is doing real work on your credit either way. The inquiry is a tiny cost of entry to a tool that helps you long-term. Don’t let small fears about small impacts keep you from making good financial decisions.

The bottom line

Getting pre-approved for a car loan, in almost every case, doesn’t hurt your credit. The pre-approval check is usually a soft inquiry that doesn’t affect your score at all. Even when a hard inquiry eventually happens later in the process, the impact is small and temporary, and the 14-day rule protects you when shopping rates across multiple lenders.

The information from a pre-approval is genuinely useful. It tells you what you qualify for, what to expect, and gives you leverage when you walk into a dealership. The cost is essentially nothing. The benefit is real.

If you’ve been putting off applying because you were worried about your credit, you can stop worrying about that part. Whatever’s holding back your decision, the pre-approval check itself isn’t it.

How Carfixcredit makes the pre-approval process easy

A lot of buyers waste months wondering whether they qualify for an auto loan, when checking takes a couple of minutes and doesn’t affect their credit at all.

Carfixcredit works with a network of lenders across the United States who handle real-world credit situations every day. The pre-approval check uses a soft inquiry, which means your credit score doesn’t move when you check what’s available to you. Bad credit, no credit, past bankruptcies, recent repossessions, none of these are automatic disqualifiers.

Getting pre-approved takes about two minutes. No sales pressure, no commitment, no impact on your credit score. You get a real answer about what you qualify for, what rate to expect, and what monthly payment range you’d be looking at.

If you’ve been waiting to apply because of credit concerns, this is the lowest-risk way to find out where you actually stand. The information is valuable. The check is free.