")

Subprime Auto Loans: How They Work and What to Watch Out For

Carfixcredit | Updated April 2026 | 9 min read

If your credit isn’t where you’d want it to be and you’ve been told you’d need a “subprime” loan to get a car, you’ve probably got a few questions about what that actually means.

Maybe you’ve heard horror stories.

Maybe you’ve been told the rates are crazy and you should just wait.

Maybe you don’t really know what subprime is and just want a straight explanation without someone trying to sell you something.

Here’s a real one..

Subprime auto loans are how millions of Americans buy cars every year.

They’re not a scam. They’re not predatory by default. They’re just car loans for people whose credit needs work.

There are good versions and bad versions, and knowing the difference is what protects you.

This is for anyone who needs to know what they’re getting into before they sit down at a finance desk.

What subprime actually means

Subprime is just a label lenders use to describe borrowers whose credit is below what they consider “prime.”

The exact cutoffs vary, but most lenders use something like this. Prime credit usually means a score above 660 or 670. Subprime means below that, with the deeper end of subprime sitting under 580.

That’s the whole concept. It’s not a judgment about you as a person. It’s just a way for lenders to categorize risk so they can price their loans accordingly. A subprime loan is a loan made to someone in that credit range, with terms adjusted to match the higher risk the lender is taking on.

The credit score that puts you in subprime can come from a lot of places. A bankruptcy. A repossession. Medical debt that wrecked your score. A divorce that left joint accounts unpaid. A few late payments years ago that haven’t fully aged off yet. Or just no credit history because you’ve never borrowed anything before.

None of those situations make you a bad borrower. They just put you in a different lending category for a while.

How a subprime loan is different from a regular one

The structure of a subprime loan is mostly the same as any auto loan. You borrow a set amount, agree to pay it back over a fixed term with interest, and the car serves as collateral. Standard stuff.

What’s different is the rate, the lender pool, and sometimes the requirements around down payment and vehicle.

The rate is higher. That’s the main thing. Where a prime borrower might get 6% or 7% on a used car, a subprime borrower is more likely to see something between 12% and 22% depending on where exactly their credit falls. The reason isn’t punishment. It’s that lenders price loans based on default risk, and historically, subprime loans default at higher rates than prime loans. The rate covers that risk.

The lender pool is different. Most traditional banks and credit unions don’t lend much in the subprime space. Specialist lenders do. These are companies whose entire business is lending to credit-challenged buyers, and they know how to underwrite the risk in ways that traditional lenders aren’t set up for.

Down payment requirements tend to be higher. A prime borrower can sometimes get away with zero down. A subprime borrower usually needs to put at least 10 to 15 percent down, sometimes more depending on the lender and where their credit sits.

Vehicle requirements can be stricter too. Some subprime lenders won’t finance cars over a certain age or mileage, because the value of older high-mileage vehicles drops too fast for them to feel comfortable with the loan-to-value ratio.

Why the rates are what they are

Nobody loves paying 18% interest on a car loan. So it’s worth understanding why that rate exists, instead of just feeling like you’re being charged extra for being broke.

Subprime borrowers default more often than prime borrowers. That’s the unavoidable math the lenders are working with. Out of every 100 subprime loans a lender writes, more of them will end in repossession or charge-off than out of 100 prime loans. The interest rate has to cover those losses, plus the cost of the loan, plus a profit, or the lender goes out of business.

The higher the default rate in a given credit tier, the higher the rate the lender charges. That’s why someone with a 540 score sees higher rates than someone with a 620 score, even though both are technically subprime. The lender is pricing the loan based on the actual risk profile of buyers in that score range.

There’s also a regulatory cost baked in. Subprime lending is more heavily regulated than prime lending in most states. Compliance, audits, and the legal infrastructure cost money, and that cost shows up in the rate too.

It’s not personal. It’s just the math of how the segment works. Knowing this doesn’t make the rate cheaper, but it might make it feel less arbitrary.

The good versions of subprime

Most subprime lenders are running honest businesses. Their loans cost more than prime, but the structure is straightforward, the disclosures are clear, and the buyer comes out the other end with a car and rebuilt credit.

A good subprime loan looks like this. The rate matches your credit profile. The term is reasonable, usually between 60 and 72 months for a used car. The down payment is set at a level that protects both you and the lender. The vehicle fits within the lender’s standard parameters. The contract is straightforward and the disclosures match what you were told verbally.

You’ll know you’re working with a legitimate subprime lender when the conversation feels like a real evaluation of your situation. They want to see your income. They want to verify employment. They check your credit. They explain the rate, the term, and the total cost in ways you can follow.

That’s how it should work. The fact that the loan costs more than a prime loan doesn’t mean it’s a bad deal. It’s just a more expensive version of the same product, priced for the credit tier.

The bad versions, what to watch out for

Subprime is also a space where some real predatory practices exist. Knowing what they look like is what protects you.

Yo-yo financing. This is when a dealer tells you you’re approved, lets you drive the car home, and then calls a week later saying the financing fell through and you need to bring in more money down or accept worse terms. The dealer is using the fact that you’ve already started thinking of the car as yours to pressure you into worse terms. The way to avoid this is simple. Don’t drive a car off the lot until the financing is fully and finally approved, signed, and locked in. If the dealer is pushing you to take the car before that’s done, slow down.

Padded loans. Some dealers add extras into the loan that you didn’t ask for. Extended warranties, gap insurance, paint protection, wheel coverage, theft tracking. Some of these have real value, some don’t. The problem is when they get rolled into the financing without a clear conversation about what each one costs and whether you actually want it. Read the itemized list. Ask about every line item. Push back on anything you don’t want.

Rates way above what your credit deserves. Even within subprime, rates have a normal range. If you’re being quoted 28% or higher on a deal that other lenders would do at 18%, something’s off. Get a second opinion before signing. Specialist subprime lenders compete with each other, and there’s almost always more than one option for a buyer with your credit profile.

Loan terms that don’t fit the car. A 96-month loan on an older used car is a setup for being underwater for years. The car will lose value faster than you pay the loan down, and if anything goes wrong, you’re stuck owing more than the car is worth. Long terms make the monthly payment look smaller, but they cost you a lot in interest and in flexibility. Be cautious of any term over 72 months on a used car.

No documentation required. A real lender wants to see your income, your employment, your address, your bank activity. If a dealer is offering financing without any of that, they’re either setting you up for a yo-yo deal where the real terms come later, or they’re an extreme buy-here-pay-here operation that’s going to charge you well above standard subprime rates.

Buy here pay here vs traditional subprime

These are two different things and worth not confusing.

A traditional subprime loan is a loan from a specialist subprime lender, usually a finance company or a bank that specializes in this space. The dealer sells you the car. The lender provides the financing. The lender holds the loan and you make payments to them.

Buy here pay here is when the dealer is also the lender. They sell you the car and finance it themselves. You make payments directly to the dealer. These dealers usually serve buyers with the absolute lowest credit scores, often below 500, and the rates are typically the highest in the industry. The cars are often older, the down payment requirements can be high, and some of these dealers install GPS trackers or starter interrupt devices on the cars to make collection easier.

Buy here pay here isn’t automatically bad. For some buyers, it’s the only option that exists, and it can be a path to a vehicle and a way to rebuild credit through consistent payments. But the terms are usually worse than what a real subprime lender would offer, and if you can qualify for a traditional subprime loan, you’re almost always better off taking it.

How to get the best deal you can in subprime

The rate you get in subprime isn’t entirely fixed. There are real things you can do to improve your terms.

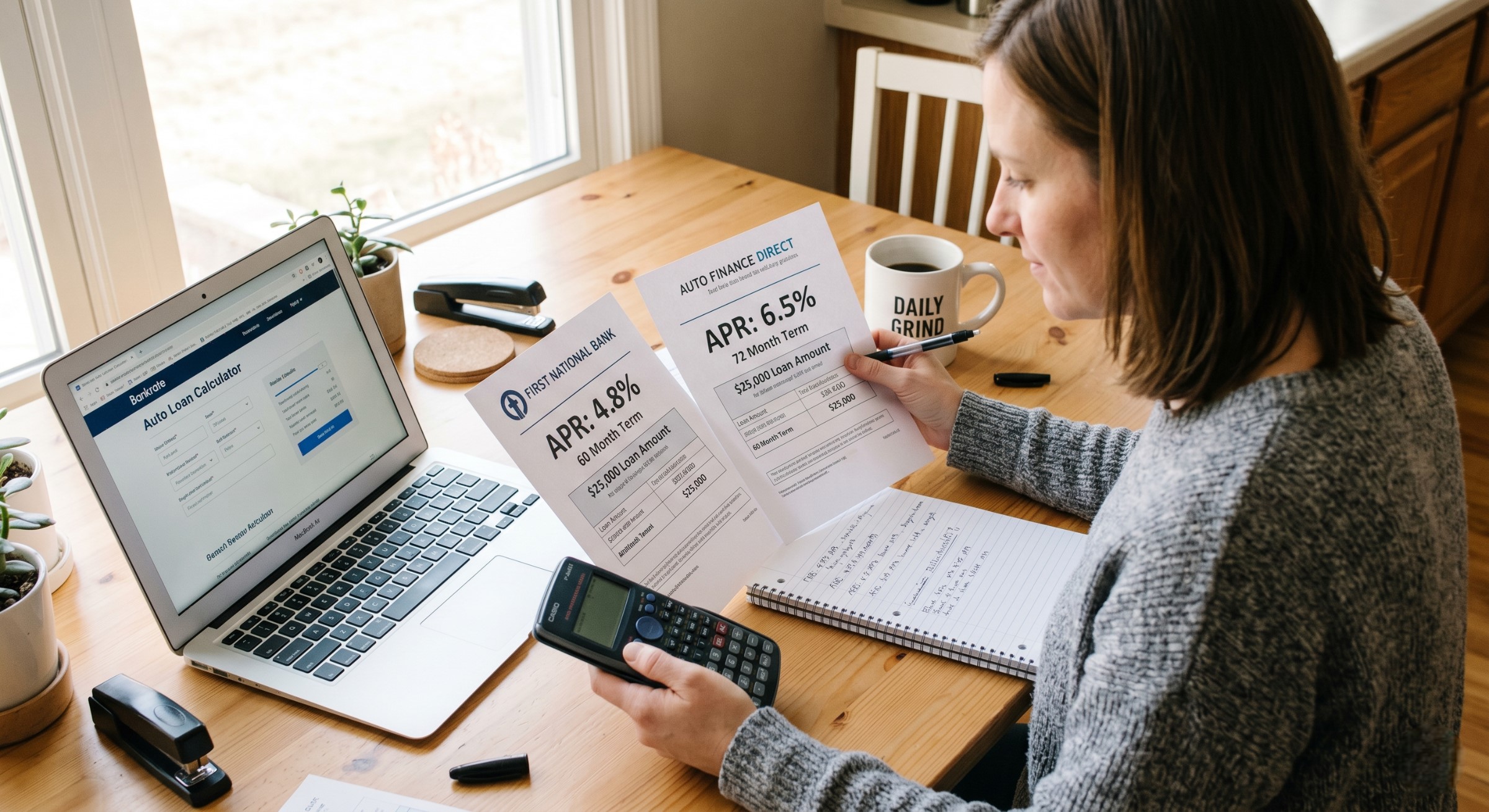

Get pre-approved before you shop. This is the single biggest thing. Pre-approval tells you what you actually qualify for, at what rate, before you walk into a dealership. It also gives you leverage when the dealer’s finance manager tries to mark up the rate. Auto loan pre-approval through a service like Carfixcredit takes a couple of minutes and doesn’t affect your credit score.

Bring a real down payment. Even an extra $500 or $1,000 can move you into a better lender tier and lower your rate noticeably. If you can wait a month or two to save up, the savings over the life of the loan often justify the wait.

Pick a vehicle that fits the lender’s profile. A reliable used car in the $12,000 to $20,000 range that’s under 8 years old is going to get you better terms than a high-mileage older vehicle, even if the price tag is similar. Lenders price loans partly based on what they could recover if they had to repossess the car, so a vehicle they’re confident in usually means better rates for you.

Be honest about your situation. Don’t oversell your income. Don’t hide a bankruptcy. Lenders find out anyway, and getting caught in something inaccurate kills the deal. Walking in with clean documentation and a straightforward story actually moves the deal faster.

Read what you sign. Sounds obvious. A lot of buyers don’t. Check the APR, the term, the total cost over the life of the loan, and every line item that’s been added. Make sure it matches what you were told.

The refinance plan

Here’s the part most subprime buyers don’t realize when they sign their first loan. You don’t have to live with the rate forever.

Twelve to 18 months of on-time payments rebuilds your credit faster than almost anything else. Once your score has come up, you can refinance the loan at much better terms. A lot of buyers who started at 18% on their first subprime loan refinance into something closer to 10% within a year and a half.

That changes how you should think about the original rate. The rate on your first loan after a credit hit is the price of admission to the rebuild. It’s not the rate you’re stuck with for the next six years. Make the payments on time, watch your credit recover, and refinance when the math makes sense.

This is how the subprime cycle works for buyers who use it well. First loan gets you into a car and starts the credit rebuild. Refinance lowers your payment and saves real money. Eventually you graduate out of subprime entirely and your next car loan is at prime rates.

The bottom line

Subprime auto loans aren’t predatory by default and they’re not a trap. They’re a real product that millions of Americans use every year to get into reliable transportation while their credit recovers from whatever knocked it down.

The trick is knowing the difference between a legitimate subprime loan and a deal that’s been padded, manipulated, or structured against your interest. Most lenders in this space are honest. Some aren’t. Walking in informed, getting pre-approved before you shop, reading what you sign, and having a refinance plan in mind protects you from the bad versions and gets you the best terms the good versions can offer.

If your credit needs work, that doesn’t mean you can’t buy a car. It just means the loan you take this year might cost more than the loan you take three years from now. That’s a tradeoff most people can live with.

How Carfixcredit can help you find an honest subprime option

A lot of buyers walk into dealerships hoping for the best and end up signing whatever they’re offered because they don’t know what else is available. The truth is the subprime market has way more options than most buyers see, and the lender network you’re working with makes a huge difference in the deal you end up with.

Carfixcredit works with a network of lenders across the United States who handle real-world credit situations every day. Bad credit, no credit, past bankruptcies, recent repossessions, none of these are automatic disqualifiers. The options available to buyers in these situations are usually broader than people assume, and seeing what you actually qualify for gives you leverage when you sit down at a finance desk.

Getting pre-approved takes about two minutes, doesn’t affect your credit score, and gives you a real number to work with instead of walking in blind. No sales pressure, no commitment, just a straight answer on what’s available to you.

If you want to know what your options actually look like before you start shopping, that’s the next step.