")

Shopping for a car is exciting. But the moment you sit down to talk financing, one thing can change everything — your credit score. Whether you’re buying a brand-new sedan in California, a used pickup truck in Texas, a motorcycle in Florida, or an ATV for the trails in Colorado, the three digits that make up your credit score will quietly shape every single part of your loan: the interest rate you’re offered, your monthly payment, how long you’ll be paying, and sometimes whether you get approved at all.

The credit score car loan connection is one of the most important financial relationships most Americans will ever encounter. And yet, most people only discover how powerful it is after they’re already sitting at a dealership. This guide exists to change that.

At CarFix Credit, we’ve helped over 183,000 Americans across all 50 states secure auto financing — from everyday cars and trucks to motorcycles, ATVs, Sea-Doos, and side-by-sides. We work with borrowers across every credit tier, from the highest scores to the most challenging situations. Over the years, we’ve seen firsthand how understanding your credit score transforms the entire borrowing experience — from stressful and confusing to clear, confident, and empowering.

This is the most comprehensive guide we’ve ever written on the subject. Whether you have excellent credit, fair credit, or a history you’d rather forget, this article will give you everything you need to understand exactly how your credit score affects your car loan — and what you can do about it starting today.

")

What Is a Credit Score — and Where Does It Come From?

A credit score is a three-digit number that ranges from 300 to 850. It is a numerical summary of your credit history — how reliably you borrow money and pay it back. Think of it like a school grade, but for your financial behavior. The higher the number, the better your grade, and the more confidence lenders have in your ability to repay a loan.

Your credit score isn’t assigned by your bank or the government. It’s calculated by independent organizations called credit bureaus, also known as consumer reporting agencies. There are three major bureaus in the United States: Equifax, Experian, and TransUnion. Each bureau collects its own data from lenders, credit card companies, and financial institutions, which is why your score may differ slightly from one bureau to another.

FICO Score vs. VantageScore — What’s the Difference?

Most auto lenders use a scoring model called the FICO Score, developed by the Fair Isaac Corporation. FICO scores are the industry standard for car loans, mortgages, and personal lending in America. You may also see references to the VantageScore, which was developed jointly by the three credit bureaus as an alternative. Both models use the same 300 to 850 range, but they weight certain factors differently.

For the purposes of credit score car loan decisions, FICO is king. When CarFix Credit’s lending partners evaluate your application, FICO is typically the score they’ll pull. However, it’s worth monitoring both — especially if you’re using a free service like Credit Karma, which often shows your VantageScore.

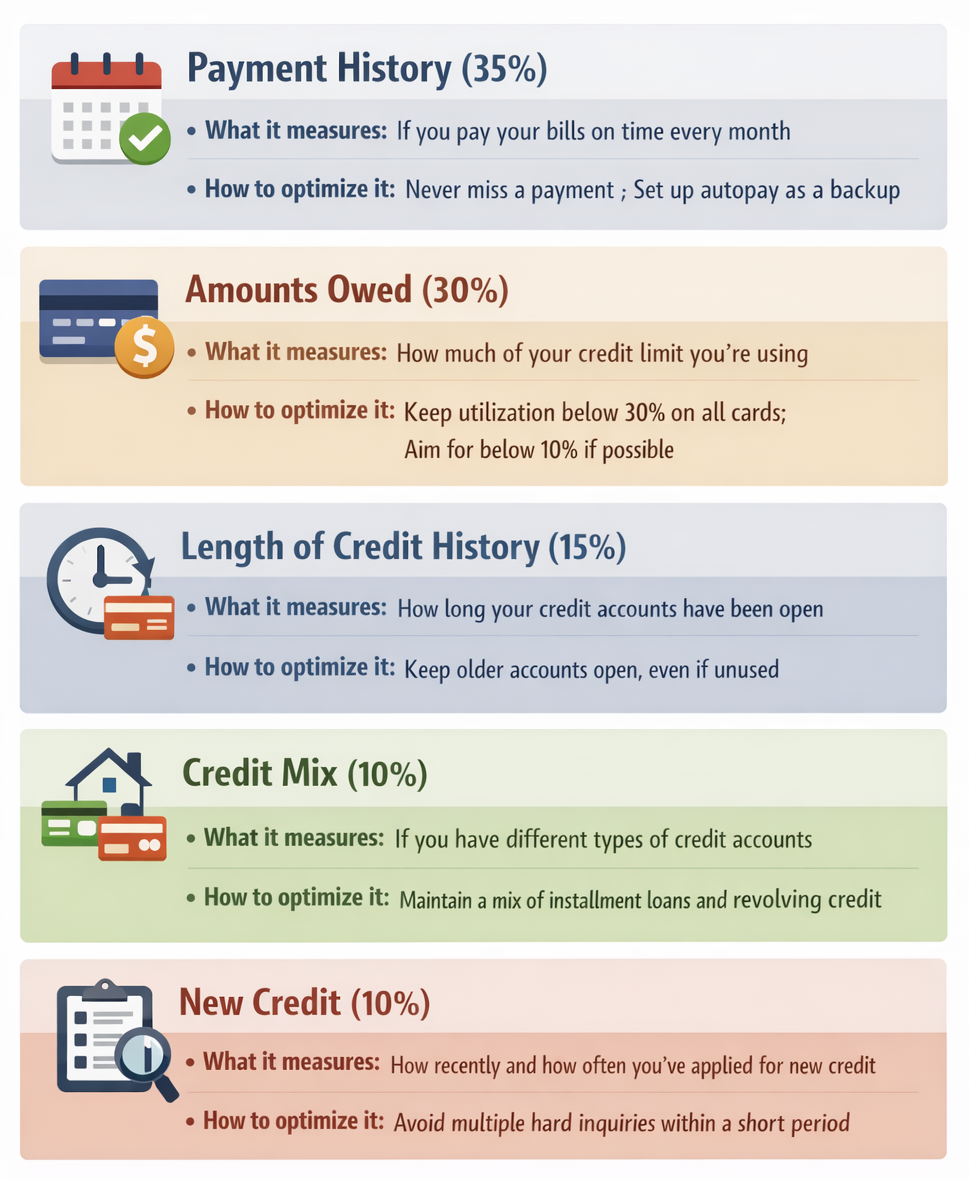

The Five Factors That Make Up Your FICO Score

Your FICO score is not random — it’s a precise calculation built from five categories of financial behavior. Here’s a breakdown of each factor, from most to least impactful:

Why Payment History Carries the Most Weight

At 35% of your total score, payment history is the single most powerful factor in your credit profile. A single missed payment — even just 30 days late — can drop your score by 60 to 110 points depending on your current standing. That kind of drop can push you from a prime borrower into near-prime territory, which could cost you thousands of dollars in extra interest on your next car loan.

On the flip side, every on-time payment you make is a positive mark being added to your record. This is why consistent, on-time payments are the foundation of both building and rebuilding credit. It’s also why successfully repaying a CarFix Credit auto loan — even at a higher interest rate — can meaningfully improve your credit profile over time.

Understanding Credit Utilization — The Silent Score Killer

Credit utilization refers to how much of your available revolving credit (primarily credit cards) you are currently using. If you have a combined credit limit of $10,000 across all your cards and you’re carrying a balance of $4,500, your utilization rate is 45% — which most lenders consider high.

Ideally, you want to keep your utilization below 30%. The best scores tend to belong to people who keep utilization below 10%. The great news is that paying down balances is one of the fastest ways to improve your score — improvements can show up on your report in as little as 30 days after a balance is paid down.

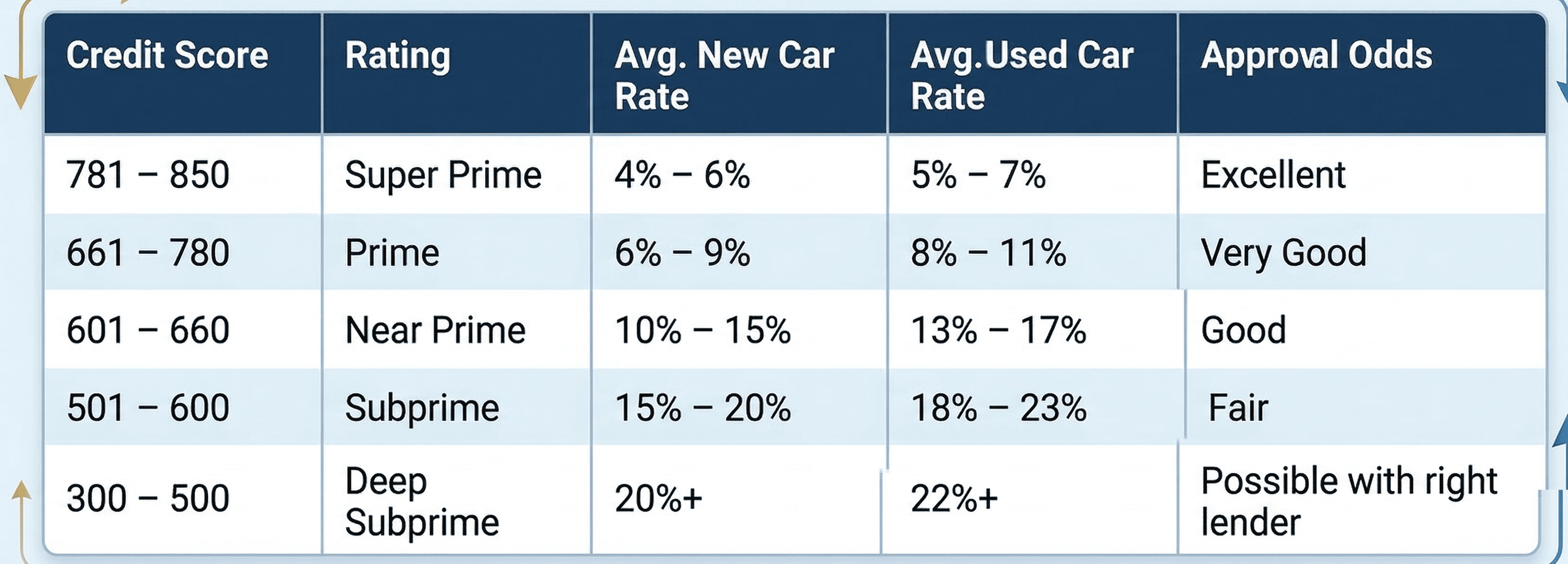

The Five Credit Score Tiers — What Each One Means for Your Car Loan

When you apply for a credit score car loan, lenders don’t just look at your raw number — they place you into a credit tier or category. Each tier comes with different risk expectations, interest rate ranges, and approval conditions. Understanding which tier you fall into before you apply puts you in a dramatically stronger position.

Tier 1 — Super Prime (781 to 850): The Pinnacle of Borrowing Power

Super prime borrowers have done everything right over a long period of time. You pay every bill on time, you carry little to no revolving debt, your credit history is long and well-established, and you haven’t been applying for new credit excessively. Lenders see you as the lowest-risk category of borrower and compete for your business.

At this tier, auto loan interest rates for new vehicles typically range from 4% to 6%. On a $30,000 car loan over 60 months, that translates to roughly $497 per month and a total interest cost of around $4,820. Super prime borrowers also have the most leverage to negotiate — dealers and lenders know you can walk away.

If you’re in this tier, CarFix Credit can still help you find competitive rates and fast pre-approval, especially for specialty vehicles like motorcycles, ATVs, or powersports equipment that many traditional banks are reluctant to finance.

Tier 2 — Prime (661 to 780): Strong, Stable, and Well-Positioned

Prime borrowers represent the largest segment of American auto loan applicants. You have a solid track record — maybe a late payment here or there in your past, or a credit card balance that’s slightly higher than ideal — but overall, lenders trust you. Approval rates in this tier are high and rates are competitive.

Expect rates between 6% and 9% for new vehicles and slightly higher for used. On that same $30,000 loan over 60 months, a prime borrower at 8% pays about $608 per month and roughly $6,480 in total interest. That’s still very manageable and reflects your strong credit history.

Prime borrowers working with CarFix Credit have access to our full lending network, which means we can shop multiple lenders on your behalf to find you the most competitive rate available — whether you’re financing a family SUV or a Kawasaki Ninja.

Tier 3 — Near Prime (601 to 660): The Crossroads Tier

Near prime is where the financial stakes become more tangible. You’re not in bad shape, but you’re not in great shape either. Perhaps you’ve missed a few payments in the past, you’re carrying higher-than-average balances, or you simply haven’t had enough time to build a long credit history. Lenders will likely approve you, but with conditions.

Interest rates in this tier typically range from 10% to 15% for new vehicles and up to 17% for used. A $30,000 loan at 12% over 60 months means monthly payments around $668 and total interest close to $10,080 — significantly more than a prime borrower pays for the same car.

Here’s the important insight for near prime borrowers: even a 30 to 50-point improvement in your credit score could move you into prime territory and potentially save you $4,000 or more in interest on a typical auto loan. If you’re in this tier, it’s worth spending 60 to 90 days improving your score before applying. CarFix Credit can also walk you through what loan terms and vehicle price points make the most sense given your current position.

Tier 4 — Subprime (501 to 600): Approval Is Possible — Here’s What to Expect

Subprime borrowers have experienced real credit challenges — significant missed payments, high debt levels, a previous repossession, collections accounts, or other negative marks on their report. Conventional banks and credit unions may decline applications in this range, but specialized auto lenders — like those in CarFix Credit’s network — work with subprime borrowers every day.

Interest rates in this tier typically range from 15% to 20% or higher, and lenders may require a down payment of 10% or more to offset their risk. On a $20,000 loan at 18% over 60 months, you’d pay approximately $508 per month and close to $10,480 in total interest. It’s more expensive — but it’s also an opportunity.

CarFix Credit specializes in connecting subprime borrowers with lenders who understand that a low score doesn’t define your full financial picture. We look at income, employment stability, down payment, and other factors to build the strongest possible application on your behalf. And importantly — every on-time payment you make on your new auto loan helps rebuild your score for the future.

Tier 5 — Deep Subprime (300 to 500): Don’t Give Up — Here’s Your Path Forward

Deep subprime is the most challenging credit tier, but it’s not a dead end. Many borrowers in this range have experienced serious financial hardship — bankruptcy, medical debt, extended unemployment, or a history of repossessions. These events leave deep marks on a credit report, sometimes for seven to ten years.

Despite the challenges, millions of deep subprime borrowers successfully finance vehicles every year through specialty lenders. The keys are finding the right lender, offering a meaningful down payment (typically 15% to 20% or more), demonstrating stable income, and being realistic about the vehicle price you’re targeting.

CarFix Credit was built with borrowers like this in mind. Our team works with a broad network of lenders — including those who specialize exclusively in deep subprime auto financing. We’ve helped thousands of Americans in this tier get into reliable vehicles that they use every day. And we treat every application with the same respect and seriousness, regardless of where your score currently sits.

The Real Dollar Cost of Your Credit Score

The easiest way to understand the impact of credit is to look at actual loan costs.

For a $25,000 vehicle financed over 60 months, a super prime borrower at about 5% interest might pay around $472 per month, for a total of about $28,307, with $3,307 in interest.

- A prime borrower at roughly 8% might pay around $507 per month, for a total of $30,400, including $5,400 in interest.

- A near prime borrower at around 12% could pay approximately $556 per month, for a total of $33,361, which includes $8,361 in interest.

- A subprime borrower at around 18% might pay close to $635 per month, totaling $38,091, with $13,091 in interest.

- A deep subprime borrower at around 23% could face monthly payments near $703, for a total cost of $42,168, including $17,168 in interest.

- That means a deep subprime borrower buying the exact same $25,000 vehicle could pay nearly $14,000 more overall than a super prime borrower.

On a $50,000 vehicle financed over 72 months, the differences grow even more dramatic. A super prime borrower at 5.5% might pay about $807 per month, with $8,104 in total interest, for a total cost of $58,104.

- A prime borrower at 9% might pay about $878 per month, with $13,216 in interest, bringing total cost to $63,216.

- A near prime borrower at 13% may pay around $969 per month, with $19,768 in interest, for a total of $69,768.

- A subprime borrower at 19% might pay close to $1,104 per month, with $29,488 in total interest, resulting in $79,488 total cost.

- A deep subprime borrower at 24% could end up paying around $1,218 per month, with $37,696 in interest, for a total cost of $87,696.

- These examples make one point very clear: improving your credit score before a major purchase can deliver one of the highest financial returns available.

Beyond the Score — Other Factors Lenders Evaluate

Your credit score matters, but it is not the only thing lenders consider.

Debt-to-Income Ratio

Debt-to-income ratio, or DTI, measures how much of your monthly gross income goes toward debt payments. Lenders add up your recurring obligations and divide that by your income. Most traditional lenders prefer a DTI below 45%, though some subprime lenders may go a bit higher.

Monthly Income and Employment Stability

Lenders also want proof that you can comfortably afford the loan. That usually means verifying income and employment. Continuous employment with the same employer for six months to a year often strengthens an application. Self-employed and gig workers can still qualify, though they may need more documentation.

Down Payment

A down payment is one of the strongest tools you control. It lowers the amount you need to finance and shows the lender that you are financially invested in the purchase. For near-prime borrowers and below, 10% to 20% down can significantly improve approval chances.

Loan-to-Value Ratio

Loan-to-value ratio, or LTV, compares the amount borrowed to the value of the vehicle. If you borrow more than the vehicle is worth, lenders see that as riskier. Most prefer an LTV at or below 100%, though some allow slightly higher depending on the situation.

Vehicle Type, Age, and Condition

The car itself matters too. Newer vehicles are usually easier to finance because they are more valuable collateral. Older, high-mileage vehicles may come with stricter approval standards. CarFix Credit’s lender network includes options for older vehicles and specialty vehicles that many traditional banks avoid.

Co-Signer Availability

A co-signer with stronger credit can improve your approval odds and may help secure a better rate. For borrowers with low scores or limited history, a co-signer can sometimes make the difference between a decline and an approval.

What Vehicles Can CarFix Credit Help You Finance?

One of CarFix Credit’s biggest advantages is the variety of vehicles it can help finance.

The company works with financing for sedans, such as the Toyota Camry, Honda Civic, and Nissan Altima. These are common daily-driver vehicles with strong resale value.

It also finances SUVs and crossovers, including vehicles like the Ford Explorer, Chevrolet Equinox, and Toyota RAV4. These remain popular among families and buyers in every credit tier.

For trucks and pickups, CarFix Credit can help with models like the Ford F-150, RAM 1500, and Chevrolet Silverado. These vehicles are often used for both work and personal use and tend to hold value well.

The company also supports financing for hatchbacks, such as the Honda Fit, Mazda3, and Toyota Prius, which are often attractive to city drivers and first-time buyers.

On the powersports side, CarFix Credit can finance motorcycles, including brands like Harley-Davidson, Honda CBR, and Kawasaki Ninja.

It can also help with ATVs and UTVs, such as Can-Am, Polaris Sportsman, and Honda Foreman models.

For watercraft buyers, CarFix Credit offers financing for Sea-Doos and other personal watercraft, including the Sea-Doo Spark, Yamaha WaveRunner, and Kawasaki Jet Ski.

The company also helps finance side-by-sides, including models like the Polaris RZR, Can-Am Maverick, and Yamaha YXZ.

Why Powersports Financing Is Different

Financing a Sea-Doo or an ATV is not the same as financing a sedan. Powersports vehicles have different depreciation patterns, seasonal usage, and insurance requirements. Many banks are not equipped to underwrite these loans properly.

CarFix Credit works with lenders who specifically understand powersports and recreational financing. That means more flexibility, less confusion, and better chances of matching borrowers with the right lender.

Whether you want to finance a WaveRunner in Florida, a Polaris RZR in Wyoming, or a Harley-Davidson in Tennessee, CarFix Credit has lender relationships built for that purpose.

Loan Amounts From $5,000 to $75,000

CarFix Credit offers financing from $5,000 to $75,000.

- At the lower end, $5,000 to $10,000 may be ideal for used economy cars, entry-level motorcycles, or basic ATVs.

- The $10,000 to $25,000 range can cover many used trucks, mid-range SUVs, newer motorcycles, and quality used sedans.

- From $25,000 to $45,000, borrowers may be looking at new midsize vehicles, well-equipped trucks, premium powersports options, or Sea-Doos.

- At the top end, $45,000 to $75,000 can support financing for full-size trucks, luxury vehicles, premium powersports packages, or high-end UTVs with accessories.

Understanding Loan Terms — From 12 to 96 Months

Your loan term is one of the most important decisions you will make because it directly affects both your monthly payment and the total interest you pay.

For a $25,000 loan at 8% interest, a 12-month term might come with a payment around $2,238 per month and only about $858 in total interest. This is best for borrowers who want the lowest overall cost and can manage a very high monthly payment.

- A 24-month term might mean about $1,130 per month and approximately $1,720 in interest.

- A 36-month term could bring the payment to roughly $762 per month, with around $2,632 in total interest.

- A 48-month term may produce a payment near $577 per month, with total interest around $3,696.

- A 60-month term, which is one of the most common options in the U.S., might result in about $470 per month and $4,200 in total interest.

- A 72-month term could lower the payment to around $398 per month, but total interest jumps to roughly $6,656.

- An 84-month term might reduce the payment further to about $344 per month, though total interest climbs to around $8,896.

- Finally, a 96-month term may bring the monthly payment down to about $305, but total interest could reach roughly $11,280.

The Short-Term vs. Long-Term Trade-Off

Shorter terms usually mean higher monthly payments but lower total cost. They are ideal for borrowers with stable, strong income who want to build equity quickly and pay less interest overall.

Medium-length terms, especially 48 to 60 months, tend to strike the best balance between affordability and total cost. That is why they remain so popular.

Longer terms, such as 72 to 96 months, offer lower monthly payments but can leave you paying much more overall. They may also increase the chance of being upside down on the loan, meaning you owe more than the vehicle is worth.

When a 96-Month Loan Makes Sense

CarFix Credit offers terms up to 96 months to help borrowers who need the lowest possible monthly payment. While it is not the cheapest option in the long run, it can make reliable transportation more accessible for some buyers.

This kind of term usually makes the most sense on higher-value vehicles expected to last well beyond the loan period, such as dependable trucks or new SUVs with strong reliability.

How to Improve Your Credit Score Before Applying

If your score needs work, there are still practical steps you can take.

- First, make every payment on time starting now. Payment history has the biggest impact on your score, so consistency matters more than anything else.

- Second, pay down credit card balances aggressively. Utilization is one of the fastest-moving parts of your score, and reducing balances can create noticeable improvements quickly.

- Third, request a credit limit increase if your account is in good standing. A higher limit can lower your utilization ratio without requiring you to pay off all the debt immediately.

- Fourth, dispute errors on your credit report. Incorrect late payments, duplicate accounts, or outdated debts can hurt your score unfairly.

- Fifth, consider becoming an authorized user on a trusted family member’s credit card account if it has a long history, low utilization, and perfect payment behavior.

- Sixth, avoid applying for new credit before your auto loan application. Too many hard inquiries can temporarily lower your score.

- Seventh, keep old credit accounts open. Long credit history helps your score, even if those accounts are no longer used often.

- Eighth, consider a credit builder loan if you have little or no credit history. These small installment loans can help establish positive payment records.

In general, paying down balances can help within 30 days. Consistent on-time payments and utilization improvements often begin producing meaningful movement within 60 to 90 days. More serious recovery from collections, repossessions, or charge-offs usually takes longer.

If you need a vehicle now, applying today and planning to refinance later can still be a smart strategy.

Can You Get a Car Loan with Bad Credit?

Yes, you can.

Bad credit is not an automatic rejection. It simply means lenders will examine your overall financial picture more carefully. With the right lender, the right vehicle, and the right application structure, many borrowers with damaged credit can still secure financing.

CarFix Credit frequently helps borrowers dealing with recent bankruptcy, prior repossessions, collections, charge-offs, no credit history, or thin credit files.

A car loan can also become an important credit-building tool. It adds installment credit to your profile, improves your credit mix, and creates a fresh stream of on-time payments that strengthen your payment history. After 12 to 24 months of good payment behavior, many borrowers improve enough to refinance at a lower rate.

CarFix Credit’s platform is designed with credit-challenged borrowers in mind. It works with lenders that specialize in subprime and deep subprime approvals, evaluates more than just the score, and offers loan options across a wide range of vehicle types and price points.

CarFix Credit’s Online Pre-Approval Process — How It Works

The company’s online pre-approval process is designed to remove uncertainty before you visit a dealership.

First, you can start the application online anytime, from your phone, tablet, or computer.

Second, you provide basic financial details such as your name, address, income, employment information, and the type of vehicle you want.

Third, CarFix Credit shops your profile across its lender network rather than relying on just one bank. That means your application is matched with lenders most likely to approve it and offer appropriate terms.

Fourth, you receive a pre-approval offer showing your likely loan amount, estimated rate range, and available repayment terms.

Finally, you can shop for your vehicle with confidence, knowing your budget and financing structure ahead of time.

Importantly, checking your pre-approval options begins as a soft inquiry, so your credit score is not harmed just for exploring your options.

Smart Strategies Before You Sign

Before finalizing any car loan, review your credit report for errors. Get pre-approved before you shop so you understand your budget. Compare total loan cost, not just the monthly payment. Review all add-ons and extras carefully to make sure nothing unnecessary is increasing the amount you finance.

You should also check whether the loan includes prepayment penalties, consider GAP coverage if you are taking a long-term loan, plan ahead for refinancing if your credit is likely to improve, and make extra payments whenever possible to reduce total interest.

Frequently Asked Questions

Does checking my credit score hurt it?

No. Checking your own score is a soft inquiry and has no negative impact. Only hard inquiries from lenders reviewing your application can temporarily lower your score.

How many points will a car loan application lower my score?

Usually about 5 to 10 points. The effect is temporary. Also, most FICO models treat multiple auto loan inquiries made within a short shopping window as a single inquiry.

What credit score do I need to get a car loan with no money down?

Generally, scores of 660 or above give you the best chance. Borrowers below that may still qualify, but lenders will usually examine income, DTI, and other factors more closely.

Is a 600 credit score enough for a car loan?

Yes. A 600 score typically falls into the near-prime range, and many lenders will still work with you. Rates may be higher, but approval is very possible.

Can I get approved after bankruptcy?

Yes. Many lenders work with borrowers after bankruptcy discharge. You may need a larger down payment and should expect higher starting rates, but financing is often available.

Can I finance a motorcycle, ATV, or Sea-Doo through CarFix Credit?

Absolutely. CarFix Credit offers financing for motorcycles, ATVs, side-by-sides, Sea-Doos, and other powersports vehicles across a range of credit profiles.

How long does pre-approval take?

The online application takes only minutes, and many borrowers receive an answer the same day.

What loan terms does CarFix Credit offer?

CarFix Credit offers repayment terms from 12 to 96 months.

What states does CarFix Credit serve?

All 50 states.

Can I refinance my current auto loan through CarFix Credit?

Yes. If your credit score has improved since you first financed your vehicle, refinancing may help reduce your rate and save money over time.

The Bottom Line: Your Credit Score Is a Powerful Tool — Use It

Your credit score is not a permanent judgment. It is a snapshot of your credit behavior at a given moment, and it can change. Understanding how credit affects car financing helps you make better decisions, prepare strategically, and approach the process with more confidence.

Whether you are buying your first vehicle, rebuilding after financial hardship, or simply trying to secure the best possible loan terms, the key is to understand where you stand and what your options are.

CarFix Credit has already helped more than 183,000 Americans secure vehicle financing. The company offers loan amounts from $5,000 to $75,000, terms from 12 to 96 months, and financing for cars, SUVs, trucks, hatchbacks, motorcycles, ATVs, Sea-Doos, and side-by-sides. It works with borrowers across all credit tiers and serves all 50 states from its headquarters in Miami, Florida.

If your credit score is 800 or 480, CarFix Credit aims to connect you with flexible, competitive loan options tailored to your situation. The company offers fast online pre-approval, considers all credit backgrounds, works with a wide network of lenders, and provides a streamlined process designed to get borrowers on the road faster.

Visit CarFix Credit to explore your options and start your free pre-approval. Checking what you qualify for takes only minutes and does not hurt your credit score.

About CarFix Credit

CarFix Credit is a U.S.-based auto financing platform headquartered in Miami, Florida. The company connects borrowers in all 50 states with flexible vehicle loan options ranging from $5,000 to $75,000 and repayment terms from 12 to 96 months. CarFix Credit specializes in helping Americans across all credit tiers — from excellent to deep subprime — secure financing for cars, trucks, SUVs, hatchbacks, motorcycles, ATVs, Sea-Doos, side-by-sides, and more.

Disclaimer

Interest rate ranges, monthly payment estimates, and total cost figures in this article are approximate and intended for educational illustration only. Actual rates and loan terms vary based on your credit profile, lender, vehicle, loan amount, down payment, and state. This content does not constitute financial advice. Consult a qualified financial professional for advice specific to your situation.